Datalogicu kolmanda kvartali tulemused olid varasemate kvartalite kiire müügitulu kasvuga võrreldes tagasihoidlikumad (+4,6% y-o-y, +4,8% ilma valuutaefektideta), ehkki oma mõju sellele avaldasid ka suvekuud ning eelmise aasta tulusid oluliselt suuremaks puhunud valuutaefekti pöördumine.

Negatiivse poole pealt vajus probleemne IA segment taas nullilähedase kasvutempo ning kasumilanguse juurde, põhjustatuna peamiselt valimiste-eelsest ettevaatlikkusest USA-s.

Samal ajal püsib tugev Datalogicu kasvu vedav trend jaemüügisektoris, kuivõrd ligi 70% ettevõtte tuludest toov ADC segment näitas endiselt tugevat kasvu nii tulude (+8,4%) kui EBITDA (+24%) poolel.

easyJeti tulemused jäid oktoobris antud prognoosi lähedale. Väljavaate osas ollakse ettevaatlikud, naela ebasoodsa liikumise leevendamiseks otsitakse võimalusi muuta ettevõtte tegevust efektiivsemaks

* EasyJet full-year pretax GBP495m, est. GBP494m.

* Rev. GBP4.67b, est. GBP4.63b

* Div. 53.8p; BDVD forecast 53.2p, yr ago 55.2p

* Outlook: Reiterates cost per seat ex-fuel and at constant currency to increase by ~1% for full year; expect a mid to high single digit decline in revenue/seat in 1H; expect to increase FY capacity by up to 9%

* Avg est. current year pretax profit GBP423m

* EasyJet full-year pretax GBP495m, est. GBP494m.

* Rev. GBP4.67b, est. GBP4.63b

* Div. 53.8p; BDVD forecast 53.2p, yr ago 55.2p

* Outlook: Reiterates cost per seat ex-fuel and at constant currency to increase by ~1% for full year; expect a mid to high single digit decline in revenue/seat in 1H; expect to increase FY capacity by up to 9%

* Avg est. current year pretax profit GBP423m

Amazoni aktsia on majandustulemuste järgselt olnud müügisurve all, osaliselt kuna info investeeringute suurendamise kohta sundis kasumiootusi allapoole tooma. Saab näha, kas ka seekord jääb lõpuks peale Jeff Bezose pikaajaline strateegia ning seetõttu lisame Amazoni jälgimisnimekirja. (Investorid hülgavad Amazoni)

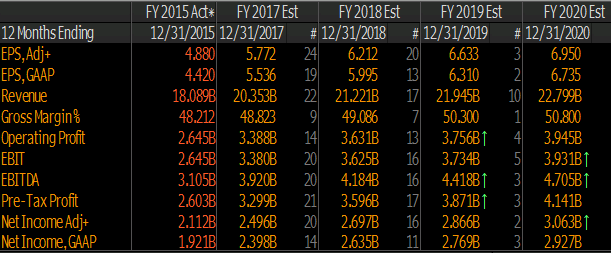

Henkel on strateegiapäeval seadnud eesmärgiks saavutada kuni 2020.a keskmiselt 2-4% orgaanilist kasvu aastas, mis ühtib suuresti analüütikute seniste ootustega

• Henkel’s financial goals for 2020:

• Organic sales growth: average 2% to 4%

• Adjusted earnings per preferred share: 7% to 9% CAGR

• Improve adjusted Ebit margin

• Expand free cash flow

• Henkel aims to generate profitable growth by focusing on 4 strategic priorities: driving growth, accelerating digitalization, increasing agility, funding growth

Konsensuse ootused:

• Henkel’s financial goals for 2020:

• Organic sales growth: average 2% to 4%

• Adjusted earnings per preferred share: 7% to 9% CAGR

• Improve adjusted Ebit margin

• Expand free cash flow

• Henkel aims to generate profitable growth by focusing on 4 strategic priorities: driving growth, accelerating digitalization, increasing agility, funding growth

Konsensuse ootused:

L Brandsi tulemused eelneva kasumihoiatuse tõttu üllatust ei valmistnaud, küll aga osutus pettumuseks vaade jooksvale kvartalile

L Brands reports Q3 (Oct) earnings of $0.42 per share, $0.02 better than the Capital IQ Consensus of $0.40 and slightly above Nov 3 guidance of approx $0.40; revenues rose 4.0% year/year to $2.58 bln vs the $2.56 bln Capital IQ Consensus and in-line with its Nov 3 guidance of $2.58 bln.

