TTWO sai eile pihta pärast nädalavahetusel ilmunud Forbesi artiklit, milles toodi välja, et Red Dead Redemptioni Online beta versioonis on väga keeruline koguda jõukust ning täheldada tegelaskuju arengus sarnast progressi nagu GTA online'i puhul ning see võib tappa mängija motivatsiooni. Firma jaoks on aga kriitiline hoida läbi huvitava sisu, virtuaalostude ning täiendavate pakketidega mängijat võimalikult kaua kinni, et pikendada mängu eluiga. Kuna tegu on alles beta versiooniga, siis jääb üles lootus, et ettevõte suudab etteheiteid lõppversioonis adresseerida.

'Red Dead Online' Has Two Significant Problems To Overcome

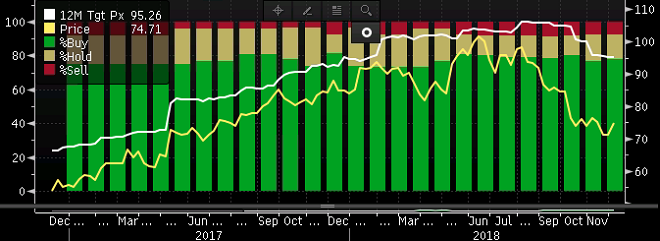

Jefferies alustab laiemas sektorianalüüsis Aptivi katmist

*Jefferies initiated coverage of Aptiv Plc with a recommendation of buy.

* PT set to $100, implies 34% increase from last close. Aptiv average PT is $95.26

Analüüsimajad on viimastel kuudel toonud ootusi alla ning koos sellega on liikunud madalamale ka keskmine 12kuu hinnasiht

*Jefferies initiated coverage of Aptiv Plc with a recommendation of buy.

* PT set to $100, implies 34% increase from last close. Aptiv average PT is $95.26

Analüüsimajad on viimastel kuudel toonud ootusi alla ning koos sellega on liikunud madalamale ka keskmine 12kuu hinnasiht

Rahatrükk Rockstari stiilis :)

'Red Dead Online' Is Giving Away Free Cash And Gold Bars As It Fixes Its Economy

'Red Dead Online' Is Giving Away Free Cash And Gold Bars As It Fixes Its Economy

Eilsel investorite päeval kinnitas Starbucks oma 2019.a prognoose, ent kärpis pikaajalist aktsiakasumi aastast kasvuootust varasema 12%+ pealt vähemalt 10%le, viidates suuremale konkurentsile ja kõrgematele kuludele.

*Starbucks reaffirms FY19 EPS guidance of $2.61-2.66, excluding non-recurring items, vs. $2.65 S&P Capital IQ Consensus; sees FY19 revs +5-7% (implies $26-26.45 bln) vs. $26.1 bln S&P Capital IQ Consensus.

* Co said it sees consolidated revenue growth of 7% to 9% and non- GAAP earnings per share growth of at least 10% in the longer term.

* Co. sees expanding retail store portfolio by about 6% to 7% net new units and growing same store sales by 3% to 4%, globally, each year. Starbucks CEO Kevin Johnson said customer behaviors are "shifting rapidly" and the company must continue to adapt at the same pace, speaking at the Investor Day in New York City.

* Starbucks says it has increased leverage to support growth, more competition is entering coffeeshop category

* Management focused on accelerating China, U.S., which are "significant" growth opportunities

*Starbucks is ramping up growth in China and looking for "prime real estate" as it will continue to "aggressively grow," Head of International John Culver said at the Investor Day in New York

* China revenue growth 80% driven by new stores, 20% by comp. sales

*Plenty" of room to expand in the U.S.

* Digital to help comp. sales in U.S.

*Delivery expansion in partnership with UberEats coming to 25% of U.S. company stores by end of 2Q

*To remodels 1/3 of U.S. stores next 2 years, new decor and more capacity

* Nestle deal seen adding in FY20

** New Nestle products to be sold starting next year

* Will have branded capsules for Nespresso coffee systems

*Starbucks reaffirms FY19 EPS guidance of $2.61-2.66, excluding non-recurring items, vs. $2.65 S&P Capital IQ Consensus; sees FY19 revs +5-7% (implies $26-26.45 bln) vs. $26.1 bln S&P Capital IQ Consensus.

* Co said it sees consolidated revenue growth of 7% to 9% and non- GAAP earnings per share growth of at least 10% in the longer term.

* Co. sees expanding retail store portfolio by about 6% to 7% net new units and growing same store sales by 3% to 4%, globally, each year. Starbucks CEO Kevin Johnson said customer behaviors are "shifting rapidly" and the company must continue to adapt at the same pace, speaking at the Investor Day in New York City.

