tänud, nüüd on korras

Septembris prognoosi tõstnud easyJet jäi maksueelse kasumiga üsna konsensuse lähedale ning ütleb, et järgneva aasta osas ühtib ootus nõukogu omaga. Hetkel prognoosib konsensus FY2016.a maksueelseks kasumiks 737,4 miljonit naela.

* EasyJet FY pretax GBP686m, est. GBP689m.

* Rev. GBP4.69b, est. GBP4.72b

* Div. 55.2p; BDVD forecast 56p, yr ago 45.4p

* Outlook: Says market expectations are in line within the Board’s expectations for the full year

* In FY16 plan to increase capacity by c.7% and by c.8% in the first half; fuel bill to decline by GBP140m-GBP160m; expect a slight decline in revenue per seat at constant currency during the first half of the year; expect a slight decline in total cost per seat at constant currency including fuel for the full year of approximately 1%

* EasyJet FY pretax GBP686m, est. GBP689m.

* Rev. GBP4.69b, est. GBP4.72b

* Div. 55.2p; BDVD forecast 56p, yr ago 45.4p

* Outlook: Says market expectations are in line within the Board’s expectations for the full year

* In FY16 plan to increase capacity by c.7% and by c.8% in the first half; fuel bill to decline by GBP140m-GBP160m; expect a slight decline in revenue per seat at constant currency during the first half of the year; expect a slight decline in total cost per seat at constant currency including fuel for the full year of approximately 1%

L Brands suutis eile lüüa hiljuti kergitatud EPSi ootust ning raporteerida ootuspärane Q3 müügitulu. Q4 aktsiakasumi ootus jääb konsensuse omast lahjamaks aga kogu aasta prognoosi tõsteti, kuid märkida tasub seda, et firmale meeldib ootuste seadmisel olla konservatiivne

L Brands reports Q3 (Oct) earnings of $0.55 per share, $0.03 better than the Capital IQ Consensus of $0.52; revenues rose 7.0% year/year to $2.48 bln vs the $2.5 bln Capital IQ Consensus.

Co issues downside guidance for Q4, sees EPS of $1.85-1.95 vs. $1.98 Capital IQ Consensus Estimate.

Co raises FY16 EPS to $3.69-3.79 from $3.58-3.73 vs. $3.79 Capital IQ Consensus Estimate.

L Brands reports Q3 (Oct) earnings of $0.55 per share, $0.03 better than the Capital IQ Consensus of $0.52; revenues rose 7.0% year/year to $2.48 bln vs the $2.5 bln Capital IQ Consensus.

Co issues downside guidance for Q4, sees EPS of $1.85-1.95 vs. $1.98 Capital IQ Consensus Estimate.

Co raises FY16 EPS to $3.69-3.79 from $3.58-3.73 vs. $3.79 Capital IQ Consensus Estimate.

Nike muudab aktsia väikeinvestoritele aktraktiivsemaks, korraldades spliti. Ühtlasi jätkatakse kapitali tagastamist läbi aktsiate tagasiostude ning kõrgema dividendi, mis väärtpaberi tugeva hinnatõusu taustal tähendab üsna tagasihoidlikku 1% tootlust.

* Co approved a new four-year, $12 bln program to repurchase shares of NIKE's Class B Common Stock. The Company anticipates that the current $8 bln share repurchase program will be completed before the end of fiscal 2016, and the new program will commence upon the completion of the current program.

* Board of Directors also declared a quarterly cash dividend on the Company's outstanding Class A and Class B Common Stock of $0.32 per share, on a pre-split basis, payable on January 4, 2016 to shareholders of record at the close of business on December 9, 2015. The dividend represents a 14 percent increase over the previous pre-split quarterly rate of $0.28 per share. This is the fourteenth year in a row the Company has increased its annual dividend, over which time the dividend has increased by a factor of more than 10.

