Euronav oli üks suuremaid venitajaid, mis võiks olla uute laevade kütus ja selleks saab :development of dual fuel Ammonia (NH3) fitted VLCC and Suezmax vessels. The initial term of the JDP will be three years.

Alati, kui NAT (ticker) hind hakkab kuskilt läbi vajuma, tuleb miskit "ülipositiivset".

Ja siin ka näide, et kütuse kulust ega amordist pole juttu, algaja teeb tehte 17000-8000=9000 ala kasum, reaalsus aga pigem 25 000- 17 000= 8000 loss

Monday, July 19, 2021

Dear Shareholders and Investors,

Rates for our suezmax ships may change very quickly as communicated in the message below.

1) A few days ago we signed a contract for one of our suezmax vessels going via the Suez Canal from the West to the East – with planned discharge in China.

The net TC rate to us is about USD 17,000 per day for 40 days which could extend to 60 days.

2) Last week, we also signed a contract which is lasting for minimum six or could last for seven months at a net TC rate to us of about

USD 17,000 per day.

The average operating costs for our ships are about USD 8,000 per day per ship. The two ships load the cargoes more or less immediately. Our contractual partners are first class companies.

Our rates – 1) & 2) - are strongly up compared with some reports, indicating rates of USD 4,000 to USD 5,000 a day or even lower in reports produced by outside parties.

Our two recent contracts are at very different levels (USD 17,000/day), a strong signal for the way forward.

NAT has 25 suezmax vessels, including two newbuildings to be delivered in 2022.

Sincerely,

Herbjorn Hansson

Founder, Chairman & CEO

Nordic American Tankers Ltd. www.nat.bm

Ja siin ka näide, et kütuse kulust ega amordist pole juttu, algaja teeb tehte 17000-8000=9000 ala kasum, reaalsus aga pigem 25 000- 17 000= 8000 loss

Monday, July 19, 2021

Dear Shareholders and Investors,

Rates for our suezmax ships may change very quickly as communicated in the message below.

1) A few days ago we signed a contract for one of our suezmax vessels going via the Suez Canal from the West to the East – with planned discharge in China.

The net TC rate to us is about USD 17,000 per day for 40 days which could extend to 60 days.

2) Last week, we also signed a contract which is lasting for minimum six or could last for seven months at a net TC rate to us of about

USD 17,000 per day.

The average operating costs for our ships are about USD 8,000 per day per ship. The two ships load the cargoes more or less immediately. Our contractual partners are first class companies.

Our rates – 1) & 2) - are strongly up compared with some reports, indicating rates of USD 4,000 to USD 5,000 a day or even lower in reports produced by outside parties.

Our two recent contracts are at very different levels (USD 17,000/day), a strong signal for the way forward.

NAT has 25 suezmax vessels, including two newbuildings to be delivered in 2022.

Sincerely,

Herbjorn Hansson

Founder, Chairman & CEO

Nordic American Tankers Ltd. www.nat.bm

STNG on omadega tagasi veebruaris. Kui ta nõndaviisi ajas rändamist jätkab, jõuavad varsti ka detsember ja november veel kätte.. näis :) Loota ju võib.

Näiteks BWLPG & AGAS ongi juba kohal, ei pea enam ootma ja lootma! ;]

Näiteks BWLPG & AGAS ongi juba kohal, ei pea enam ootma ja lootma! ;]

Kõrge gaasi ega nafta hind ei soosi tankereid. Odavam hind, suurem nõudlus.

Hetkel on kõrgem hind, kuna piiratud pakkumine, mitte hull nõudlus.

Gaasikaid peaks LPG sektoris kõvasti üle olema, mainisin seda juba kevade poole.

Nafta tankerid tiksuvad tasudega alla 10K päevas, samas madala väävliga kütus kallis.

Hetkel on kõrgem hind, kuna piiratud pakkumine, mitte hull nõudlus.

Gaasikaid peaks LPG sektoris kõvasti üle olema, mainisin seda juba kevade poole.

Nafta tankerid tiksuvad tasudega alla 10K päevas, samas madala väävliga kütus kallis.