* Starbucks says it has increased leverage to support growth, more competition is entering coffeeshop category

* Management focused on accelerating China, U.S., which are "significant" growth opportunities

*Starbucks is ramping up growth in China and looking for "prime real estate" as it will continue to "aggressively grow," Head of International John Culver said at the Investor Day in New York

* China revenue growth 80% driven by new stores, 20% by comp. sales

*Plenty" of room to expand in the U.S.

* Digital to help comp. sales in U.S.

*Delivery expansion in partnership with UberEats coming to 25% of U.S. company stores by end of 2Q

*To remodels 1/3 of U.S. stores next 2 years, new decor and more capacity

* Nestle deal seen adding in FY20

** New Nestle products to be sold starting next year

* Will have branded capsules for Nespresso coffee systems

H&Mi neljanda kvartali müük osutus ootuspäraseks, marginaalidest kuuleme aga alles jaanuari viimasel päeval, mil avaldatakse kogu majandusaasta aruanne.

4Q sales SEK56.4 billion (YoY +12%), estimate SEK56.11 billion (Bloomberg data)

4Q sales SEK56.4 billion (YoY +12%), estimate SEK56.11 billion (Bloomberg data)

Nike pakub turul ettevõtete kasvu osas muretsema hakanud investoritele sõõma värsket õhku, saavutades teises kvartalis kiirenenud müügitulu kasvu ning kergitades valuutakõikumisi arvestamata fiskaalaasta müügitulu ootust

Nike reports Q2 (Nov) earnings of $0.52 per share, $0.06 better than the S&P Capital IQ Consensus of $0.46; an increase of 13% percent driven by double-digit revenue growth, gross margin expansion and a lower average share count, partially offset by higher selling and administrative expenses and a higher effective tax rate.

Revenues rose 9.6% year/year to $9.37 bln vs the $9.17 bln S&P Capital IQ Consensus. Revenues for the NIKE Brand were $8.9 billion, up 14% on a currency-neutral basis driven by accelerated growth across all geographies and in NIKE Direct, led by digital. Revenue grew in nearly every key category led by Sportswear with well-balanced double-digit growth across footwear and apparel globally.

Now sees currency neutral FY19 revenue up in the high single-digit range, potentially approaching low double digits (consensus +7.5%), with gross margin expansion roughly in-line with expansion of 70 bps delivered over the first half of FY19.

Sees currency neutral Q3 revenue growth squarely within the high single-digit range vs. +7% consensus; sees Q3 gross margin expansion roughly in-line with full year guidance vs. +100 bps consensus.

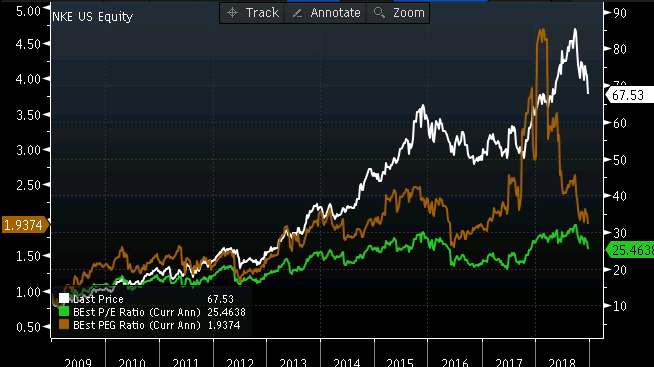

Nike'i aktsia (valge), jooksva majandusaasta oodataval kasumil põhinev PE (roheline) ning PEG (pruun)

Nike reports Q2 (Nov) earnings of $0.52 per share, $0.06 better than the S&P Capital IQ Consensus of $0.46; an increase of 13% percent driven by double-digit revenue growth, gross margin expansion and a lower average share count, partially offset by higher selling and administrative expenses and a higher effective tax rate.

Revenues rose 9.6% year/year to $9.37 bln vs the $9.17 bln S&P Capital IQ Consensus. Revenues for the NIKE Brand were $8.9 billion, up 14% on a currency-neutral basis driven by accelerated growth across all geographies and in NIKE Direct, led by digital. Revenue grew in nearly every key category led by Sportswear with well-balanced double-digit growth across footwear and apparel globally.

Now sees currency neutral FY19 revenue up in the high single-digit range, potentially approaching low double digits (consensus +7.5%), with gross margin expansion roughly in-line with expansion of 70 bps delivered over the first half of FY19.