* Also approved a two-for-one split of both NIKE's Class A and Class B Common shares. The split will be in the form of a 100% stock dividend payable on Dec 23, 2015 to shareholders of record at the close Dec 9, 2015.

* Co approved a new four-year, $12 bln program to repurchase shares of NIKE's Class B Common Stock. The Company anticipates that the current $8 bln share repurchase program will be completed before the end of fiscal 2016, and the new program will commence upon the completion of the current program.

* Board of Directors also declared a quarterly cash dividend on the Company's outstanding Class A and Class B Common Stock of $0.32 per share, on a pre-split basis, payable on January 4, 2016 to shareholders of record at the close of business on December 9, 2015. The dividend represents a 14 percent increase over the previous pre-split quarterly rate of $0.28 per share. This is the fourteenth year in a row the Company has increased its annual dividend, over which time the dividend has increased by a factor of more than 10.

* Also approved a two-for-one split of both NIKE's Class A and Class B Common shares. The split will be in the form of a 100% stock dividend payable on Dec 23, 2015 to shareholders of record at the close Dec 9, 2015.

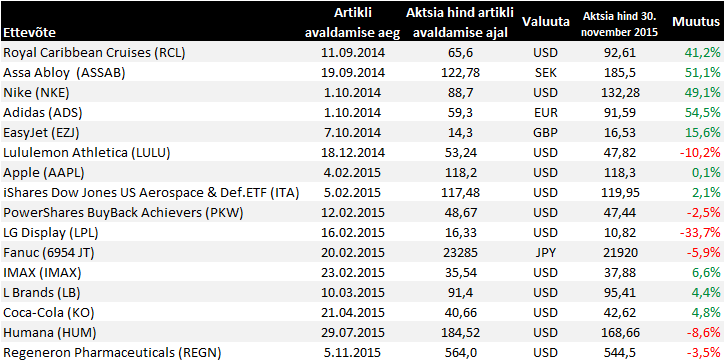

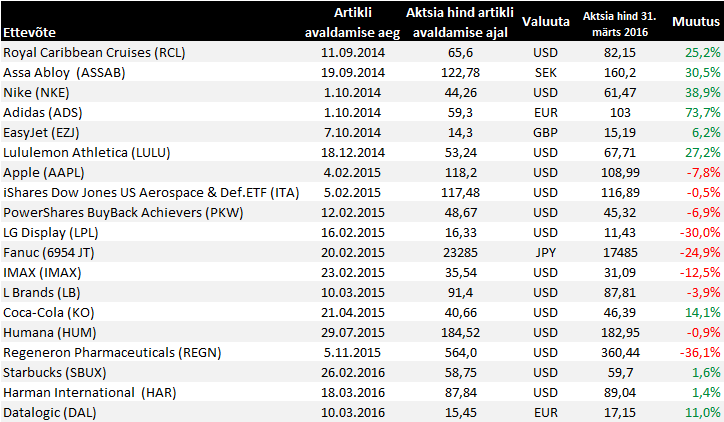

Nimekiri 30.nov seisuga

L Brandsi müügikasv püsis novembris tugevana

L Brands reports November same store sales +7.0% vs +3.0% Retail Metrics consensus

L Brands reports November same store sales +7.0% vs +3.0% Retail Metrics consensus

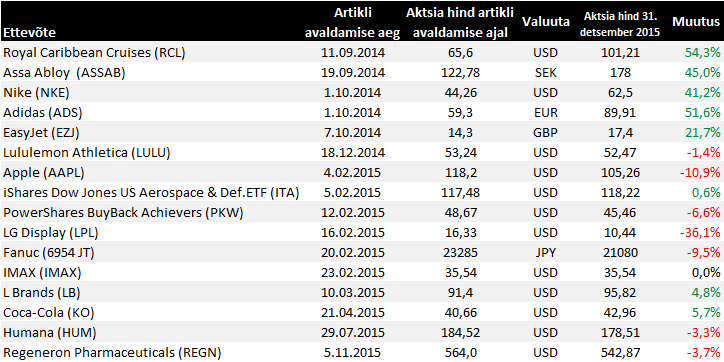

Seisuga 31.dets

Osad majad kartsid, et Lululemon saavutas pühade ajal suurema liikluse oma poodides tänu kõrgematele allahindlustele, kuid eilne positiivne kasumihoiatus näitas, et marginaalides ei antud järele:

