Henkelilt ootuspärane käive ja veidi parem ärikasum. Prognoosid jäid samaks.

• Henkel adj. EBIT excluding one-time items EU854m, est. EU837m (+13.8% YoY)

• Sales EU5.06b, est. EU5.04b (+13.6% YoY, organic 4.0%)

• Confirms outlook

• Still sees organic sales growth of 2% - 4%

• Still sees EPS increase between 7% - 9%

• Still sees EBIT margin more than 17%

Chemours on saanud viimasel ajal päris mitu upgrade'i kasumipotentsiaali suurenemise tõttu, sest kui varasemalt jälgiti ettevõtte puhul rohkem titaandioksiidi turgu, siis nüüd tuuakse veel välja arvatust menukamat jahutussegu Opteon.

JPMorgan analyst Jeffrey Zekauskas, who upgraded Chemours to Overweight from Neutral on Friday, sees more upside ahead. The reason: Chemours is producing a new kind of coolant—its brand name is Opteon—that contributes less to global warming than standard refrigerants.

As of now, Zekauskas explains in a note to clients, only Chemours and Honeywell International (HON) make this type of coolant, which could see demand from auto-part makers in the U.S. and Europe, as well as from other, non-auto companies. That would be great news for Chemours because Opteon costs more than standard coolants, so a sales pickup would boost profit margins.

JPMorgan analyst Jeffrey Zekauskas, who upgraded Chemours to Overweight from Neutral on Friday, sees more upside ahead. The reason: Chemours is producing a new kind of coolant—its brand name is Opteon—that contributes less to global warming than standard refrigerants.

As of now, Zekauskas explains in a note to clients, only Chemours and Honeywell International (HON) make this type of coolant, which could see demand from auto-part makers in the U.S. and Europe, as well as from other, non-auto companies. That would be great news for Chemours because Opteon costs more than standard coolants, so a sales pickup would boost profit margins.

Easyjeti esimese poolaasta käive kasvas aastaga 3,2% 1,83 miljardi naelani, mida oli oodatust veidi vähem ning samuti kujunes maksueelne kahjum arvatust suuremaks, olles mõjutatud lihavõtete liikumisest teise poolaastasse (ca 45 miljonit naela) ning negatiivsest valuutaliikumisest (82 miljonit naela). Teise poolaasta osas ollakse optimistlikud, tänu millele loodetakse kogu majandusaasta osas saavutada konsensuse 371 miljoni naela suurust maksueelse kasumi ootust (mullu 498 mln naela).

•Rev. GBP1.83b vs GBP1.77b, co. says in statement; est. GBP1.88b

• Revenue/seat fell 4.9% to GBP48.80

•Headline cost per seat excluding fuel at constant currency flat at £38.54, reflecting strong cost control despite high levels of disruption

•1H Pretax Loss GBP236m; Est. GBP176m Loss

• Net loss GBP192m vs GBP15m; est. GBP135.7m

• Basic EPS loss 48.9 pence; est. 32 pence

"Looking ahead, we are seeing an improving revenue per seat trend as well as the continued reduction of competitor capacity growth. Cost performance for the full year will continue to be strong"

•Rev. GBP1.83b vs GBP1.77b, co. says in statement; est. GBP1.88b

• Revenue/seat fell 4.9% to GBP48.80

•Headline cost per seat excluding fuel at constant currency flat at £38.54, reflecting strong cost control despite high levels of disruption

•1H Pretax Loss GBP236m; Est. GBP176m Loss

• Net loss GBP192m vs GBP15m; est. GBP135.7m

• Basic EPS loss 48.9 pence; est. 32 pence

"Looking ahead, we are seeing an improving revenue per seat trend as well as the continued reduction of competitor capacity growth. Cost performance for the full year will continue to be strong"