Sees currency neutral Q3 revenue growth squarely within the high single-digit range vs. +7% consensus; sees Q3 gross margin expansion roughly in-line with full year guidance vs. +100 bps consensus.

Nike'i aktsia (valge), jooksva majandusaasta oodataval kasumil põhinev PE (roheline) ning PEG (pruun)

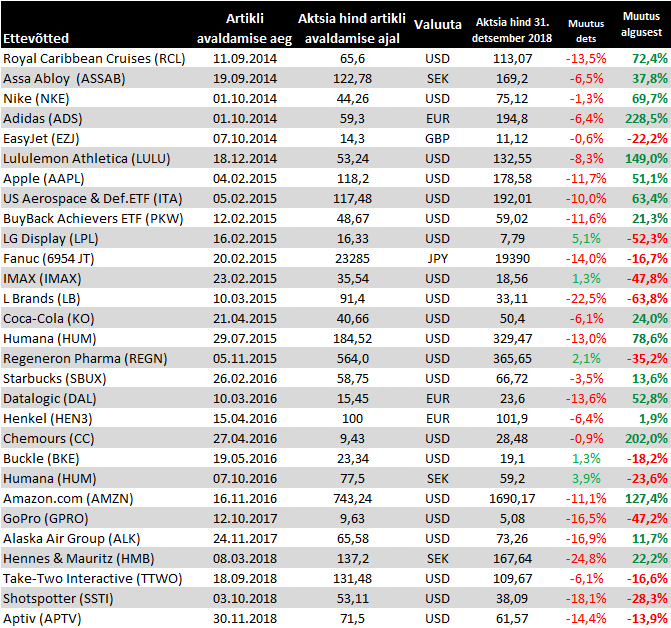

Muutused detsembri lõpu seisuga

Kui jaemüüjatel üldiselt pole Ühendriikides pühade ajal kuigi hästi läinud, siis Lululemon vastupidiselt tõstab prognoose

Co issues raised guidance for Q4 (Jan), sees EPS of $1.72-1.74 from $1.64-1.67 vs. $1.70 S&P Capital IQ Consensus; sees Q4 (Jan) revs of $1.14-1.15 bln from $1.115-1.125 bln vs. $1.12 bln S&P Capital IQ Consensus; total comparable sales increased in the mid-to-high teens on a constant dollar basis (prior guidance in the high-single to low-double digits on a constant dollar basis).

Co issues raised guidance for Q4 (Jan), sees EPS of $1.72-1.74 from $1.64-1.67 vs. $1.70 S&P Capital IQ Consensus; sees Q4 (Jan) revs of $1.14-1.15 bln from $1.115-1.125 bln vs. $1.12 bln S&P Capital IQ Consensus; total comparable sales increased in the mid-to-high teens on a constant dollar basis (prior guidance in the high-single to low-double digits on a constant dollar basis).

Henkel hindab praegust turuolukorda keeruliseks, ent usub saavutavat tänavu müügitulu 2-4% orgaanilist kasvu. Ühtlasi teatati, et kavatsetakse suurendada investeeringuid, mis mõjutab negatiivselt ärikasumi marginaali (2018.a esialgsetel tulemustel oli 17,6% kuid jääb 16-17% vahemikku 2019.a) ning jätab korrigeeritud aktsiakasumi tänavu mullusest väiksemaks, samas kui analüütikud ootasid ca 5% kasvu.

Henkel sees 2019 adj. Ebit margin of 16%-17%, adj. earnings per preferred share development in mid- single digit percentage range below prior year on constant exchange rates, co. says in statement.

* Henkel to invest ~EU300m annually from 2019 onwards; about two thirds for brands, technologies and innovations and one third for digital transformation

* Sees mid- to long-term organic sales growth of 2%-4% , adj. EPS growth mid- to high-single-digit percentage range at constant FX

Henkel sees 2019 adj. Ebit margin of 16%-17%, adj. earnings per preferred share development in mid- single digit percentage range below prior year on constant exchange rates, co. says in statement.

* Henkel to invest ~EU300m annually from 2019 onwards; about two thirds for brands, technologies and innovations and one third for digital transformation

* Sees mid- to long-term organic sales growth of 2%-4% , adj. EPS growth mid- to high-single-digit percentage range at constant FX

Ehkki easyjeti 2019. fiskaalaasta esimese kvartali müügitulu kasvas ligi 14%, siis käive istme kohta oli aastatagusest madalam mitmete ühekordsete asjaolude tõttu (uued raamatupidamisstandardid, droonilennud Gatwickil ning aasta varem ajutiselt kasuks tulnud konkurentide pankrotid ja Ryanari lendude tühistamised). Brexitist hoolimata püsib aga nõudlus tugevana ning ettevõte ootab septembris lõppeval majandusaastal turuga sarnast maksueelset kasumit (578 miljonit naela ehk sama palju nagu 2018. fiskaalaastal).