TNK vahepeal tulemused, päris valus q3 tulemas.

Siia teemasse hakkab rohkem elu tulema, et kevadel ma juba teadsin, et see pidu on läbi, lihtsalt uskumatult kaua on turg midagi lootnud- ala mega nõudlus. Kõnedest käis (Teekay) läbi, et vanad laevad jne , küsiti, kas te ei plaani oma vanu rauaks müüa, rekord kõrged metalli hinnad- vastus NO WAY. Ehk igas presekas, kus näete, laevad +20 vanad, siis reaalselt loodetakse veel taastumist ja reaalne põhi pole käes.

Kui tankerid sinna jõuavad, kus minu arvates BUY on, siis tasub vaadata Euronav või DHT poole.

NAT varsti kaasab rautselt raha, kuskil põhjas, nagu ta ikka teeb.

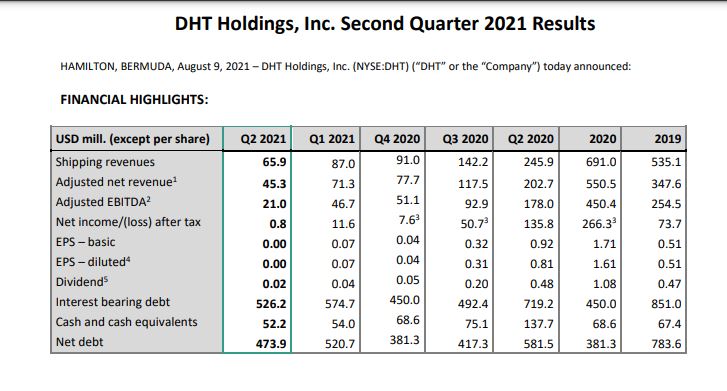

DHT tuli täna AH: Näide, kui tsükliline asi on, tabelis näha mega aastat, mis on kord 5 aasta tagant :)

Kui tankerid sinna jõuavad, kus minu arvates BUY on, siis tasub vaadata Euronav või DHT poole.

NAT varsti kaasab rautselt raha, kuskil põhjas, nagu ta ikka teeb.

DHT tuli täna AH: Näide, kui tsükliline asi on, tabelis näha mega aastat, mis on kord 5 aasta tagant :)

DHT pikendab laenu krediiti 216M, pole pahad tingimused. Kavalad firmad teevad seda alati, kui halvad ajad ees ootamas. Kindlasti kuuleb teistes ka müügi ja tagasi liisimise teemasid (kellel kehvem seis).

The new facility bears interest at a rate equal to Libor + 1.90% and has final maturity in January 2027.

The new facility bears interest at a rate equal to Libor + 1.90% and has final maturity in January 2027.

Laenu tingimused, kui hoogu on, oleks huvitav Tallinki tingimusi näha, või kellel on, kopigu siia võrdluseks vastusena.

The credit facility contains a covenant requiring that at all times the charter-free market value of the vessels that

secure the credit facility be no less than 135% of borrowings. Also, DHT covenants that, throughout the term of the

credit facility, DHT, on a consolidated basis, shall maintain:

• Value adjusted* tangible net worth of $300 million

• Value adjusted* tangible net worth shall be at least 25% of value adjusted total assets

• Unencumbered consolidated cash of at least the higher of (i) $30 million and (ii) 6% of our gross interestbearing deb

Seoses selle 30M cashiga, siis ei usu, et edaspdi on võimalik aktsiad tagasi osta ja kui tasud ei tõuse, peaks hind hakkama soodsamas suunas vajuma.

The credit facility contains a covenant requiring that at all times the charter-free market value of the vessels that

secure the credit facility be no less than 135% of borrowings. Also, DHT covenants that, throughout the term of the

credit facility, DHT, on a consolidated basis, shall maintain:

• Value adjusted* tangible net worth of $300 million

• Value adjusted* tangible net worth shall be at least 25% of value adjusted total assets

• Unencumbered consolidated cash of at least the higher of (i) $30 million and (ii) 6% of our gross interestbearing deb

Seoses selle 30M cashiga, siis ei usu, et edaspdi on võimalik aktsiad tagasi osta ja kui tasud ei tõuse, peaks hind hakkama soodsamas suunas vajuma.

