Igatahes:

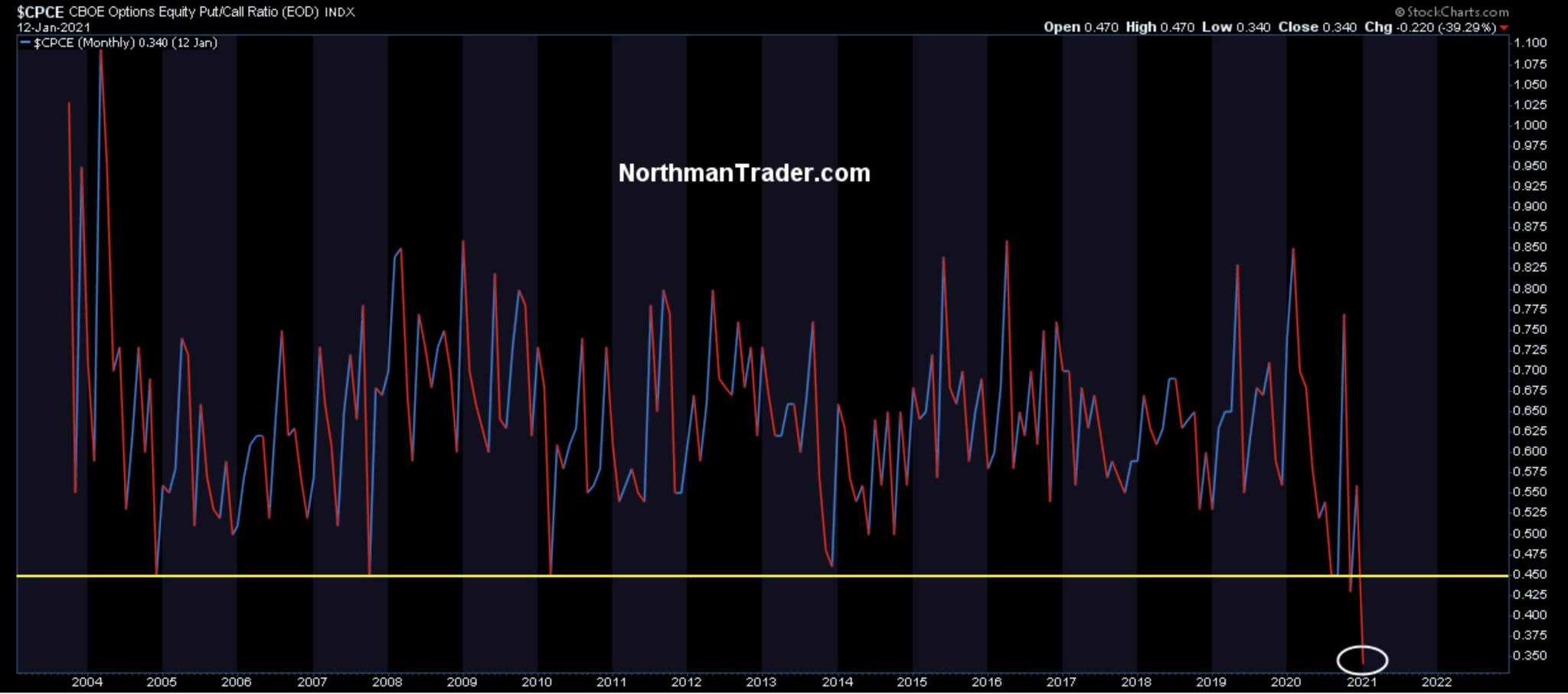

Put/call

The Winners of the New World

Cramer lists his top 10 favorite stocks and explains the methodology behind his choices.

JIM CRAMER FEB 29, 2000 9:42 AM EST

Editor's Note: James J. Cramer is the keynote speaker at the 6th Annual Internet and Electronic Commerce Conference and Exposition, held today at the Jacob Javits Center in New York City. We're running the full text of that speech here.

You want winners? You want me to put my

Cramer Berkowitz

hedge fund hat on and just discuss what my fund is buying today to try to make money tomorrow and the next day and the next? You want my top 10 stocks for who is going to make it in the New World? You know what? I am going to give them to you. Right here. Right now.

OK. Here goes. Write them down -- no handouts here!:

724 Solutions

(SVNX)

,

Ariba

(ARBA)

,

Digital Island

(ISLD)

,

Exodus

(EXDS)

,

InfoSpace.com

(INSP)

,

Inktomi

(INKT)

,

Mercury Interactive

(MERQ)

,

Sonera

(SNRA)

,

VeriSign

(VRSN)

and

Veritas Software

(VRTS)

.

We are buying some of every one of these this morning as I give this speech. We buy them every day, particularly if they are down, which, no surprise given what they do, is very rare. And we will keep doing so until this period is over -- and it is very far from ending. Heck, people are just learning these stories on Wall Street, and the more they come to learn, the more they love and own! Most of these companies don't even have earnings per share, so we won't have to be constrained by that methodology for quarters to come.