Total revenue in the first quarter to 31 December 2018 increased by 13.7% to £1,296 million. Passenger revenue increased by 12.2% to £1,025 million and ancillary revenue increased by 19.9% to £271 million.

Total revenue per seat decreased by 4.2% at constant currency, in line with expectations

"For the first half of 2019, booking levels currently remain encouraging despite the lack of certainty around Brexit for our customers. Second half bookings continue to be ahead of last year and our expectations for the full year headline profit before tax are broadly in line with current market expectations."

Total revenue in the first quarter to 31 December 2018 increased by 13.7% to £1,296 million. Passenger revenue increased by 12.2% to £1,025 million and ancillary revenue increased by 19.9% to £271 million.

Total revenue per seat decreased by 4.2% at constant currency, in line with expectations

"For the first half of 2019, booking levels currently remain encouraging despite the lack of certainty around Brexit for our customers. Second half bookings continue to be ahead of last year and our expectations for the full year headline profit before tax are broadly in line with current market expectations."

Eelnevat hoiatust arvestes avaldas Apple ootuspärased esimese kvartali tulemused ja kuigi teise kvartali müügitulu ning brutokasumi margaali keskpunkt jäävad konsensuse prognoosidest madalamaks, andsid Tim Cooki kommentaarid jaanuaris paranenud iPhone'i müügitrendist lootust, et ehk on olukord stabiliseerumas ning see võimaldab saavutada numbreid pigem ootuse vahemiku ülemises otsas.

Apple prelim Q1 $4.18 vs $4.17 S&P Capital IQ Consensus Estimate; revs $84.3 bln vs $84.00 bln S&P Capital IQ Consensus Estimate

Apple reports Q1 gross margin of 38.0% versus ests of 38.0% (in line with pre-announcement); sees Q2 gross margins 37-38% versus 38.1% ests and 38.3% last year

Co issues guidance for Q2, sees Q2 revs of $55-59 bln vs. $58.97 bln S&P Capital IQ Consensus; gross margin between 37-38% vs. 38% ests.

Apple prelim Q1 $4.18 vs $4.17 S&P Capital IQ Consensus Estimate; revs $84.3 bln vs $84.00 bln S&P Capital IQ Consensus Estimate

Apple reports Q1 gross margin of 38.0% versus ests of 38.0% (in line with pre-announcement); sees Q2 gross margins 37-38% versus 38.1% ests and 38.3% last year

Co issues guidance for Q2, sees Q2 revs of $55-59 bln vs. $58.97 bln S&P Capital IQ Consensus; gross margin between 37-38% vs. 38% ests.

H&Mi neljanda kvartali müük oli juba varasemalt teada, täna avaldatud kasuminumber valmistas aga oodatust nõrgema marginaali tõttu pettumuse. Allahindlused küll vähenesid eelneva aasta sama perioodiga võrreldes, ent täiendavaid kulusid tekitasid logistika väljavahetamisega ning ettevõtte ümberpööramisega seotud kulud. Varude tase küll alanes kvartaliga veidi, kuid 17,9% osakaaluna müügist püsib endiselt väga kõrgena (firma eesmärgiks on 12-14%). Dividend jäeti eelmise aasta tasemele ning tegevjuhi sõnul on senised sammud näitamas positiivseid tulemusi. Jooksva kvartali esimese kahe kuu müük kasvas 4%

* H&M 4Q pretax profit SEK4.35 billion vs estimate SEK4.93 billion (range SEK4.33 billion to SEK5.46 billion) (BD).

* H&M says result negatively affected by costs generated in connection with the earlier replacement of logistics systems, but also by activities in preparation for upcoming transitions

* Together with negative year-end effects these costs amounted to ~SEK560m in 4Q

* FY dividend per share SEK9.75 vs. SEK9.75 y/y, estimate SEK8.72 (range SEK4.50 to SEK9.75) (Bloomberg data)

* Board’s reasoning for dividend proposal is that underlying business is showing gradual improvements, investments capex will reduce in 2019 and company remains in strong financial position taking into consideration capital structure target

* 4Q gross margin 54.2%, estimate 54.9% (BD)

* 4Q markdowns in relation to sales -0.6 percentage points

* 4Q stock-in-trade as share of sales excluding VAT 17.9% vs. 18.9% q/q

* In 2019 the H&M group plans a net addition of 175 new stores, of which almost half will consist of newer brands

* Net sales in the period 1 December 2018 to 28 January 2019 increased by 4 percent in local currencies compared to the corresponding period the previous year.