Tallink

Laen ca 700M (2 kvartal 2021)

31. detsember 2020 seisuga on laevade väärtus konsolideeritud finantsseisundi aruandes summas 1 134 564 tuhat eurot.

1. Pankadega sõlmitud laenulepingutes on kontsern nõustunud vastavalt lepingu eritingimustele tagama teatud omakapitali, likviidsuse ning muude suhtarvude taseme. (mina find käsuga ei leidnud, saladus, põhjendus varjamiseks, mis nägin, et neid ennem pole vaja läinud ja ju ei lähe ka edaspidi ja me ei avalda). DHT laenud ka valdavalt põhjala pankadest. Teada on, et aktsiatega lapitakse, aga investorile ei öelda, mida.

2. Laevasid pole alla hinnatud, nende väärtus =soetus - amort. Pangad nõuavad market value ja eeldaks 135% siia.

3. Omakapital väiksem, kui laen (eks see ka karjub)

Laen ca 700M (2 kvartal 2021)

31. detsember 2020 seisuga on laevade väärtus konsolideeritud finantsseisundi aruandes summas 1 134 564 tuhat eurot.

1. Pankadega sõlmitud laenulepingutes on kontsern nõustunud vastavalt lepingu eritingimustele tagama teatud omakapitali, likviidsuse ning muude suhtarvude taseme. (mina find käsuga ei leidnud, saladus, põhjendus varjamiseks, mis nägin, et neid ennem pole vaja läinud ja ju ei lähe ka edaspidi ja me ei avalda). DHT laenud ka valdavalt põhjala pankadest. Teada on, et aktsiatega lapitakse, aga investorile ei öelda, mida.

2. Laevasid pole alla hinnatud, nende väärtus =soetus - amort. Pangad nõuavad market value ja eeldaks 135% siia.

3. Omakapital väiksem, kui laen (eks see ka karjub)

DHT tulemustest, see kehtib kõikide laevade ja aktsiate kohta, et mida jälgida- katalüsaatorid.