Co issues downside guidance for Q4 (Jan), sees EPS of $1.85-2.00 vs. $2.02 Capital IQ Consensus Estimate.

Comparable sales in OctQ increased +2%, in-line with Nov 3 guidance; By segment: Victoria's Secret comps -1% and Bath & Body Works comps of +7%.

L Brands reports Q3 (Oct) earnings of $0.42 per share, $0.02 better than the Capital IQ Consensus of $0.40 and slightly above Nov 3 guidance of approx $0.40; revenues rose 4.0% year/year to $2.58 bln vs the $2.56 bln Capital IQ Consensus and in-line with its Nov 3 guidance of $2.58 bln.

Co issues downside guidance for Q4 (Jan), sees EPS of $1.85-2.00 vs. $2.02 Capital IQ Consensus Estimate.

Comparable sales in OctQ increased +2%, in-line with Nov 3 guidance; By segment: Victoria's Secret comps -1% and Bath & Body Works comps of +7%.

30. novembri seisuga

Üsna ootamatult tuli eile uudis, et Starbucksi asutaja ning juht Howard Schultz astub tagasi. Kuigi teatavat määramatust see tekitab, siis võivad aktsionärid leida lohutust teadmisest, et Schultz jääb nõukogu etteotsa ning kavatseb edaspidi oma tähelepanu suunata firma high-end kohvikute arendamisele, millest ehk kuuleme lähemalt firma 7. detsembri strateegiapäeval.

The co announced that Kevin Johnson, President and Chief Operating Officer will expand his responsibilities and assume the role and responsibilities of President and Chief Executive Officer, effective April 3, 2017.

Also effective April 3, 2017, Howard Schultz, Chairman and Ceo, will be appointed Executive Chairman and will shift his focus to innovation, design and development of Starbucks Reserve Roasteries around the world, expansion of the Starbucks Reserve retail store format and the company's social impact initiatives. In this new role Schultz will continue to serve as chairman of the Board.

As President and Chief Operating Officer since March 2015, Johnson has led the company's global operating businesses across all geographies as well as the core support functions of Starbucks supply chain, marketing, human resources, technology, and mobile and digital platforms.

The co announced that Kevin Johnson, President and Chief Operating Officer will expand his responsibilities and assume the role and responsibilities of President and Chief Executive Officer, effective April 3, 2017.

Also effective April 3, 2017, Howard Schultz, Chairman and Ceo, will be appointed Executive Chairman and will shift his focus to innovation, design and development of Starbucks Reserve Roasteries around the world, expansion of the Starbucks Reserve retail store format and the company's social impact initiatives. In this new role Schultz will continue to serve as chairman of the Board.

As President and Chief Operating Officer since March 2015, Johnson has led the company's global operating businesses across all geographies as well as the core support functions of Starbucks supply chain, marketing, human resources, technology, and mobile and digital platforms.