* H&M 4Q pretax profit SEK4.35 billion vs estimate SEK4.93 billion (range SEK4.33 billion to SEK5.46 billion) (BD).

* H&M says result negatively affected by costs generated in connection with the earlier replacement of logistics systems, but also by activities in preparation for upcoming transitions

* Together with negative year-end effects these costs amounted to ~SEK560m in 4Q

* FY dividend per share SEK9.75 vs. SEK9.75 y/y, estimate SEK8.72 (range SEK4.50 to SEK9.75) (Bloomberg data)

* Board’s reasoning for dividend proposal is that underlying business is showing gradual improvements, investments capex will reduce in 2019 and company remains in strong financial position taking into consideration capital structure target

* 4Q gross margin 54.2%, estimate 54.9% (BD)

* 4Q markdowns in relation to sales -0.6 percentage points

* 4Q stock-in-trade as share of sales excluding VAT 17.9% vs. 18.9% q/q

* In 2019 the H&M group plans a net addition of 175 new stores, of which almost half will consist of newer brands

* Net sales in the period 1 December 2018 to 28 January 2019 increased by 4 percent in local currencies compared to the corresponding period the previous year.

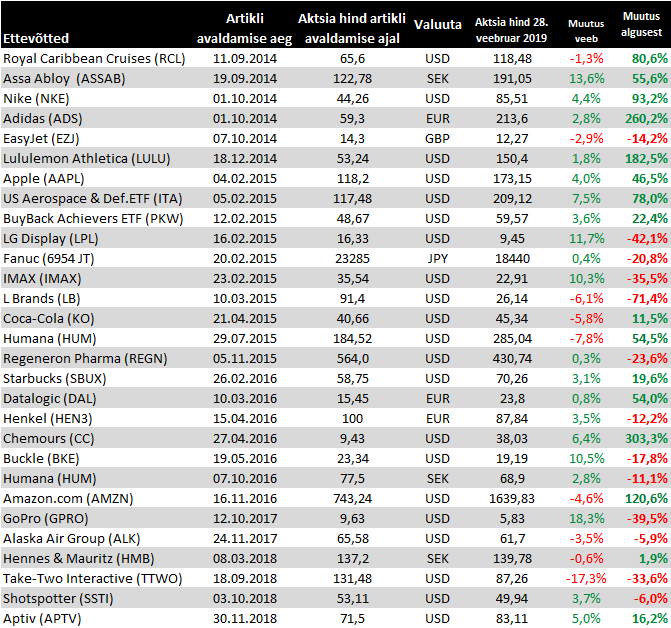

Aptiv lõpetas aasta oodatust paremate numbritega, prognoosib tänavu arvatust veidi tagasihoidlikuma käibe juures konsensuse lähedast aktsiakasumit

Aptiv reports Q4 (Dec) earnings of $1.34 per share, excluding non-recurring items, $0.13 better than the S&P Capital IQ Consensus of $1.21; revenues rose 5.7% year/year to $3.64 bln vs the $3.52 bln S&P Capital IQ Consensus. Adjusted for currency exchange, commodity movements and divestitures, revenue increased by 8% in the fourth quarter. This reflects growth of 18% in North America, 4% in Europe, 2% in Asia and flat performance in South America, our smallest region. Adjusted Operating Income margin was 11.8%, compared to 13.1% in the prior year period, reflecting our continued incremental investments for growth, partially offset by above-market sales growth and the beneficial impacts of cost reduction initiatives.

Co issues downside guidance for Q1, sees EPS of $0.97-1.02, excluding non-recurring items, vs. $1.22 S&P Capital IQ Consensus; sees Q1 revs of $3.4-3.5 bln vs. $3.65 bln S&P Capital IQ Consensus.

Co issues guidance for FY19, sees EPS of $5.25-5.45, excluding non-recurring items, vs. $5.39 S&P Capital IQ Consensus; sees FY19 revs of $14.6-15.0 bln vs. $15.05 bln S&P Capital IQ Consensus.

Aptiv reports Q4 (Dec) earnings of $1.34 per share, excluding non-recurring items, $0.13 better than the S&P Capital IQ Consensus of $1.21; revenues rose 5.7% year/year to $3.64 bln vs the $3.52 bln S&P Capital IQ Consensus. Adjusted for currency exchange, commodity movements and divestitures, revenue increased by 8% in the fourth quarter. This reflects growth of 18% in North America, 4% in Europe, 2% in Asia and flat performance in South America, our smallest region. Adjusted Operating Income margin was 11.8%, compared to 13.1% in the prior year period, reflecting our continued incremental investments for growth, partially offset by above-market sales growth and the beneficial impacts of cost reduction initiatives.