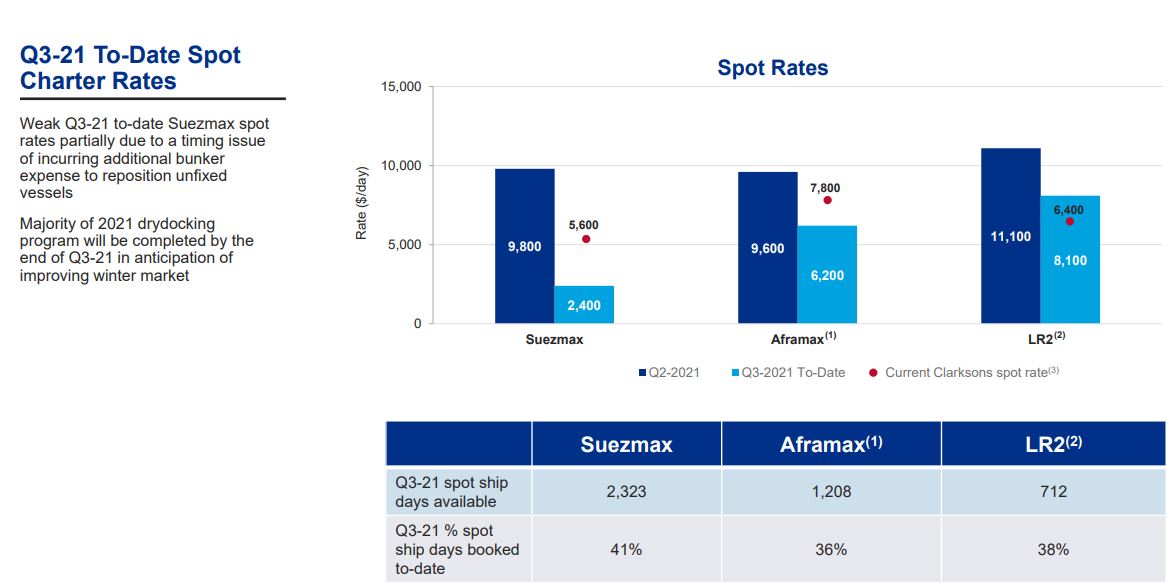

TANKER MARKET & OUTLOOK

A recovery in the tanker cycle has continued to be deferred during the second quarter of 2021. Freight markets remained difficult driven by three key factors. Firstly, long awaited oil production rises has not translated into sustainable increases in global crude exports. This is mainly from OPEC+ tapering production cuts and non-OPEC nations (e.g. Brazil & US shale) responding to higher crude prices. Secondly, persistent localized outbreaks of Covid-19 have continued to curb economic activity, thus slowing the return to the full pre-covid oil-demand. This is particularly the case for Jet Fuel demand. Thirdly, available tonnage, whilst not increasing, has remained stubbornly elevated in particular in key export markets like the Middle East.

The anticipated timeline of Iran’s return to global oil markets has also been pushed back. Crude tanker markets would benefit from a resolution of this situation via (1) a return of additional barrels to the commercial sector and (2) increasing pressure to exit the market on those (largely elderly) VLCC/Suezmax tankers engaged in illicit trading activity in recent years.

However, there are a number of improving elements building foundations for future recovery. Asset prices continued to rise – VLCC and Suezmax newbuild prices rising 9% during Q2 alone, as steel prices hit their highest level since August 2008. Recycling also accelerated during the second quarter – year to date 9 VLCCs have exited the global fleet – more than double of the total amount in 2020. The number of phase out candidates continues to accumulate, with 9% of the VLCC fleet for instance already over 20 years of age. Elevated recycle values based on high steel prices, rising bunker prices for higher consuming older tonnage and upcoming emissions regulations, should incentivize more phasing out going forward.

Further pockets of encouragement come from the level of global onshore oil inventories returning to the five-year pre-Covid-19 average. This is an important building block required for tanker market recovery to generate volume demand for crude imports/exports and therefore tanker employment. During the recent quarter there has been a sustained rise in Middle East cargoes, with June’s tanker cargo count in the region being the highest since December 2020. Toward the end of Q2 this was reducing the surplus tonnage in the region.

Higher demand for crude is assumed as economies re-open from Covid-19 restrictions. Economic agencies (IEA/EIA) both expect global demand to be just 1 million bpd below the pre-Covid-19 peak by the fourth quarter of 2021. Strong oil production growth – historically a key driver for tanker ton-miles – is therefore required to meet this anticipated 3-4 million bpd forecast demand increase during the second half of 2021.

The eventual agreement within the OPEC+ coalition to begin increasing production by 400,000 bpd starting this month, could see an additional 2 million barrels in circulation by the year end – with 1 million bpd in crude exports requiring on average 30 VLCCs to transport them. The target to end the entire 5.8 million bpd production cuts by September 2022, if enacted, is particularly encouraging.

These two interlinked factors, demand for and supply of crude, remain the key variables for tanker markets short term. Visibility on demand remains limited. Rising crude demand has largely been and led by OECD nations (US & Europe) where vaccination rates have been highest. Full emerging market engagement (limited due to lower vaccination rates) and international travel (restrictions on movement) remain limited in demand contribution. Increases in production need to translate more fully into exported barrels. Both factors are required to move into equilibrium with one another before freight rates can gain upward traction and prevent the (already high) oil price to move to levels where it could curtail demand. In addition, the recent ramping up of climate change regulations is a structural feature for the tanker market to manage over the medium term.

TANKER MARKET & OUTLOOK

A recovery in the tanker cycle has continued to be deferred during the second quarter of 2021. Freight markets remained difficult driven by three key factors. Firstly, long awaited oil production rises has not translated into sustainable increases in global crude exports. This is mainly from OPEC+ tapering production cuts and non-OPEC nations (e.g. Brazil & US shale) responding to higher crude prices. Secondly, persistent localized outbreaks of Covid-19 have continued to curb economic activity, thus slowing the return to the full pre-covid oil-demand. This is particularly the case for Jet Fuel demand. Thirdly, available tonnage, whilst not increasing, has remained stubbornly elevated in particular in key export markets like the Middle East.