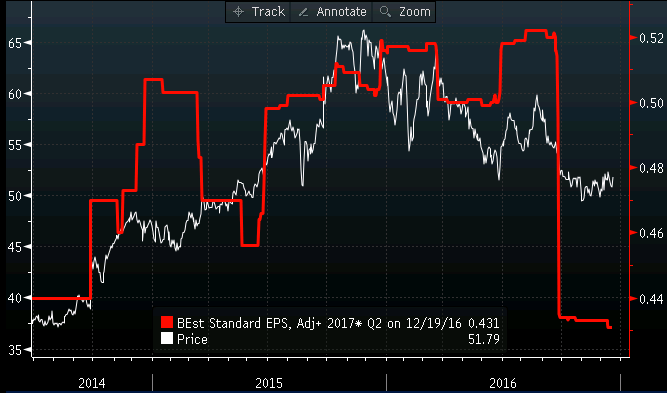

Nike suutis ületada viimaste kuude jooksul langenud Q2 müügitulu ja aktsiakasumi ootust. Esialgne reaktsioon viis aktsia järelkauplemise ajal ligi 6% üles, millest jäi lõpuks järele 2%, kui konverentsikõne ajal avaldatud tulevikutellimused valmistasid pettumuse aga ettevõte loodab siiski kogu 2017.a majandusaasta käivet kasvatada jätkuvalt high-single digit protsendi võrra

2Q rev. $8.18b (YoY 6%) est. $8.09b

2Q gross margin 44.2%, est. 44.3%

2Q Inventory +9.00%

2Q EPS 50c, est. 43c

Nike Worldwide Futures Orders Ex-Currency Up 2%, Est. Up 5.3%

North America futures orders ex-currency down 4%, est. up 1.5%.

Expects 3Q sales to rise by mid-single-digit percentage

Sees 3Q gross margin down 100-125bps

Reiterates sales to rise high-single digits for FY17

Expects North America revenue growth to continue to outpace futures growth; sees return to expanding gross margins with tighter inventory levels in 2H17

2Q rev. $8.18b (YoY 6%) est. $8.09b

2Q gross margin 44.2%, est. 44.3%

2Q Inventory +9.00%

2Q EPS 50c, est. 43c

Nike Worldwide Futures Orders Ex-Currency Up 2%, Est. Up 5.3%

North America futures orders ex-currency down 4%, est. up 1.5%.

Expects 3Q sales to rise by mid-single-digit percentage

Sees 3Q gross margin down 100-125bps

Reiterates sales to rise high-single digits for FY17

Expects North America revenue growth to continue to outpace futures growth; sees return to expanding gross margins with tighter inventory levels in 2H17

Seisuga 31. detsember 2016

USA tarbijate kindlustunne võib presidendivalimiste järgselt kõrge olla, aga jaemüüjate elu pole kõige lihtsam pühade ajal olnud. Lisaks Kohlile, Macy'sele teatas ka L Brands, et detsembri müük jäi oodatust nõrgemaks

L BRANDS DEC. COMP SALES DOWN 1% VS. EST. UP 1.5%

L Brands sees Q4 EPS at low end of $1.85-2.00 prior range vs $1.97 Capital IQ Consensus; December comps -1%

L BRANDS DEC. COMP SALES DOWN 1% VS. EST. UP 1.5%

L Brands sees Q4 EPS at low end of $1.85-2.00 prior range vs $1.97 Capital IQ Consensus; December comps -1%