Co issues downside guidance for Q1, sees EPS of $0.97-1.02, excluding non-recurring items, vs. $1.22 S&P Capital IQ Consensus; sees Q1 revs of $3.4-3.5 bln vs. $3.65 bln S&P Capital IQ Consensus.

Co issues guidance for FY19, sees EPS of $5.25-5.45, excluding non-recurring items, vs. $5.39 S&P Capital IQ Consensus; sees FY19 revs of $14.6-15.0 bln vs. $15.05 bln S&P Capital IQ Consensus.

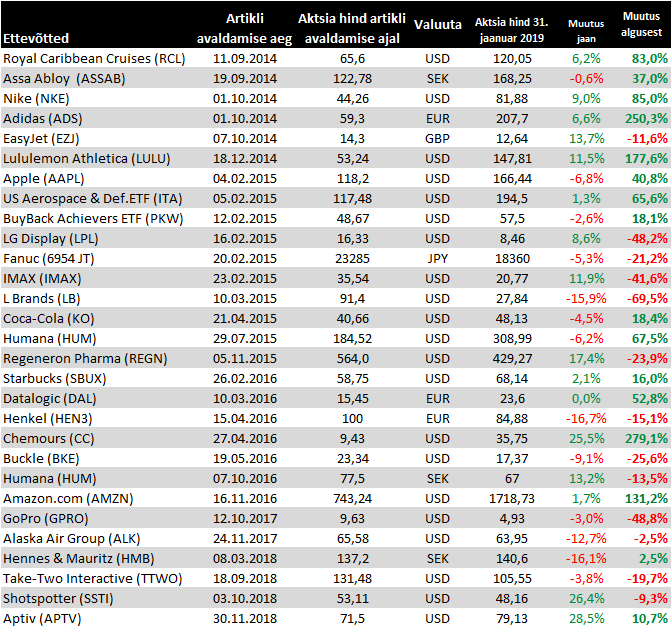

Väikse hilinemisega jaanuari muutused

Coca-Cola neljanda kvartali tulemused osutusid ootuspäraseks, kuid prognoosid valmistavad pettumuse

Coca-Cola reports Q4 (Dec) earnings of $0.43 per share, excluding non-recurring items, in-line with the S&P Capital IQ Consensus of $0.43; revenues fell 5.5% year/year to $7.1 bln vs the $7.07 bln S&P Capital IQ Consensus.

Co issues guidance for FY19, sees EPS of (1%) - 1% to approximately $2.06-2.10 vs. $2.22 S&P Capital IQ Consensus; sees FY19 revs of +3-4% to approximately $32.9-33.2 bln, may not be comparable to $33.51 bln S&P Capital IQ Consensus. FY19 guidance currency headwind based on the current rates and including the impact of hedged positions.

Coca-Cola reports Q4 (Dec) earnings of $0.43 per share, excluding non-recurring items, in-line with the S&P Capital IQ Consensus of $0.43; revenues fell 5.5% year/year to $7.1 bln vs the $7.07 bln S&P Capital IQ Consensus.

Co issues guidance for FY19, sees EPS of (1%) - 1% to approximately $2.06-2.10 vs. $2.22 S&P Capital IQ Consensus; sees FY19 revs of +3-4% to approximately $32.9-33.2 bln, may not be comparable to $33.51 bln S&P Capital IQ Consensus. FY19 guidance currency headwind based on the current rates and including the impact of hedged positions.

Shotspotteri eile avaldatud tulemused osutusid arvatust paremaks, kuid järelkauplemise ajal viis hinna alla esimese kvartali prognoositav kahjum, olgugi et majandusaasta osas kinnitati varasemaid ootusi

Shotspotter reports Q4 (Dec) earnings of $0.03 per share, $0.03 better than the S&P Capital IQ Consensus of ($0.00); revenues rose 49.2% year/year to $9.7 mln vs the $9.47 mln S&P Capital IQ Consensus. The increase in revenues was due to growth in the number of miles covered, which was driven by expanded deployments with current customers as well as the addition of new customers.

Co sees a Q1 net loss vs. $0.00 S&P Capital IQ Consensus.

Co issues guidance for FY19, sees EPS of profitable vs. $0.15 S&P Capital IQ Consensus; sees FY19 revs of $45-47 mln vs. $46.19 mln S&P Capital IQ Consensus.