Ei ole välistatud, et kunagi ostetakse Amazonist ka ravimeid

Amazon is hiring people to break into the multibillion-dollar pharmacy market

Amazon is hiring people to break into the multibillion-dollar pharmacy market

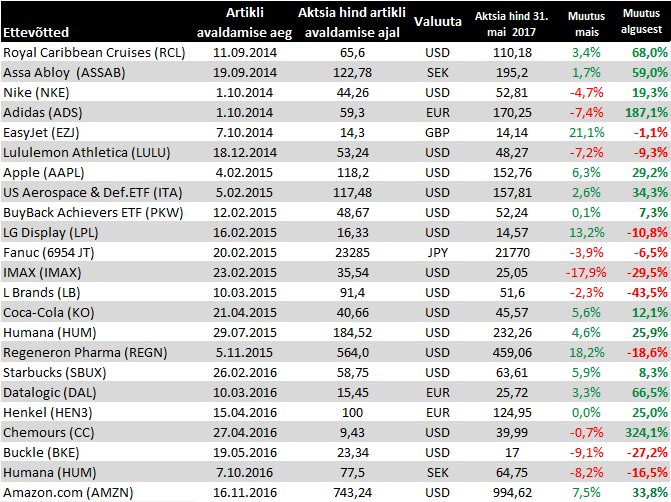

31. mai seisuga

Lululemon suutis lõpetada esimese kvartali paremate tulemustega, kui neljanda lõpus hoiatati. Mäletatavasti toodi toona välja puuduseid kollektsioonis, mis viisid võrreldava müügi langusesse. Teiseks kvartaliks oodatav võrreldava müügi taastumine pakub investoritele ilmselt lohutust, kuna viitab, et probleemile on suudetud lahendus leida. Majandusaasta kasumiootust tõstetakse suuremate investeeringute tõttu siiski vaid kahe sendi võrra.

Lululemon reports Q1 (Apr) earnings of $0.32 per share, $0.04 better than the Capital IQ Consensus of $0.28; revenues rose 5.0% year/year to $520.3 mln vs the $513.99 mln Capital IQ Consensus. Total comparable sales decreased 1%, or decreased by 1% on a constant dollar basis.

Sees 2Q Comps up in Low-to-Mid Single Digits Constant FX

Co issues in-line guidance for FY18, sees EPS of $2.28-2.38, excluding non-recurring items, vs. $2.31 Capital IQ Consensus Estimate; sees FY18 revs of $2.53-2.58 bln vs. $2.56 bln Capital IQ Consensus Estimate.

Lululemon reports Q1 (Apr) earnings of $0.32 per share, $0.04 better than the Capital IQ Consensus of $0.28; revenues rose 5.0% year/year to $520.3 mln vs the $513.99 mln Capital IQ Consensus. Total comparable sales decreased 1%, or decreased by 1% on a constant dollar basis.

Sees 2Q Comps up in Low-to-Mid Single Digits Constant FX

Co issues in-line guidance for FY18, sees EPS of $2.28-2.38, excluding non-recurring items, vs. $2.31 Capital IQ Consensus Estimate; sees FY18 revs of $2.53-2.58 bln vs. $2.56 bln Capital IQ Consensus Estimate.

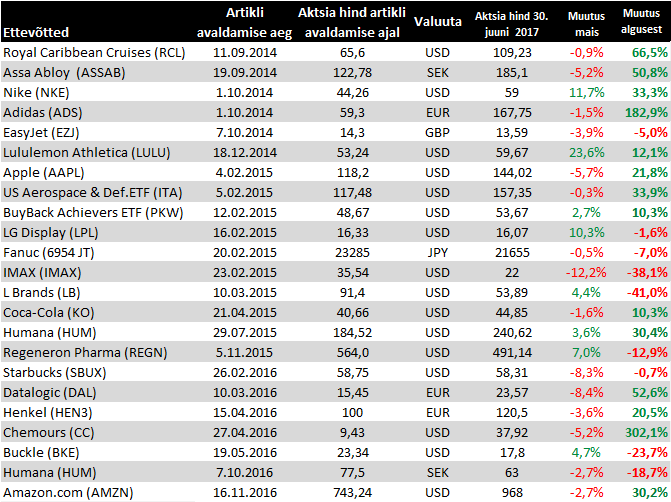

30. juuni seisuga

Easyjet teatas, et seitse aasat firmat juhtinud Carolyn McCall liigub järgmisest aastast ITV etteotsa. Bernsteini arvates pole see küll hea uudis, kuid ei tohiks luua ka materiaalset negatiivset riski.