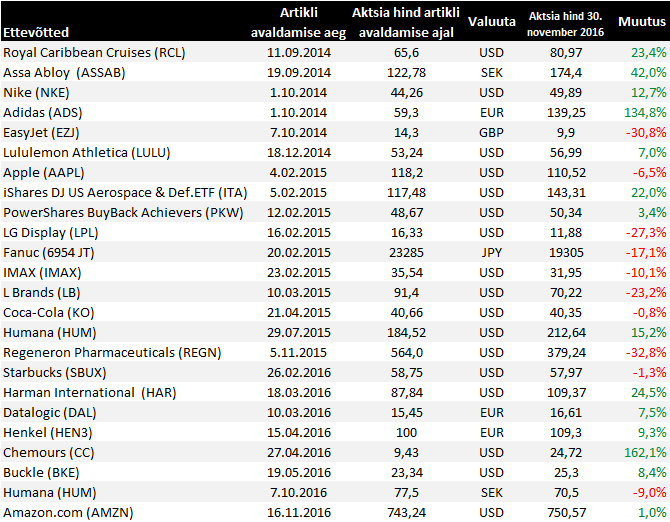

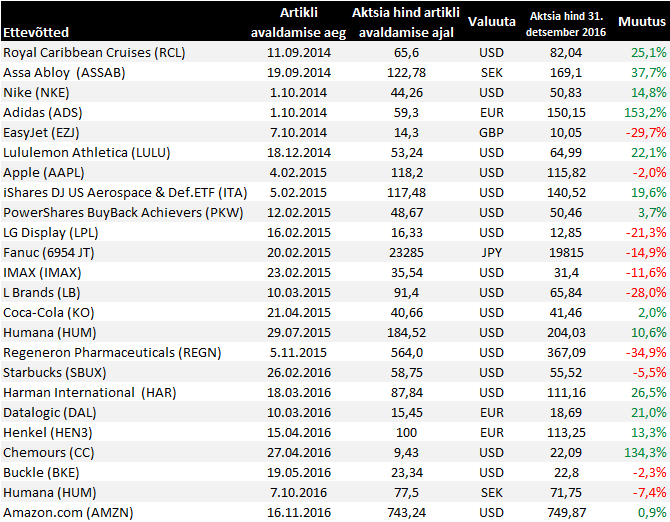

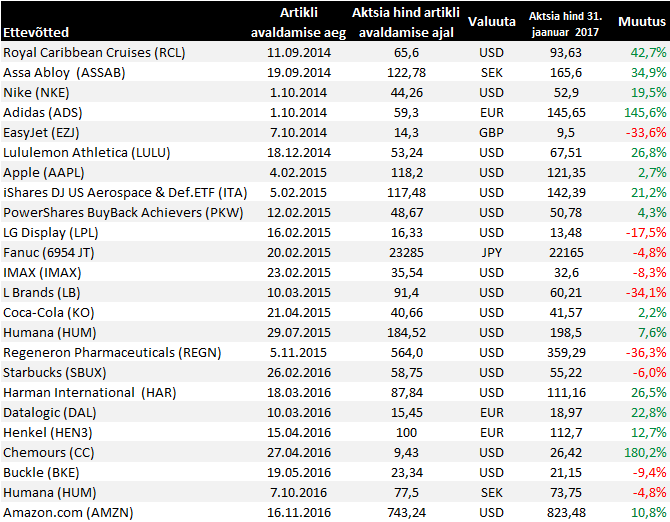

Eeltoodud tabelis on Humana (HUM) kahekordselt.

ttrust

Eeltoodud tabelis on Humana (HUM) kahekordselt.

Võib tõesti tunduda nii aga need on erinevad ettevõtted, üks tegutseb Rootsis, teine Ühendriikides

My Bad.

Lululemon täpsustab veidi oma prognoose

Co issues in-line guidance for Q4 (Jan), sees EPS of $0.99-1.01, excluding non-recurring items, vs. $1.00 Capital IQ Consensus Estimate

previous EPS guidance for the fourth quarter was a range of $0.96 -1.01

Co sees Q4 (Jan) revs of $775-785 mln vs. $782.18 mln Capital IQ Consensus Estimate, compared to previous guidance of net revenue in the range of $765-785 million

Q4 total comparable sales increase in the mid-single digits on a constant dollar basis

Co issues in-line guidance for Q4 (Jan), sees EPS of $0.99-1.01, excluding non-recurring items, vs. $1.00 Capital IQ Consensus Estimate

previous EPS guidance for the fourth quarter was a range of $0.96 -1.01

Co sees Q4 (Jan) revs of $775-785 mln vs. $782.18 mln Capital IQ Consensus Estimate, compared to previous guidance of net revenue in the range of $765-785 million

Q4 total comparable sales increase in the mid-single digits on a constant dollar basis

Eile keelas USA riigikohus Humana ülevõtmise Aetna poolt, kuna see vähendaks ravikindlustuse turul konkurentsi. Aetna kaalub edasikaebamist aga paljud analüüsimajad ei usu, et justiitsministeeriumist võiks tulla soosiv otsus. JPMorgan on varasemalt toonud välja, et Humana aktsia võib tehingu ärajäämisel langeda 190-195 dollarile, mida eile ka korraks testiti.