There, now that that's done with, can we talk about the methodology that produced those top 10 so that you can understand how, in a universe of a gazillion stocks, we arrived at those, so you too can figure it out? I hope we can because I have another 10 and still another 10 and another. They all do the same thing: They make the Web faster, cheaper, better and easier to access anywhere, anytime. They allow you to get on the Web securely anywhere in the world. They make the Web economy the only economy that matters. That's all they do.

We try to own every one of them. Every single one. And if I had my druthers, I wouldn't own any other stocks in the year 2000. Because these are the only ones worth owning right now in this extremely difficult, extremely narrow stock market. They are the only ones that are going higher consistently in good days and bad. I love every one of them, just as I loathe the rest of the stock universe.

How did this stock market get like this, to where the only people who can make a dime in it are the people who are interested in the most arcane subject, the moving of data from one space to another, via strange new machines and software? How did it get to the point where nothing else matters, most particularly the 90% of the stock market I have studied for the last 20 years? How did all of that knowledge become totally irrelevant and the only stocks that work are the stocks of companies that didn't exist five years ago and came public in the last two or three years?

Let's start with the world in the early 21st century, a world where capital is abundant for a chosen few and nonexistent for just about everybody else. It is a world where the whole of Wall Street and Silicon Valley is at your fingertips if you are creating the infrastructure for the New Economy, and a world where neither Wall Street nor Silicon Valley could give a darn about you if you are using that infrastructure.

Or in other words, we don't care if

General Motors

(GM)

and

Ford

(F)

are going with

Oracle

(ORCL)

or with

i2

(ITWO)

for their new parts procurement process. We don't want to own GM or Ford on any occasion. In fact, we would rather own the loser in that tech bake-off than the winner in nontech, because in this new world, there is so much business to be done for the i2s and the Oracles that the capital will remain plentiful for them, win or lose a particular piece of business.

Just yesterday I found myself wishing I had bought i2 when it lost out to Oracle for the giant business-to-business contract for the Big Three automakers. Others had the same idea because i2, the loser Friday, was up much more Monday than GM and Ford could be this year. i2 can own the world because the company with the access to cheap capital always wins. And the companies with no access have to lose.

Or, closer to home. We in the stock market don't care that

The Street.com Inc.

(TSCM)

, a company I helped create, has built a compelling new brand, has more than 100,000 paid subscribers and has $100 million in the bank. We just want to know which companies TheStreet.com employs to publish each day. We want to know who the host is, which publishing tool works best, which wireless strategy TheStreet.com is adopting and how does it automate its email? (By the way, the answers are Exodus,

Vignette

(VIGN)

,

Motorola

(MOT)

and

Kana

(KANA)

-- all at or near their 52-week highs as TheStreet.com languishes at its 52-week low, a triumph of the arms merchants over the combatants if there ever were one.)

How did this bizarro world where nine-tenths of the companies I have followed as a stock picker for the last 20 years are losers and one-tenth are winners? To answer that question, you have to throw out all of the matrices and formulas and texts that existed before the Web. You have to throw them away because they can't make money for you anymore, and that is all that matters. We don't use price-to-earnings multiples anymore at Cramer Berkowitz. If we talk about price-to-book, we have already gone astray. If we use any of what Graham and Dodd teach us, we wouldn't have a dime under management.

So how do we sort through which stocks get bought and which stocks get assigned to the waste bin?

We have a phrase on Wall Street. It's called

raising the bar. If you can raise the bar, or brighten the outlook for your company, if you can see your growth accelerating, your stock will go higher and you will be given the currency to expand, acquire and do whatever you want. That's the secret of the quintessential New Economy stock:

Cisco

(CSCO)

. This giant networker has the ability to control its own destiny. It can, as my colleague

Adam Lashinsky

says at

TSC

, buy any company it wants to. It can pay any price. Because it has a currency that it better than U.S. dollars: It has Cisco stock. It can do that because it raises the bar every quarter!

But what about the Old Economy stocks? Can

Merck

(MRK)

raise the bar? Can

Pfizer

(PFE)

? Can

U.S. Steel

(X)

? Or

Phelps Dodge

(PD)

?

Union Pacific

(UNP)

? No, no, no, no, no and no. So what happens to them? Despite the billions in buybacks and the plethora of strong buys that the Street has put out about these companies, their stocks have no traction. They just stumble along, rising and falling haphazardly with every whim and quizzical speech of the

Federal Reserve

chairman that still controls their destiny. If

Greenspan

indicates that there is more tightening ahead, these traditional companies, the ones that you measure with traditional matrices, get pole-axed as we worry about where the capital will ultimately come from if credit gets choked off, while the arms merchants in the Web war, with capital to burn, just go higher.

It is no secret that the

Dow

, made up principally of companies that can't raise the bar, is down 12% while the

Nasdaq

, which is made up of companies that can raise the bar, is up 12%. And in the self-fulfilling jungle that is Wall Street, only growth can maintain growth!

So how do we find what are the great growth companies, knowing that growth and not cheapness of stock to company is what matters? We have to look for the fastest-growing industries and then select the companies that can make the infrastructure happen the fastest and the cheapest in those industries. The growth must be positively organic, if not viral. There must be heavy technological barriers to entry. And there must be an ability to scale without any thought to human cost. These companies must be able to dominate their businesses or be willing to become part of a larger institution that dominates.