The anticipated timeline of Iran’s return to global oil markets has also been pushed back. Crude tanker markets would benefit from a resolution of this situation via (1) a return of additional barrels to the commercial sector and (2) increasing pressure to exit the market on those (largely elderly) VLCC/Suezmax tankers engaged in illicit trading activity in recent years.

However, there are a number of improving elements building foundations for future recovery. Asset prices continued to rise – VLCC and Suezmax newbuild prices rising 9% during Q2 alone, as steel prices hit their highest level since August 2008. Recycling also accelerated during the second quarter – year to date 9 VLCCs have exited the global fleet – more than double of the total amount in 2020. The number of phase out candidates continues to accumulate, with 9% of the VLCC fleet for instance already over 20 years of age. Elevated recycle values based on high steel prices, rising bunker prices for higher consuming older tonnage and upcoming emissions regulations, should incentivize more phasing out going forward.

Further pockets of encouragement come from the level of global onshore oil inventories returning to the five-year pre-Covid-19 average. This is an important building block required for tanker market recovery to generate volume demand for crude imports/exports and therefore tanker employment. During the recent quarter there has been a sustained rise in Middle East cargoes, with June’s tanker cargo count in the region being the highest since December 2020. Toward the end of Q2 this was reducing the surplus tonnage in the region.

Higher demand for crude is assumed as economies re-open from Covid-19 restrictions. Economic agencies (IEA/EIA) both expect global demand to be just 1 million bpd below the pre-Covid-19 peak by the fourth quarter of 2021. Strong oil production growth – historically a key driver for tanker ton-miles – is therefore required to meet this anticipated 3-4 million bpd forecast demand increase during the second half of 2021.

The eventual agreement within the OPEC+ coalition to begin increasing production by 400,000 bpd starting this month, could see an additional 2 million barrels in circulation by the year end – with 1 million bpd in crude exports requiring on average 30 VLCCs to transport them. The target to end the entire 5.8 million bpd production cuts by September 2022, if enacted, is particularly encouraging.

These two interlinked factors, demand for and supply of crude, remain the key variables for tanker markets short term. Visibility on demand remains limited. Rising crude demand has largely been and led by OECD nations (US & Europe) where vaccination rates have been highest. Full emerging market engagement (limited due to lower vaccination rates) and international travel (restrictions on movement) remain limited in demand contribution. Increases in production need to translate more fully into exported barrels. Both factors are required to move into equilibrium with one another before freight rates can gain upward traction and prevent the (already high) oil price to move to levels where it could curtail demand. In addition, the recent ramping up of climate change regulations is a structural feature for the tanker market to manage over the medium term.

Analüütikud rikuvad korraks peo ära, endal plaan oli 5$ juurest osta

DHT Holdings upgraded to Buy from Hold at Stifel 18:53 DHT Stifel analyst Benjamin Nolan upgraded DHT Holdings to Buy from Hold with a $7 price target.

DHT Holdings upgraded to Buy from Neutral at H.C. Wainwright 06:07 DHT H.C. Wainwright analyst Magnus Fyhr upgraded DHT Holdings to Buy from Neutral with a price target of $8, up from $7.50. The shares are down 14% during the past month, leaving the stock trading at a 24% discount to net asset value, which has created "an attractive entry point," argues Fyhr. He views DHT as well positioned to capitalize on a tanker market recovery with its "high-quality fleet of 26 VLCC tankers and a strong balance sheet," Fyhr tells investors.

Read more at:

https://thefly.com/n.php?id=3355049

DHT Holdings upgraded to Buy from Hold at Stifel 18:53 DHT Stifel analyst Benjamin Nolan upgraded DHT Holdings to Buy from Hold with a $7 price target.