Royal Caribbean ületab aktsiakasumi ootust, aga jääb müügituluga alla. Tänu rekordkõrgetele broneeringutele ollakse aasta osas optimistlikud

Reports Q4 (Dec) earnings of $1.23 per share, excluding non-recurring items, $0.02 better than the Capital IQ Consensus of $1.21; revenues rose 0.4% year/year to $1.91 bln vs the $1.97 bln Capital IQ Consensus.

Co issues upside guidance for Q1, sees EPS of approx $0.90, excluding non-recurring items, vs. $0.68 Capital IQ Consensus Estimate.

Co issues upside guidance for FY17, sees EPS of $6.90-7.10, excluding non-recurring items, vs. $6.81 Capital IQ Consensus Estimate.

Co says its booked position for 2017 is better than last year's record high, and at higher rates. Strength from North American consumers is driving exceptionally positive trends for North American and European products. These trends, along with a positive outlook for Australia and a solid booked position in China for the first half of the year, are positioning the company for robust growth in 2017.

Reports Q4 (Dec) earnings of $1.23 per share, excluding non-recurring items, $0.02 better than the Capital IQ Consensus of $1.21; revenues rose 0.4% year/year to $1.91 bln vs the $1.97 bln Capital IQ Consensus.

Co issues upside guidance for Q1, sees EPS of approx $0.90, excluding non-recurring items, vs. $0.68 Capital IQ Consensus Estimate.

Co issues upside guidance for FY17, sees EPS of $6.90-7.10, excluding non-recurring items, vs. $6.81 Capital IQ Consensus Estimate.

Co says its booked position for 2017 is better than last year's record high, and at higher rates. Strength from North American consumers is driving exceptionally positive trends for North American and European products. These trends, along with a positive outlook for Australia and a solid booked position in China for the first half of the year, are positioning the company for robust growth in 2017.

Starbucks raporteeris eile prognoositust veidi nõrgema müügitulu juures ootuspärase aktsiakasumi. Makrokeskkonda hinnatakse keeruliseks ja osaliselt mõjutas tulemusi ka mobiilsete tellimuste populaarsus, mis tekitas kohvikutes ummikuid ja tingis lõpetamata makseid. Terve aasta aktsiakasumi ootus jäeti samaks, müügitulu prognoosi korrigeeriti tagasihoidlikuma aasta alguse tõttu pisut allapoole.

Reports Q1 (Dec) earnings of $0.52 per share, excluding non-recurring items, in-line with the Capital IQ Consensus of $0.52; revenues rose 6.7% year/year to $5.73 bln vs the $5.85 bln Capital IQ Consensus.

Co issues guidance for FY17, reaffirms EPS of $2.12-2.14, excluding non-recurring items, vs. $2.14 Capital IQ Consensus Estimate; lowers FY17 revenue guidance from double digit growth to +8-10% growth, this computes to $23.02-23.45 bln vs. $23.11 bln Capital IQ Consensus Estimate.

Starbucks on conf call sees Q2 $0.44-0.45 vs $0.46 Capital IQ Consensus Estimate

* Starbucks on earnings call says stores challenged to keep up with higher demand

Seeing “significant congestion” at hand-off point in U.S.

* Congestion resulted in customers not completing sale

* Working on digital enhancements to handle more orders

* Says macro retail environment is “challenging”

Reports Q1 (Dec) earnings of $0.52 per share, excluding non-recurring items, in-line with the Capital IQ Consensus of $0.52; revenues rose 6.7% year/year to $5.73 bln vs the $5.85 bln Capital IQ Consensus.

Co issues guidance for FY17, reaffirms EPS of $2.12-2.14, excluding non-recurring items, vs. $2.14 Capital IQ Consensus Estimate; lowers FY17 revenue guidance from double digit growth to +8-10% growth, this computes to $23.02-23.45 bln vs. $23.11 bln Capital IQ Consensus Estimate.

Starbucks on conf call sees Q2 $0.44-0.45 vs $0.46 Capital IQ Consensus Estimate

* Starbucks on earnings call says stores challenged to keep up with higher demand

Seeing “significant congestion” at hand-off point in U.S.