lululemon athletica raises Q4 guidance to EPS $0.78-0.80, up from $0.75-0.78 vs $0.77 consensus, revenue $690-695 mln, prior guidance $670-685 mln vs $678.2 mln Capital IQ consensus

This is based on a total comparable sales increase in the high-single digits on a constant dollar basis, prior guidance based on total comparable sales increase in the mid-single digits on a constant dollar basis.

lululemon athletica raises Q4 guidance to EPS $0.78-0.80, up from $0.75-0.78 vs $0.77 consensus, revenue $690-695 mln, prior guidance $670-685 mln vs $678.2 mln Capital IQ consensus

This is based on a total comparable sales increase in the high-single digits on a constant dollar basis, prior guidance based on total comparable sales increase in the mid-single digits on a constant dollar basis.

Euroopa Keskpangas jätkub deposiitide kasv vaatamata negatiivsele intressimäärale (joonisel triljonit eurot)

EasyJeti esimese kvartali müügitulu jäi Pariisi ja Egiptuse sündmuste tõttu oodatust pehmemeks, kuid firma sõnul on broneeringud hakanud uuesti taastuma ning tänu odavamale kütusele ja kulude kontrollile suudetakse praeguste prognooside kohaselt teenida septembris lõppeval majandusaastal turu ootusele vastava maksueelse kasumi (konsensus GBP738m vs GBP686m 2015.a)

* EasyJet 1Q rev. GBP930m, est. GBP959m (range GBP937m-GBP984m). Yr ago GBP931m.

* 1Q revenue per seat was down by 3.7% at constant currency; cost per seat decreased by 3.7% at constant currency, .

* Sees profit before tax for the year to 30 September in line with market expectations

* Forward bookings for the second quarter are showing a marked improvement in revenue per seat compared to November and December

* EasyJet 1Q rev. GBP930m, est. GBP959m (range GBP937m-GBP984m). Yr ago GBP931m.

* 1Q revenue per seat was down by 3.7% at constant currency; cost per seat decreased by 3.7% at constant currency, .

* Sees profit before tax for the year to 30 September in line with market expectations

* Forward bookings for the second quarter are showing a marked improvement in revenue per seat compared to November and December