DHT Holdings upgraded to Buy from Neutral at H.C. Wainwright 06:07 DHT H.C. Wainwright analyst Magnus Fyhr upgraded DHT Holdings to Buy from Neutral with a price target of $8, up from $7.50. The shares are down 14% during the past month, leaving the stock trading at a 24% discount to net asset value, which has created "an attractive entry point," argues Fyhr. He views DHT as well positioned to capitalize on a tanker market recovery with its "high-quality fleet of 26 VLCC tankers and a strong balance sheet," Fyhr tells investors.

Read more at:

https://thefly.com/n.php?id=3355049

Euronavi kõne ka läbi, siit tuli huvitav fakt, miks laevade üle küllus. Nimelt 50 vana laeva pole jõudnud vana rauda vaid veavad illegaalset kütust Iraanist ja Venetsueelast.

Ei usu, et põhi käes veel. Q3 traditsiooni järgi on üks halvemaid kuid, ehk lükkab see rohkem vanarauda.

Ei usu, et põhi käes veel. Q3 traditsiooni järgi on üks halvemaid kuid, ehk lükkab see rohkem vanarauda.

Täna oli hea päev ja homme loodetavasti tuleb veel parem. Capesize, VLCC, VLGC indeksid üles, aktsiad alla.. nii jätka ;-)

Toomas, mis need tasud hetkel on?

Kui Hiina jahtub, väheneb nõudlus kütuse järel, ning see ei mõju hindadele hästi. Maismaa laod tühjad, sinna saab toppida hetkel küll ja veel ning normaalsetest tasudest nähakse hetkel und- sõidetakse endiselt kahjumiga. Kui kedagi põhjast kraapida, siis DHT või EURN. Hetkel ei ole aktsia hind soodne. Pakuks - 1$ kukkumist ennem nende hindadel.

Kui Hiina jahtub, väheneb nõudlus kütuse järel, ning see ei mõju hindadele hästi. Maismaa laod tühjad, sinna saab toppida hetkel küll ja veel ning normaalsetest tasudest nähakse hetkel und- sõidetakse endiselt kahjumiga. Kui kedagi põhjast kraapida, siis DHT või EURN. Hetkel ei ole aktsia hind soodne. Pakuks - 1$ kukkumist ennem nende hindadel.

Capesize oli 4304, kõik muu oli ilusti veeall nagu sa ütlesid. Ma ei ole kahjuks eriti osav põhja kraapimises ning seeõttu siiralt loodan, et sul on õigus ja täiendav kukkumine on veel ees mitte seljataga.

Ma ise jälgin ainult tankereid, aga ega täpset põhja tea, vahel turul püsib lootus kauem kui mõistlik.

Näiteks kui tankeri omanikud endiselt liiga positiivselt meelestatud , (kuigi veohinnad ala 5000 ja tasuvuse punkt 20 000$) siis ei müüda 20a laevu ära vanarauda ja ikka veo hinnad püsivad madalal.

Näiteks kui tankeri omanikud endiselt liiga positiivselt meelestatud , (kuigi veohinnad ala 5000 ja tasuvuse punkt 20 000$) siis ei müüda 20a laevu ära vanarauda ja ikka veo hinnad püsivad madalal.

Üürike oli mu õnn, täna:

Baltic #Capesize index +5% to $56k/d

Brazil/China +6% to $47k/d

Oct FFA +8% to $46k/d

Kahjuks aktsiad jätkasid tõusu. GOGL.OL tegi päeva lõpus ilusa jõnksu alla, samas US open läks +4.4% seega.. ma ei tea, vaatab kas homsel hommikul õnnestub samast kohast jätkata.

Re: VLCC, VLGC: spot endiselt veeall, aktsiad teel üles. Positiivne meelestatus :)

Baltic #Capesize index +5% to $56k/d

Brazil/China +6% to $47k/d

Oct FFA +8% to $46k/d

Kahjuks aktsiad jätkasid tõusu. GOGL.OL tegi päeva lõpus ilusa jõnksu alla, samas US open läks +4.4% seega.. ma ei tea, vaatab kas homsel hommikul õnnestub samast kohast jätkata.