"We were able to produce 49% topline growth in the fourth quarter along with increased gross margins and solid adjusted EBITDA, which helped us to achieve GAAP profitability for the first time in our company's history. In 2018, we also made significant strides operationally, including the addition of key personnel, an expansion of our sales reach through our strategic reseller agreement with Verizon, augmenting our existing Smart Cities initiative, and the launch of ShotSpotter Missions, which is receiving positive reviews from a number of customers."

Shotspotter reports Q4 (Dec) earnings of $0.03 per share, $0.03 better than the S&P Capital IQ Consensus of ($0.00); revenues rose 49.2% year/year to $9.7 mln vs the $9.47 mln S&P Capital IQ Consensus. The increase in revenues was due to growth in the number of miles covered, which was driven by expanded deployments with current customers as well as the addition of new customers.

Co sees a Q1 net loss vs. $0.00 S&P Capital IQ Consensus.

Co issues guidance for FY19, sees EPS of profitable vs. $0.15 S&P Capital IQ Consensus; sees FY19 revs of $45-47 mln vs. $46.19 mln S&P Capital IQ Consensus.

"We were able to produce 49% topline growth in the fourth quarter along with increased gross margins and solid adjusted EBITDA, which helped us to achieve GAAP profitability for the first time in our company's history. In 2018, we also made significant strides operationally, including the addition of key personnel, an expansion of our sales reach through our strategic reseller agreement with Verizon, augmenting our existing Smart Cities initiative, and the launch of ShotSpotter Missions, which is receiving positive reviews from a number of customers."

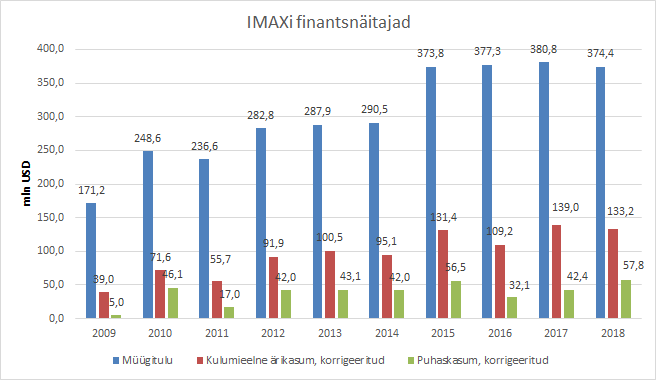

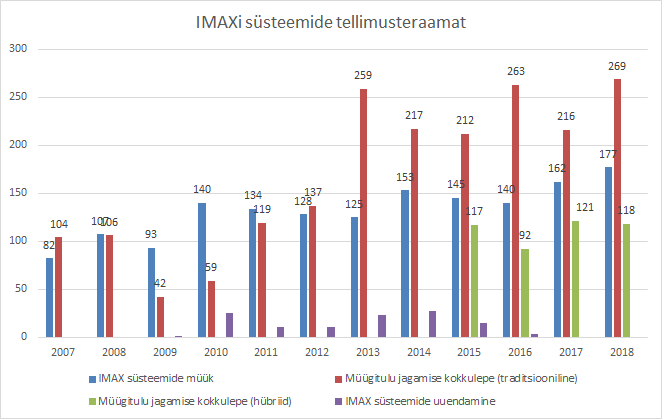

Imax lõpetas eelmise aasta oodatust positiivsemate tulemustega, näidates viimases neljandikus YoY käibe langust peamiselt mdalama filmitulu tõttu, mis moodustas 38% käibest ning kipub sõltuma blockbusteritest. Uusi tellimusi saadi mullu kokku 122 vs 170 2017.a (upgrade'e arvestdes 234 vs 177) ning installeeriti 149 süsteemi vs 165 eelneval aastal, mis kokkuvõttes kergitas aasta lõpuks täitmata tellimuste mahu 499 pealt 564le. Ettevõte ise on tänavuse filmivaliku osas optimistlikult meelestatud.

Imax reports Q4 (Dec) earnings of $0.26 per share, $0.02 better than the S&P Capital IQ Consensus of $0.24; revenues fell 13.2% year/year to $109 mln vs the $101.42 mln S&P Capital IQ Consensus.

"We believe our achievements last year set the stage for IMAX to have a blockbuster year in 2019. We further differentiated The IMAX Experience®, increased awareness of the IMAX brand and tackled key challenges in China, where we delivered our strongest box office year ever and doubled the industry growth rate," said IMAX CEO Richard L. Gelfond. "While these achievements have already begun paying dividends—as evidenced by the 47% year-over-year increase in adjusted earnings per share—we anticipate these initiatives to continue to improve the performance of our business in 2019 and beyond. And we have hit the ground running in 2019. Year-to-to date, we have already achieved $78 million of box office in China, a 61% increase compared to 2018. Overall, we are encouraged by our recent results as we head into the blockbuster filled calendar, which includes highly anticipated films such as Captain Marvel, Avengers: Endgame, The Lion King and Star Wars Episode IX."