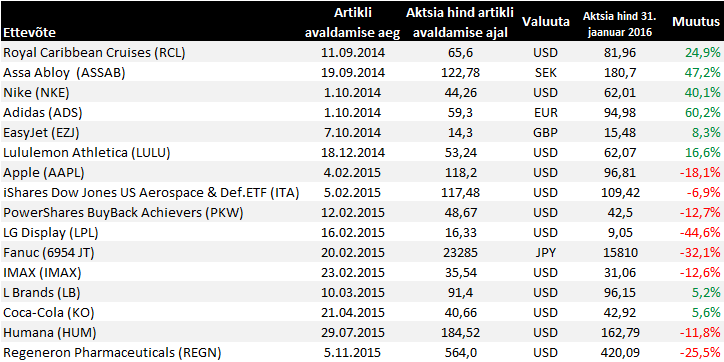

Seisuga 31. jaanuar 2016

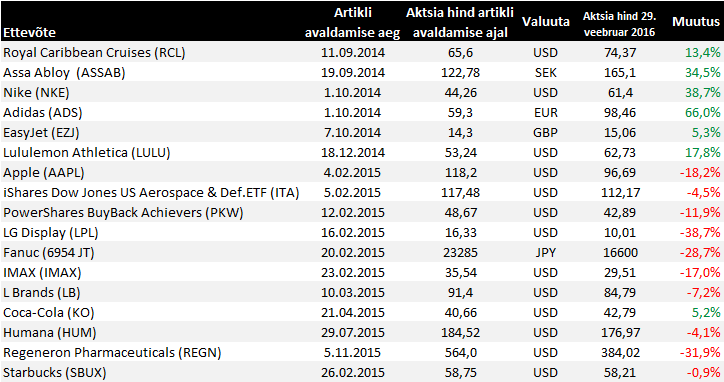

olen võlgu tabeli 29. veebruari seisuga

Lisame nimekirja veel kaks ettevõtet, mille tegemistel hoiame silma peal ning üritame regulaarselt infot ka siia postitada:

Harman – maailma juhtiv infotainment-süsteemide tootja

Meist kõigist saavad poemüüjad

Harman – maailma juhtiv infotainment-süsteemide tootja

Meist kõigist saavad poemüüjad

Nike raporteeris eile oodatust parema kolmanda kvartali aktsiakasumi ja ligi 8% YoY kasvanud käibe, mis jäi konsensusele pisut alla. 2017.a aktsiakasumi kasvuks prognoosib Nike "low teens" ning suuresti just teise poolaata arvelt, kuna esimeses pooles tuleb teha suurte spordisündmuste toetuseks investeeringuid. Kuna Nike 5a plaan näeb ette kesmiselt 15% EPS kasvu aastas ning turu ootused on koos aktsiaga üles läinud, jäi aktsia reaktsioon eile järelturul negatiivseks (-6%).

Nike reports Q3 (Feb) earnings of $0.55 per share, $0.07 better than the Capital IQ Consensus of $0.48; revenues rose 7.7% year/year to $8.03 bln vs the $8.2 bln Capital IQ Consensus

Gross margin was 45.9% vs. 45.4% guidance, flat compared to prior year.

NIKE Futures Orders +12%; +17% in constant currency vs. estimates in the mid to high teens ex-FX

FY17 reported revenue to grow at high single digit rate

FY17 EPS to grow at low teen rate with EPS growth more heavily weighted toward the back half of FY17.

Nike reports Q3 (Feb) earnings of $0.55 per share, $0.07 better than the Capital IQ Consensus of $0.48; revenues rose 7.7% year/year to $8.03 bln vs the $8.2 bln Capital IQ Consensus

Gross margin was 45.9% vs. 45.4% guidance, flat compared to prior year.

NIKE Futures Orders +12%; +17% in constant currency vs. estimates in the mid to high teens ex-FX

FY17 reported revenue to grow at high single digit rate

FY17 EPS to grow at low teen rate with EPS growth more heavily weighted toward the back half of FY17.

Lululemon suutis veebruaris tõstetud Q4 prognoose lüüa, müügitulu ootused esimeseks kvartaliks ja terveks majandusaastaks vastavad konsensuse ootusetele, aktsiakasumi prognoos jääb aga nõrgemaks (investorite üheks fookuseks on olnud marginaalide taastamise võime).

Lululemon reports Q4 (Jan) earnings of $0.85 per share, $0.05 better than the Capital IQ Consensus of $0.80; revenues rose 16.9% year/year to $704.3 mln vs the $693.83 mln Capital IQ Consensus. LULU reports Q4 total comps of +11% vs +high single digits prior guidance and +8% estimate.

Co issues guidance for Q1, sees EPS of $0.28-0.30 vs. $0.37 Capital IQ Consensus Estimate; sees Q1 revs of $483-488 mln vs. $484.73 mln Capital IQ Consensus Estimate. LULU sees Q1 total comparable store sales mid single digits on a constant dollar basis vs +7% estimate

Co issues guidance for FY17, sees EPS of $2.05-2.15 vs. $2.16 Capital IQ Consensus Estimate; sees FY17 revs of $2.285-2.335 bln vs. $2.33 bln Capital IQ Consensus Estimate. LULU sees fiscal 2016 (FY17) total comparable store sales increase in the mid-single digits on a constant dollar basis vs +6% estimate.