So, whom does that eliminate? First, any company that is a commodity producer simply can't be owned, no matter what. The New Economy makes those be simply a function of low-cost producer with no ability ever to raise price. This, of course, is the crying shame of the way the Fed is trying to break the economy because the only place that could stand for a little inflation is in the deflationary commodity industries. But their inflation revolves around the ability to build inventory to anticipate future price hikes and the Fed is taking short rates to a height that makes it uneconomic to stockpile.

Second, it eliminates any bricks-and-mortar company that doesn't embrace the Net. To not embrace the Net is to give a cost edge to a competitor who does. It does so because the Net removes the middleman that was a product of the regional economy. There is $4 trillion worth of wholesaling that gets instantly eliminated by the Net. Before only the largest orders could be processed by the biggest companies because it was too expensive otherwise. Now all orders can be processed by the biggest companies through the Web. There is no need for the jobber or the wholesaler. Obviously, if you are still using that old distribution network, you can't compete against those who do.

Third, it eliminates any industry that does not have a proprietary brand. This is one of those weird features of the Web that people haven't woken up to yet, but it will seem obvious a few months from now. In the New World's economy, the desire to "name your own price" is too great to squelch. An outfit like

priceline

(PCLN)

will change the very nature of brands in this country. It won't destroy the premium brand, but it will force everyone else out of the market. Why? Because the way priceline works is that we are trying to buy the premium brand for the price of the off-price brand. That means the off-price brands, whether they be

Colgate

(CL)

or

Dial

(DL)

or

Hunt's

or

Ralston

(RAL)

, are simply doomed by the Web. Why would you ever buy the second- or third-best when you can get the best via priceline for the same price as the lower tier? Ahh, that's a real killer. It leaves only the top brands to vie for supermarket space. The others won't be worth carrying. They won't move! Oh yeah, same goes for the airlines and the hotels and just about everybody else.

Fourth, it just destroys retail as we know it. Why? Because the companies that embrace the Web more vigorously will eventually be pitted against other companies that embrace the Web more vigorously, creating a virtual constant price war, the kind of war that

Marx

, of all, actually predicted would happen to capitalism. It will happen to retail once everyone realizes that

Amazon

(AMZN)

recreated

Wal-Mart

(WMT)

online because it will forever have access to cheap capital. Why do I say forever? Because at a certain point, it will be done with its buildout and will effectively be able to cherry-pick whomever it wants to destroy while having it be subsidized by other areas. It will be

Home Depot

(HD)

vs. Wal-Mart vs. Amazon in the end. Nobody else. And that's only if Home Depot figures out it better get on the Web and fast.

Fifth, it wipes out everybody who straddles the Old and New Worlds. Let's take the brokerage industry. If you are trying to preserve a price point, because you need those margins, you can't and you become roadkill. Same with journalism. If you are free online and cost offline, you will eventually not be able to charge offline. Why not? Because the

Hewlett-Packards

(HWP)

and

Intels

(INTC)

and Ciscos are bent on making the online version far superior to the offline version. And they will do it. They, too, have the access to capital to make it happen.

I can tell you from

TheStreet.com

that we have substantial cost advantages over our printed cousins. We can come out around the clock. We don't require paper, ink, delivery people or trucks. In that sense, we are much more like television, personal television, which is why we were wrong initially to think we could charge for basic news, and right to think we can charge a huge amount for proprietary analysis that can make you money.

The struggle between the offliners and the onliners in banking will also pan out just like these other industries, with huge wins for those with a fresh online culture and hideous losses for those who don't see it coming or are slow to adjust. If you have to preserve your giant branch network and the costs that come with it while someone else perfects secure wireless Internet transactions, you can forget about it. You can't afford to compete. How can

Bank of America

(BAC)

compete with

Nokia

(NOK)

as a way to bank? How can

Goldman Sachs

(GS)

compete with

Yahoo!

(YHOO)

as a way to invest? Isn't Nokia, with its wireless machine that goes everywhere a better bank than one that needs branches? Isn't Yahoo!, with its access to all of the information and quotes in the financial world a better place to buy stocks than Goldman?

Of course they are.

So, if you can't own the retailers, and you can't own transports, and you can't own banks and brokers and financials and you can't own commodity makers and you can't own the newspapers, and you can't own the machinery stocks, what can you own?

A-ha, that just leaves us with tech. That's why we keep coming back to it. That's why, despite the 80% increase in the Nasdaq last year, we are looking at another record year now. It is by that process of elimination that I have picked my top 10. And my next 10 and my next 10 after. Only those companies are worth owning. The rest?

You can have them.

Thank you.

"martk"

Jim Cramer vahetult enne tehnoloogiasektori kokku varisemist aastal 2000.

"stefan""martk"

Jim Cramer vahetult enne tehnoloogiasektori kokku varisemist aastal 2000.

Üks varaklass mis võib tänavu kokku variseda on raha. See siis juhul kui covid-olukord märgatavalt paraneb, ja keskpangad intressid ei tõsta. Ühesõnaga, võimalik stsenaarium.