* Successor CEO from outside company may be preferable, would offer fresh view

* Priorities of new CEO should be continuing strategy to increase market share in airline’s largest European bases; improve operationally including better on-time flight performance; and increase focus on costs

* Successor CEO from outside company may be preferable, would offer fresh view

* Priorities of new CEO should be continuing strategy to increase market share in airline’s largest European bases; improve operationally including better on-time flight performance; and increase focus on costs

Kui vahepeal jõudis Assa Abloy puhul mure Aasia müügitulemuste, eeskätt Hiina, puhul leeveneda, siis pärast teise kvartali oodatust nõgemaid numbreid on see uuesti esiplaanil.

* 2Q sales SEK19.4 billion, estimate SEK19.81 billion (range SEK19.59 billion to SEK20.17 billion)

* 2Q Ebit SEK3.11 billion, estimate SEK3.21 billion (range SEK3.15 billion to SEK3.27 billion)

* Global Eco. Trend Has Improved to Some Degree Y/Y

* Positive Trend on Most Mkts in North, S. America

* Positive Trend Also in Parts of Europe

* Trend Weak on Some Mkts in Asia, Middle East

* Expansion Strategy, Even on Emerging Mkts, Unchanged

* Sales in Northam Continued to Develop Well

* China sales Fell Again; Fell in Brazil, Middle East

* 2Q sales SEK19.4 billion, estimate SEK19.81 billion (range SEK19.59 billion to SEK20.17 billion)

* 2Q Ebit SEK3.11 billion, estimate SEK3.21 billion (range SEK3.15 billion to SEK3.27 billion)

* Global Eco. Trend Has Improved to Some Degree Y/Y

* Positive Trend on Most Mkts in North, S. America

* Positive Trend Also in Parts of Europe

* Trend Weak on Some Mkts in Asia, Middle East

* Expansion Strategy, Even on Emerging Mkts, Unchanged

* Sales in Northam Continued to Develop Well

* China sales Fell Again; Fell in Brazil, Middle East

Kuigi easyJeti kolmanda kvartali müügitulu osutus antud prognoosist paremaks ning kogu majandusaasta väljavaadet kergitati, näitab aktsia negatiivne reaktsioon, et investorite ootused olid väärtpaberi eelnevate kuude rallit arvestades kõrgemad

EasyJet reported 3Q revenue GBP1.39b vs GBP1.2b yr ago and forecast FY17 pretax profit GBP380m to GBP420m. Bloomberg average estimated for FY17 pretax is GBP375m.

CEO Carolyn McCall said: “"Although we expect capacity to continue to put pressure on yields, our progress this year has enabled us to upgrade this year’s PBT forecast”

EasyJet reported 3Q revenue GBP1.39b vs GBP1.2b yr ago and forecast FY17 pretax profit GBP380m to GBP420m. Bloomberg average estimated for FY17 pretax is GBP375m.

CEO Carolyn McCall said: “"Although we expect capacity to continue to put pressure on yields, our progress this year has enabled us to upgrade this year’s PBT forecast”

Morgan Stanley usub, et Nike on USA äri ümber pööramas ning tõstab soovituse overweight peale hinnasihiga 68 dollarit (varem neutraalne ja 56).

We think the window to buy Nike at the bottom of a cycle is closing. Nike EPS and North America sales growth rates are likely troughing. Plus, Nike’s major supply chain innovations may be about to catalyze a multi-year margin expansion story. We see a very favorable 3:1 risk/reward.

We think the window to buy Nike at the bottom of a cycle is closing. Nike EPS and North America sales growth rates are likely troughing. Plus, Nike’s major supply chain innovations may be about to catalyze a multi-year margin expansion story. We see a very favorable 3:1 risk/reward.