Lululemon reports Q4 (Jan) earnings of $0.85 per share, $0.05 better than the Capital IQ Consensus of $0.80; revenues rose 16.9% year/year to $704.3 mln vs the $693.83 mln Capital IQ Consensus. LULU reports Q4 total comps of +11% vs +high single digits prior guidance and +8% estimate.

Co issues guidance for Q1, sees EPS of $0.28-0.30 vs. $0.37 Capital IQ Consensus Estimate; sees Q1 revs of $483-488 mln vs. $484.73 mln Capital IQ Consensus Estimate. LULU sees Q1 total comparable store sales mid single digits on a constant dollar basis vs +7% estimate

Co issues guidance for FY17, sees EPS of $2.05-2.15 vs. $2.16 Capital IQ Consensus Estimate; sees FY17 revs of $2.285-2.335 bln vs. $2.33 bln Capital IQ Consensus Estimate. LULU sees fiscal 2016 (FY17) total comparable store sales increase in the mid-single digits on a constant dollar basis vs +6% estimate.

31. märtsi seisuga

lisame jälgimisnimekirja Henkeli, millest Kristiina on kirjutanud siin: Henkel – maailma suurim tööstusliimide tootja

Coca-Cola numbrid praktiliselt in-line

Coca-Cola prelim Q1 $0.45 vs $0.44 Capital IQ Consensus Estimate; revs $10.28 bln (YoY -4%) vs $10.24 bln Capital IQ Consensus Estimate

2016 OUTLOOK

Expect organic revenue to be up 4% to 5% in 2016, in line with long-term target.

Expects comparable currency neutral income before taxes (structurally adjusted) to grow 6% to 8% in 2016, in line with long-term target, as strong operating profit growth is expected to be partially offset by increased interest expense.

Based on the current spot rates, currency is expected to be an 8 to 9 point headwind, including the impact of hedged positions for the full year.

Coca-Cola prelim Q1 $0.45 vs $0.44 Capital IQ Consensus Estimate; revs $10.28 bln (YoY -4%) vs $10.24 bln Capital IQ Consensus Estimate

2016 OUTLOOK

Expect organic revenue to be up 4% to 5% in 2016, in line with long-term target.

Expects comparable currency neutral income before taxes (structurally adjusted) to grow 6% to 8% in 2016, in line with long-term target, as strong operating profit growth is expected to be partially offset by increased interest expense.

Based on the current spot rates, currency is expected to be an 8 to 9 point headwind, including the impact of hedged positions for the full year.

IMAXilt oodatust paremad tulemused tänu tugevale piletitulule (Star Wars eeldatavalt andis olulise panuse):

--Reports Q1 (Mar) earnings of $0.22 per share, $0.06 better than the Capital IQ Consensus of $0.16; revenues rose 48.1% year/year to $92.1 mln, vs the $83.91 mln Capital IQ Consensus, primarily due to strong box office.

--Global Box Office of $272 million, up 64% from Q1 2015, driven by strong growth domestically and continued strength in international markets

--Adjusted EBITDA grew 97% year-over-year to $31.5 million, resulting in adjusted EBITDA margins of 37.4%, up over 1,000 basis points from Q1 2015

--Signings growth of 71%, with 36 new signings up from 21 in Q1 2015

--Reports Q1 (Mar) earnings of $0.22 per share, $0.06 better than the Capital IQ Consensus of $0.16; revenues rose 48.1% year/year to $92.1 mln, vs the $83.91 mln Capital IQ Consensus, primarily due to strong box office.

--Global Box Office of $272 million, up 64% from Q1 2015, driven by strong growth domestically and continued strength in international markets

--Adjusted EBITDA grew 97% year-over-year to $31.5 million, resulting in adjusted EBITDA margins of 37.4%, up over 1,000 basis points from Q1 2015

--Signings growth of 71%, with 36 new signings up from 21 in Q1 2015