Re: VLCC, VLGC: spot endiselt veeall, aktsiad teel üles. Positiivne meelestatus :)

Uus LA juures passivate, laadimist ootavate konteineri-laevade rekord: 65, kondiveohinnad u. 10x, võrreldes 2019 a.

www.bbc.com/news/business-58643717

www.bbc.com/news/business-58643717

Või noh x10 on väikeklientidele Eestist. Suurklientidelegi julmalt hind tõusnud.

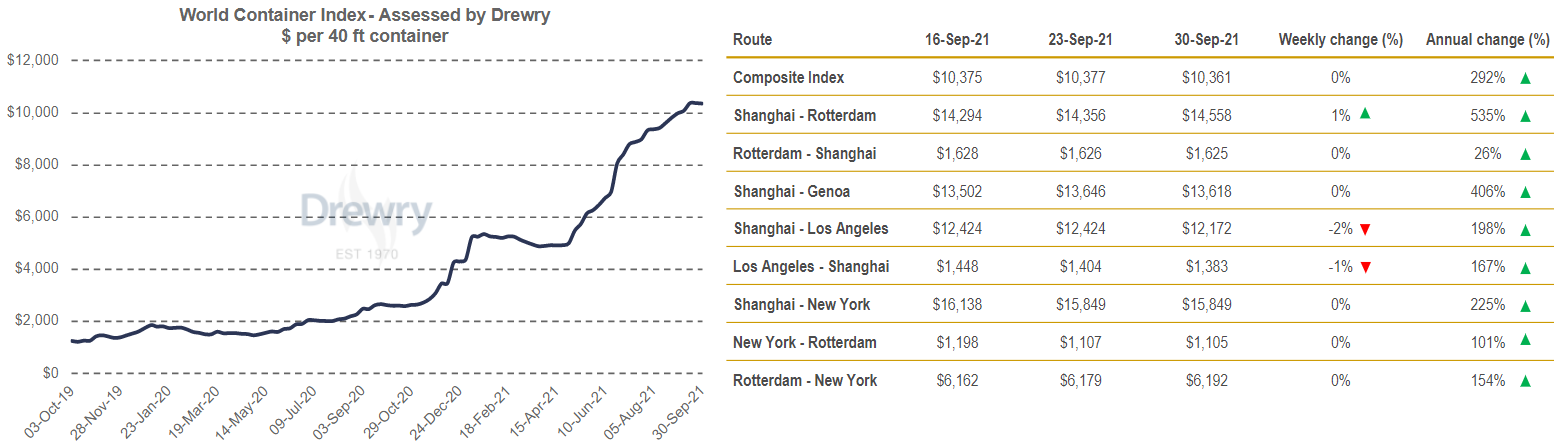

Composite World Container index inched down by 0.2% to $10,360.87 per 40ft container this week, but remains 291.8% higher than a year ago. Avg composite index of the WCI, assessed by Drewry for year-to-date, is $6,977 per 40ft container, which is $4,547 higher than the five-year average of $2,430 per 40ft container.

Shanghai to LA dropped 2% or $252 to reach $12,172 per 40ft box. Similarly, rates on LA – Shanghai fell 1% or $21 to reach $1,383 per 40ft container. However, rates on Shanghai – Rotterdam nudged up by 1% or $202 and stood at $14,558 per feu. Rates on Rotterdam-Shanghai, Shanghai-Genoa, Shanghai-New York and Rotterdam-New York keeps hovering around previous weeks level.

Composite World Container index inched down by 0.2% to $10,360.87 per 40ft container this week, but remains 291.8% higher than a year ago. Avg composite index of the WCI, assessed by Drewry for year-to-date, is $6,977 per 40ft container, which is $4,547 higher than the five-year average of $2,430 per 40ft container.

Shanghai to LA dropped 2% or $252 to reach $12,172 per 40ft box. Similarly, rates on LA – Shanghai fell 1% or $21 to reach $1,383 per 40ft container. However, rates on Shanghai – Rotterdam nudged up by 1% or $202 and stood at $14,558 per feu. Rates on Rotterdam-Shanghai, Shanghai-Genoa, Shanghai-New York and Rotterdam-New York keeps hovering around previous weeks level.

Ja MPCC teeb mida, müüb kuni veel keegi ostab?!