Vahepeal tagaplaanile vajunud spekulatsioon Amazoni sisenemisest ravimite jaemüügi turule leiab täna kinnitust

Amazon will acquire PillPack; terms not disclosed

PillPack is a pharmacy designed to provide the best possible customer experience in the U.S. for people who take multiple daily prescriptions. PillPack delivers medications in pre-sorted dose packaging, coordinates refills and renewals, and makes sure shipments are sent on time. The parties expect to close the transaction during the second half of 2018.

Nagu Nike juba Q3 ajal tõdes, nägid nad Põhja-Ameerika äri ümberpöördumist, prognoosides toona neljandaks kvartaliks nullkasvu. Tegelikkuses suudeti näidata väikest paranemist.

Nike reports Q4 (May) earnings of $0.69 per share, $0.05 better than the Capital IQ Consensus of $0.64; revenues rose 12.8% year/year to $9.79 bln vs the $9.4 bln Capital IQ Consensus. Revenues for the NIKE Brand were $9.3 billion, up 9 percent on a currency-neutral basis, driven by double-digit increases in NIKE Direct, international geographies, Sportswear, Global Football and growth in North America.

Sales ex-FX: Footwear +8%, Apparel +15%; NA +3%, EMEA +10%, APac/LatAm +13%, China +25%

Announces new $15B buyback when current program is completed in FY19

FY19 revs expectations have moved up slightly to high single digit range (prior mid to high single digit range); expect Q1 revs growth at same level vs +8% consensus

Co expects 2019 gross margin expansion of ~50 basis points or slightly greater (prior guidance for expansion roughly in-line w/ LT financial model of 50-100 bps). Expect less gross margin expansion in 1H

Nike reports Q4 (May) earnings of $0.69 per share, $0.05 better than the Capital IQ Consensus of $0.64; revenues rose 12.8% year/year to $9.79 bln vs the $9.4 bln Capital IQ Consensus. Revenues for the NIKE Brand were $9.3 billion, up 9 percent on a currency-neutral basis, driven by double-digit increases in NIKE Direct, international geographies, Sportswear, Global Football and growth in North America.

Sales ex-FX: Footwear +8%, Apparel +15%; NA +3%, EMEA +10%, APac/LatAm +13%, China +25%

Announces new $15B buyback when current program is completed in FY19

FY19 revs expectations have moved up slightly to high single digit range (prior mid to high single digit range); expect Q1 revs growth at same level vs +8% consensus

Co expects 2019 gross margin expansion of ~50 basis points or slightly greater (prior guidance for expansion roughly in-line w/ LT financial model of 50-100 bps). Expect less gross margin expansion in 1H

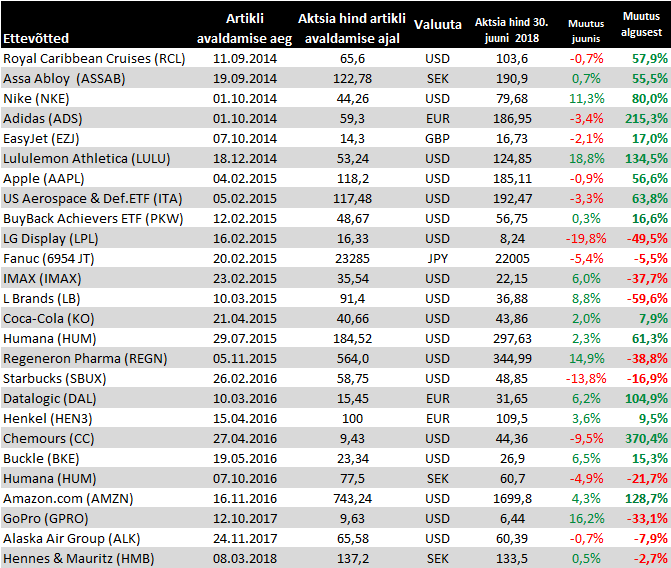

Muutused juuni seisuga

Märtsis Assa Abloy etteotsa valitud uus juht on alustanud Hiina äri korrastamisega, kandes maha 5,6miljardi Rootsi krooni ulatuses ülevõttudega tekkinud immateriaalset vara. Ja kui aasta alguses tekkis lootus, et Hiina tulemused on stabiiseerumas, siis värskemate kommetaaride kohaselt oodatakse nõrkust nii lühi- kui ka keskpikas perspektiivis,.