Viimasel ajal ei möödu vist ühte päeva ka, kui Amazon jälle mõne müüki toetava teenusega välja ei tuleks

Amazon launches new shopping platform Spark - shoppable photo feed

Amazon launches new shopping platform Spark - shoppable photo feed

Coca-Colalt üsna ootuspärased numbrid ja prognoos

Reports Q2 (Jun) earnings of $0.59 per share, excluding non-recurring items, $0.02 better than the Capital IQ Consensus of $0.57; revenues fell 15.9% year/year to $9.7 bln vs the $9.62 bln Capital IQ Consensus

Co issues in-line guidance for FY17, sees EPS flat to down 2% to $1.87-1.91 (from down 1-3%), excluding non-recurring items, vs. $1.88 Capital IQ Consensus; ~3% growth in organic revenues (non-GAAP) -- No Change

Reports Q2 (Jun) earnings of $0.59 per share, excluding non-recurring items, $0.02 better than the Capital IQ Consensus of $0.57; revenues fell 15.9% year/year to $9.7 bln vs the $9.62 bln Capital IQ Consensus

Co issues in-line guidance for FY17, sees EPS flat to down 2% to $1.87-1.91 (from down 1-3%), excluding non-recurring items, vs. $1.88 Capital IQ Consensus; ~3% growth in organic revenues (non-GAAP) -- No Change

Sarnaselt konkurentidele raporteeris ka Adidas tugevad esialgsed teise kvartali numbrid, mille baasil kergitati prognoose. Täpsemad tulemused 3. augustil.

Due to the strong first half year performance, the company has increased its 2017 financial outlook. Management now projects currency-neutral sales to grow at a rate between 17% and 19% in 2017 (previously: to increase by between 12% and 14% compared to the adjusted 2016 net sales of € 18.483 billion for the company’s continuing operations). Furthermore, the company forecasts a year-over-year gross margin improvement during the second half of 2017 and expects to continue to generate operating leverage throughout the remainder of the year. As a result, net income from continuing operations is now forecasted to increase at a rate between 26% and 28% in 2017 to a level between € 1.360 billion and € 1.390 billion. This compares to the original guidance as provided in March of an increase of between 13% and 15% to a level between € 1.200 billion and € 1.225 billion for the company’s net income from continuing operations..

Due to the strong first half year performance, the company has increased its 2017 financial outlook. Management now projects currency-neutral sales to grow at a rate between 17% and 19% in 2017 (previously: to increase by between 12% and 14% compared to the adjusted 2016 net sales of € 18.483 billion for the company’s continuing operations). Furthermore, the company forecasts a year-over-year gross margin improvement during the second half of 2017 and expects to continue to generate operating leverage throughout the remainder of the year. As a result, net income from continuing operations is now forecasted to increase at a rate between 26% and 28% in 2017 to a level between € 1.360 billion and € 1.390 billion. This compares to the original guidance as provided in March of an increase of between 13% and 15% to a level between € 1.200 billion and € 1.225 billion for the company’s net income from continuing operations..

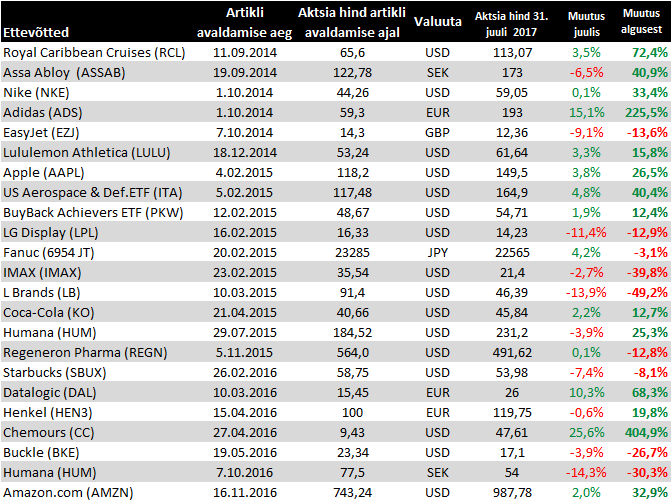

Muutused 31. juuli seisuga

Royal Caribbean raporteerib üsna ootuspärase müügitulu juures veidi parema aktsiakasumi ning tõstab prognoose

Reports Q2 (Jun) earnings of $1.71 per share, $0.04 better than the Capital IQ Consensus of $1.67 and above prior guidance of $1.60-1.65; revenues rose 4.3% year/year to $2.20 bln vs the $2.19 bln Capital IQ Consensus.