Imax reports Q4 (Dec) earnings of $0.26 per share, $0.02 better than the S&P Capital IQ Consensus of $0.24; revenues fell 13.2% year/year to $109 mln vs the $101.42 mln S&P Capital IQ Consensus.

"We believe our achievements last year set the stage for IMAX to have a blockbuster year in 2019. We further differentiated The IMAX Experience®, increased awareness of the IMAX brand and tackled key challenges in China, where we delivered our strongest box office year ever and doubled the industry growth rate," said IMAX CEO Richard L. Gelfond. "While these achievements have already begun paying dividends—as evidenced by the 47% year-over-year increase in adjusted earnings per share—we anticipate these initiatives to continue to improve the performance of our business in 2019 and beyond. And we have hit the ground running in 2019. Year-to-to date, we have already achieved $78 million of box office in China, a 61% increase compared to 2018. Overall, we are encouraged by our recent results as we head into the blockbuster filled calendar, which includes highly anticipated films such as Captain Marvel, Avengers: Endgame, The Lion King and Star Wars Episode IX."

L Brands jätkab pettumuse valmistamist

L Brands reports Q4 (Jan) earnings of $2.14 per share, excluding non-recurring items, $0.07 better than the S&P Capital IQ Consensus of $2.07; revenues rose 0.6% year/year to $4.85 bln vs the $4.9 bln S&P Capital IQ Consensus.

Comps +3% y/y

Co issues downside guidance for Q1, sees EPS of ~$0.00, excluding non-recurring items, vs. $0.13 S&P Capital IQ Consensus.

Co issues downside guidance for FY20, sees EPS of $2.20-2.60, excluding non-recurring items, vs. $2.70 S&P Capital IQ Consensus.

L Brands reports Q4 (Jan) earnings of $2.14 per share, excluding non-recurring items, $0.07 better than the S&P Capital IQ Consensus of $2.07; revenues rose 0.6% year/year to $4.85 bln vs the $4.9 bln S&P Capital IQ Consensus.

Comps +3% y/y

Co issues downside guidance for Q1, sees EPS of ~$0.00, excluding non-recurring items, vs. $0.13 S&P Capital IQ Consensus.

Co issues downside guidance for FY20, sees EPS of $2.20-2.60, excluding non-recurring items, vs. $2.70 S&P Capital IQ Consensus.

Liikumised veebruari lõpu seisuga

Adidase neljanda kvartali tulemused jäid oodatust pisut tagasihoidlikumaks peamiselt Lääne-Euroopa arvatust nõrgema tulemuse tõttu. Käesoeva aasta müügitulu kasv peaks mõnevõrra aglustuma, sest firma on kogemas tugevat nõudlust keskmisest hinnaklassist rõivaste järele, mida ei suudeta pakkumisprobleemide tõttu teenindada. Teine poolaasta peaks sestap nende leevenemisel tooma esimesest poolest kiirema kasvu.

* 4Q revenue EU5.23 billion, estimate EU5.17 billion (range EU5.05 billion to EU5.38 billion) (BD)

* 4Q operating profit EU129 million, estimate EU141.3 million (range EU114.0 million to EU164.0 million) (BD)

* 2018 dividend per share EU3.35, estimate EU3.18 (range EU2.60 to EU3.46) (Bloomberg data)

* 2018 net income cont. ops EU1.71 billion, up 20%

* Adidas sees currency-neutral sales growing 5%-8% in 2019 compared to reported sales growth of 8% in 2018.

* Sees 2019 operating margin +11.3% to +11.5%

* Sees 2019 net income cont. ops rising 10%-14%

* 4Q revenue EU5.23 billion, estimate EU5.17 billion (range EU5.05 billion to EU5.38 billion) (BD)

* 4Q operating profit EU129 million, estimate EU141.3 million (range EU114.0 million to EU164.0 million) (BD)

* 2018 dividend per share EU3.35, estimate EU3.18 (range EU2.60 to EU3.46) (Bloomberg data)

* 2018 net income cont. ops EU1.71 billion, up 20%

* Adidas sees currency-neutral sales growing 5%-8% in 2019 compared to reported sales growth of 8% in 2018.

* Sees 2019 operating margin +11.3% to +11.5%

* Sees 2019 net income cont. ops rising 10%-14%