* Congestion resulted in customers not completing sale

* Working on digital enhancements to handle more orders

* Says macro retail environment is “challenging”

Apple lõi kvartali lukku arvatust paremate tulemustega ja kuigi ettevaatav müügitulu ootus valmistas väikese pettumuse, siis järelkauplemise ajal jäi turul domineerima positiivne emotsioon.

Apple reports Q1 (Dec) earnings of $3.36 per share, $0.14 better than the Capital IQ Consensus of $3.22; revenues rose 3.3% year/year to $78.35 bln vs the $77.26 bln Capital IQ Consensus. Gross margin 38.5%, in-line with estimates vs. 40.5% last year.

Co reported Q1 iPhones of 78.3 mln vs 77.3 mln ests versus 74.8 mln last year.

Co reported Q1 iPads of 13.1 mln vs 14.7 mln ests versus 16.1 mln last year.

Co reported Q1 Macs of 5.4 mln vs 5.2 mln ests versus 5.3 mln last year.

Apple sees Q2 revs $51.5-53.5 bln vs $54.0 bln Capital IQ Consensus Estimate

Apple sees Q2 gross margins of 38-39% vs 38.7% ests and 39.4% last year

The company expects that foreign exchange will be a 'major negative' as the company moves from the December to the March quarter.

Apple reports Q1 (Dec) earnings of $3.36 per share, $0.14 better than the Capital IQ Consensus of $3.22; revenues rose 3.3% year/year to $78.35 bln vs the $77.26 bln Capital IQ Consensus. Gross margin 38.5%, in-line with estimates vs. 40.5% last year.

Co reported Q1 iPhones of 78.3 mln vs 77.3 mln ests versus 74.8 mln last year.

Co reported Q1 iPads of 13.1 mln vs 14.7 mln ests versus 16.1 mln last year.

Co reported Q1 Macs of 5.4 mln vs 5.2 mln ests versus 5.3 mln last year.

Apple sees Q2 revs $51.5-53.5 bln vs $54.0 bln Capital IQ Consensus Estimate

Apple sees Q2 gross margins of 38-39% vs 38.7% ests and 39.4% last year

The company expects that foreign exchange will be a 'major negative' as the company moves from the December to the March quarter.

Jaanuari lõpu seisuga

Tugev baas aeglustas Assa Abloy 2016.a neljanda kvartali orgaanilise kasvu 1,0%ni (Q3 2,0%), mida oli siiski vähem võrreldes analüütikute ootusega ning peamiseks teguriks selle taga on jätkuvalt nõrgapoolne nõudlus arenevates riikides, eeskätt Hiinas.

• Assa Abloy 4Q adj. operating profit SEK2.91b, est. SEK3.20b (range SEK3.15b-SEK3.30b).

• 4Q sales SEK19.5b, est. SEK19.7b (range SEK18.8b-SEK20.1b)

• 4Q organic rev. growth +1.00%

• FY16 dividend SEK3.00, median est. SEK2.825

CEO: “My judgment is that the global economic trend remains weak. On most markets in North and South America and in parts of Europe there is a positive trend, but on many markets in Asia and the Middle East the trend is weak. However, our strategy of expanding our market presence, even on the emerging markets, remains unchanged. We are also continuing our investments in new products, especially in the growth area of electromechanics.”

• Assa Abloy 4Q adj. operating profit SEK2.91b, est. SEK3.20b (range SEK3.15b-SEK3.30b).

• 4Q sales SEK19.5b, est. SEK19.7b (range SEK18.8b-SEK20.1b)

• 4Q organic rev. growth +1.00%

• FY16 dividend SEK3.00, median est. SEK2.825

CEO: “My judgment is that the global economic trend remains weak. On most markets in North and South America and in parts of Europe there is a positive trend, but on many markets in Asia and the Middle East the trend is weak. However, our strategy of expanding our market presence, even on the emerging markets, remains unchanged. We are also continuing our investments in new products, especially in the growth area of electromechanics.”