Co issues upside guidance for Q3, sees EPS of approx $3.45, excluding non-recurring items, vs. $3.30 Capital IQ Consensus Estimate.

Co issues upside guidance for FY17, sees EPS of approx $7.35-7.45, excluding non-recurring items, vs. $7.25 Capital IQ Consensus Estimate and vs prior guidance of $7.00-7.20

"Our brands are executing beautifully, keeping the business in an exceptionally strong position...Strong close-in demand for cruise bolstered the quarter, and we see further uplift for the balance of the year, positioning us well for the Double-Double and beyond.".

Reports Q2 (Jun) earnings of $1.71 per share, $0.04 better than the Capital IQ Consensus of $1.67 and above prior guidance of $1.60-1.65; revenues rose 4.3% year/year to $2.20 bln vs the $2.19 bln Capital IQ Consensus.

Co issues upside guidance for Q3, sees EPS of approx $3.45, excluding non-recurring items, vs. $3.30 Capital IQ Consensus Estimate.

Co issues upside guidance for FY17, sees EPS of approx $7.35-7.45, excluding non-recurring items, vs. $7.25 Capital IQ Consensus Estimate and vs prior guidance of $7.00-7.20

"Our brands are executing beautifully, keeping the business in an exceptionally strong position...Strong close-in demand for cruise bolstered the quarter, and we see further uplift for the balance of the year, positioning us well for the Double-Double and beyond.".

Käesoleva aasta alguses Aetnaga ühinemisest taganema sunnitud USA ravikindlustuse pakkuja Humana ületab analüütikute aktsiakasumi ootust ning tõstab fiskaalaasta prognoosi

Reports Q2 (Jun) earnings of $3.49 per share, excluding non-recurring items, $0.42 better than the Capital IQ Consensus of $3.07.

Co issues upside guidance for FY17, raises EPS to ~$11.50 from $at least $11.10, excluding non-recurring items, vs. $11.15 Capital IQ Consensus Estimate.

The increases in FY17 guidance for both GAAP and Adjusted EPS were primarily driven by the strong results in the Retail segment, largely attributable to the company's individual Medicare Advantage business, partially offset by lower than expected Healthcare Services segment pretax income due to lower than anticipated pharmacy utilization and the continued optimization of our chronic care management programs. The individual Medicare Advantage business is exceeding its operational targets, experiencing lower than anticipated utilization, higher than expected revenue on a per member basis and favorable medical fee-for-service claims reserve development (Prior Period Development).

Reports Q2 (Jun) earnings of $3.49 per share, excluding non-recurring items, $0.42 better than the Capital IQ Consensus of $3.07.

Co issues upside guidance for FY17, raises EPS to ~$11.50 from $at least $11.10, excluding non-recurring items, vs. $11.15 Capital IQ Consensus Estimate.

The increases in FY17 guidance for both GAAP and Adjusted EPS were primarily driven by the strong results in the Retail segment, largely attributable to the company's individual Medicare Advantage business, partially offset by lower than expected Healthcare Services segment pretax income due to lower than anticipated pharmacy utilization and the continued optimization of our chronic care management programs. The individual Medicare Advantage business is exceeding its operational targets, experiencing lower than anticipated utilization, higher than expected revenue on a per member basis and favorable medical fee-for-service claims reserve development (Prior Period Development).