* Assa Abloy reports one-off non-cash costs of SEK6b in the second quarter, related to its Chinese operations in the Asia Pacific Division.

* One-off costs of SEK5.6b are attributable to impairment of goodwill and other intangible assets, while SEK400m is related to write-downs of operating assets

* Says preliminary 2Q group sales increased 9% to SEK21.14b vs average analyst est. SEK21.03b

* Organic sales growth was 5% vs 2% in year earlier quarter

* Adj. operating profit excluding the announced one-off costs was SEK3.31b vs SEK3.11b a year earlier; adjusted operating margin 15.7% vs 16.1%

* Says the one-off costs "reflect the continued challenging market conditions for new projects in China"

* In updated China strategic review, company expects continued weak earnings in the short- and medium term in the Chinese market

* Still remains firmly committed to Chinese operations, and believes in the long-term earnings potential of this market

* Assa Abloy reports one-off non-cash costs of SEK6b in the second quarter, related to its Chinese operations in the Asia Pacific Division.

* One-off costs of SEK5.6b are attributable to impairment of goodwill and other intangible assets, while SEK400m is related to write-downs of operating assets

* Says preliminary 2Q group sales increased 9% to SEK21.14b vs average analyst est. SEK21.03b

* Organic sales growth was 5% vs 2% in year earlier quarter

* Adj. operating profit excluding the announced one-off costs was SEK3.31b vs SEK3.11b a year earlier; adjusted operating margin 15.7% vs 16.1%

* Says the one-off costs "reflect the continued challenging market conditions for new projects in China"

* In updated China strategic review, company expects continued weak earnings in the short- and medium term in the Chinese market

* Still remains firmly committed to Chinese operations, and believes in the long-term earnings potential of this market

Eelmise postituse jätkuks raporteeris Assa Abloy täna ametlikud teise kvartali tulemused ning kommentaarides tõdeb uus juht, et olukord Hiinas jääb keeruliseks veel mõneks aastaks.

Assa Abloy reported sales for the second quarter that met the average analyst estimate.

* 2Q sales SEK21.14 billion, estimate SEK21.03 billion (range SEK20.42 billion to SEK21.58 billion) (Bloomberg data)

* 2Q organic revenue +5%

* 2Q Operating Income SEK 2.91B, Op. Margin 13.8%

* Continuing with current restructuring programs and, aspreviously announced, expects to launch a new program by end 2018.

The market situation in China continues to be difficult, as previously reported. We expect the operating margin to remain low in the Chinese market for the next few years and this has resulted in a required write-down of SEK 5,595 M for impairment of goodwill and other intangible assets. We also made provisions of SEK 400 M for receivables and inventory in the quarter.

After the events of 2016, our focus was internal and directed to stabilizing the organization. We are now building a focused China organization around our main brands: PanPan, Yale and ASSA ABLOY. China will remain very important to us, and we remain firmly committed to the market. In China we are now seeing continued urbanization, a growing aftermarket for our products, and increasing demand for more advanced security solutions. We are convinced that with our new business strategy in place China will give us good returns in the longer term.

Assa Abloy reported sales for the second quarter that met the average analyst estimate.

* 2Q sales SEK21.14 billion, estimate SEK21.03 billion (range SEK20.42 billion to SEK21.58 billion) (Bloomberg data)

* 2Q organic revenue +5%

* 2Q Operating Income SEK 2.91B, Op. Margin 13.8%

* Continuing with current restructuring programs and, aspreviously announced, expects to launch a new program by end 2018.

The market situation in China continues to be difficult, as previously reported. We expect the operating margin to remain low in the Chinese market for the next few years and this has resulted in a required write-down of SEK 5,595 M for impairment of goodwill and other intangible assets. We also made provisions of SEK 400 M for receivables and inventory in the quarter.

After the events of 2016, our focus was internal and directed to stabilizing the organization. We are now building a focused China organization around our main brands: PanPan, Yale and ASSA ABLOY. China will remain very important to us, and we remain firmly committed to the market. In China we are now seeing continued urbanization, a growing aftermarket for our products, and increasing demand for more advanced security solutions. We are convinced that with our new business strategy in place China will give us good returns in the longer term.

Vaatamata mitmetele lennuliiklust takistanud teguritele (kokku 2606 ära jäänud lendu vs 314 2017.a kolmandas kvartalis), suutis easyJet kasvatada kvartali käivet 14% 1,6 miljardi naelani ning tänu soodsale ärikeskkonnale suveperioodil tõstetakse septembris lõppeva majandusaasta maksueelse kasumi ootust

* 3Q revenue GBP1.6 billion

* 3Q revenue per seat at constant currency +4.8%

* 3Q passengers 24.4 million

* 3Q load factor 93.4%

* 3Q capacity +8.9%

* Sees FY headline profit pretax GBP550 million to GBP590 million, saw GBP530.0 million to GBP580.0 million

* Expects FY Capacity to Grow by C.4.5%

* H2 revenue per seat at constant currency to increase by low to mid-single digits

* Full Year headline cost per seat excluding fuel at constant currency to increase by circa 3% assuming normal levels of disruption in Q4

* 3Q revenue GBP1.6 billion

* 3Q revenue per seat at constant currency +4.8%

* 3Q passengers 24.4 million

* 3Q load factor 93.4%

* 3Q capacity +8.9%

* Sees FY headline profit pretax GBP550 million to GBP590 million, saw GBP530.0 million to GBP580.0 million

* Expects FY Capacity to Grow by C.4.5%

* H2 revenue per seat at constant currency to increase by low to mid-single digits

* Full Year headline cost per seat excluding fuel at constant currency to increase by circa 3% assuming normal levels of disruption in Q4

Coca-Cola teise kvartali käive vähenes osade pudeldajate refrantsiisimise tõttu -8% 8,9 miljardi dollarini (orgaaniline kasv +5%) , millega ületas konsensuse 8,54mld suurust ootust ning sendi võrra suuremaks osutus ka aktsiakasum. Ühtlasi kinnitatakse varasemat prognoosi saavutada tänavu 8-10% aktsiakasumi kasvu.

Reports Q2 (Jun) earnings of $0.61 per share, excluding non-recurring items, $0.01 better than the Capital IQ Consensus of $0.60; revenues fell 8.3% year/year to $8.9 bln vs the $8.54 bln Capital IQ Consensus.

Co reaffirms guidance for FY18, sees EPS of +8-10% to ~$2.06-2.10 vs. $2.08 Capital IQ Consensus Estimate.

FY18 Guidance Details: At least 4% growth in organic revenues (non-GAAP). At least 9% growth in comparable currency neutral operating income (adjusted for structural items and accounting changes) (non-GAAP). Full Year 2018 EPS Comparable EPS from continuing operations (non-GAAP): 8% to 10% growth versus $1.91 in 2017 –

No Change

Reports Q2 (Jun) earnings of $0.61 per share, excluding non-recurring items, $0.01 better than the Capital IQ Consensus of $0.60; revenues fell 8.3% year/year to $8.9 bln vs the $8.54 bln Capital IQ Consensus.

Co reaffirms guidance for FY18, sees EPS of +8-10% to ~$2.06-2.10 vs. $2.08 Capital IQ Consensus Estimate.