Regeneron andis eile ülevaate oma teise kvartali tulemustest, mis sisaldasid nii positiivset kui negatiivset infot. Positiivse poole pealt kasvasid Regeneroni suurima tulude allika, EYLEA müügitulud y-o-y 11% ning ühtekokku tõi ravim kvartali jooksul sisse $919 miljonit tulusid. Samuti kasvas non-GAAP kasum ligi 48%, ületades sellega selgelt analüütikute oodatud 11% kasvumäära. Samal ajal jäid kahe uue ravimi, kvartali jooksul turule toodud Kevzara ja Dupixenti tulud esialgu tagasihoidlikuks ning ka juba möödunud aastal turule toodud Praluenti tulud on endiselt allapoole ootusi. Nii Kevzarast kui Dupixentist oodatakse märksa suuremat tuge EYLEA’le, mille tulud peaksid lähiaastatel paljuski oma potentsiaali tipu saavutama.

Lisaks teatas Regeneron, et aasta lõpus aeguvat koostöölepingut teadus- ja arendustööks Sanofiga ei pikendata, mis ühelt poolt tähendab Sanofilt saadud iga-aastase rahasüsti lõppemist, teisalt aga võimaldab Regeneronil edaspidi turule toodavaid ravimeid turustada vabalt valitud partneritega või võtta kogu vastutus (ja tulud) enda kanda.

Lisaks teatas Regeneron, et aasta lõpus aeguvat koostöölepingut teadus- ja arendustööks Sanofiga ei pikendata, mis ühelt poolt tähendab Sanofilt saadud iga-aastase rahasüsti lõppemist, teisalt aga võimaldab Regeneronil edaspidi turule toodavaid ravimeid turustada vabalt valitud partneritega või võtta kogu vastutus (ja tulud) enda kanda.

Datalogic andis reede õhtul oma teise kvartali tulemused. Ühtekokku oli tegemist ettevõtte senise ajaloo tugevaima kvartaliga, kus rekordkõrgustesse jõudsid nii sissetulnud tellimuste maht, müügitulutulud kui ka kasum, ehkki aasta lõikes on tavapäraselt neljas kvartal kõige tugevam.

Müügitulude kasv kiirenes Q2 +7,7%-ni (+6,4% konstantse EUR/USD juures), tellimuste arv kasvas +10,2% võrra, korrigeeritud ärikasum +11,6% ning korrigeeritud EPS +7,8%. Kasumlikkusele mõjus positiivselt tugev turuolukord, mis võimaldas eelistada kõrgema marginaaliprofiiliga tellimusi, samas kui valuutamõjud, kõrgem efektiivne maksumäär ning kõrgemad finantskulud mõjusid puhaskasumi reale negatiivselt.

Müügitulude kasv kiirenes Q2 +7,7%-ni (+6,4% konstantse EUR/USD juures), tellimuste arv kasvas +10,2% võrra, korrigeeritud ärikasum +11,6% ning korrigeeritud EPS +7,8%. Kasumlikkusele mõjus positiivselt tugev turuolukord, mis võimaldas eelistada kõrgema marginaaliprofiiliga tellimusi, samas kui valuutamõjud, kõrgem efektiivne maksumäär ning kõrgemad finantskulud mõjusid puhaskasumi reale negatiivselt.

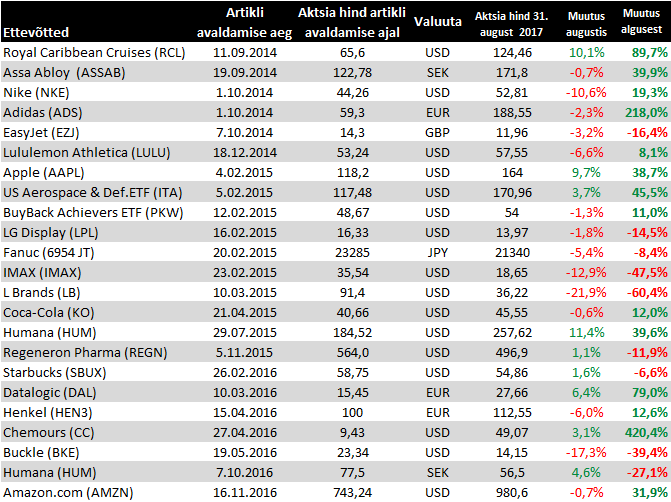

Muutused 31. augusti seisuga