FY18 Guidance Details: At least 4% growth in organic revenues (non-GAAP). At least 9% growth in comparable currency neutral operating income (adjusted for structural items and accounting changes) (non-GAAP). Full Year 2018 EPS Comparable EPS from continuing operations (non-GAAP): 8% to 10% growth versus $1.91 in 2017 –

No Change

Amazon raporteeris eile ootuspärase käibe juures arvatust parema aktsiakasumi tänu kõrgema marginaalide äridele (subscription services, AWS ning reklaam). Kolmanda kvartali käibeprognoos jääb analüütikute ootusele alla, kuid teist kvartalit järjest antakse optimistlikum ärikasumi väljavade, mis peegeldab kõrgema marginaalidega üksuste jätkuvat momentumit

Reports Q2 (Jun) earnings of $5.07 per share, $2.54 better than the Capital IQ Consensus of $2.53; revenues rose 39.3% year/year to $52.89 bln vs the $53.37 bln Capital IQ Consensus; operating income +375% to $3.0B vs. $1.76 bln ests and $1.1-1.9B guidance

Breaking down Amazon's businesses further:

Online sales grew 12% to $27.2 bln

Third Party sales grew 36% to $9.7 bln

Subscription services sales grew 55% to $3.4 bln

AWS sales grew 49% to $6.11 bln; operating income grew 79% to $1.6 bln

Advertising revenue grew 132% to $2.2 bln.

Co issue guidance for Q3, sees Q3 revs of $54.0-57.5 bln vs. $58.04 bln Capital IQ Consensus Estimate; operating income $1.4-2.4B vs. $1.3 bln ests

Reports Q2 (Jun) earnings of $5.07 per share, $2.54 better than the Capital IQ Consensus of $2.53; revenues rose 39.3% year/year to $52.89 bln vs the $53.37 bln Capital IQ Consensus; operating income +375% to $3.0B vs. $1.76 bln ests and $1.1-1.9B guidance

Breaking down Amazon's businesses further:

Online sales grew 12% to $27.2 bln

Third Party sales grew 36% to $9.7 bln

Subscription services sales grew 55% to $3.4 bln

AWS sales grew 49% to $6.11 bln; operating income grew 79% to $1.6 bln

Advertising revenue grew 132% to $2.2 bln.

Co issue guidance for Q3, sees Q3 revs of $54.0-57.5 bln vs. $58.04 bln Capital IQ Consensus Estimate; operating income $1.4-2.4B vs. $1.3 bln ests

Apple'i kallimad telefonid lähevad isegi uute ootuses veel üsna hästi kaubaks ning samuti näitas tugevat momentumit teenuste müük, tänu millele suudeti lüüa teise kvartali müügitulu ning kasumiootust. Väljavaade kolmandaks kvartaliks peegeldab korraliku kasvu jätkumist.

Apple reports Q3 (Jun) earnings of $2.34 per share, $0.16 better than the Capital IQ Consensus of $2.18; revenues rose 17.3% year/year to $53.27 bln vs the $52.43 bln Capital IQ Consensus; gross margins 38.3% vs 38.3% ests and 38.5% last year (guidance 38.0-38.5%).

iPhone shipments 41.3 mln vs 42 mln ests vs 41 mln last year, ASP $724 vs. $694 ests

iPad of 11.5 mln vs 11.2 mln ests vs 11.4 mln last year; Macs of 3.7 mln vs 4.3 mln ests vs 4.3 mln units last year.

Service rev +31% to $9.55 bln vs. $9.2 bln ests.

Americas rev +20% to $24.5 bln; Europe +14% to $12.1 bln; China +19% to $9.55 bln; Japan +7% to $3.9 bln, A-Pac +16% to $3.2 bln

Co issues upside guidance for Q4, sees Q4 revs of $60-62 bln vs. $59.4 bln Capital IQ Consensus; gross margins of 38.0-38.5% vs 38.2% ests and 37.9% last year.

"We're thrilled to report Apple's best June quarter ever, and our fourth consecutive quarter of double-digit revenue growth," said Tim Cook, Apple's CEO. "Our Q3 results were driven by continued strong sales of iPhone, Services and Wearables, and we are very excited about the products and services in our pipeline." "Our strong business performance drove revenue growth in each of our geographic segments, net income of $11.5 billion, and operating cash flow of $14.5 billion," said Luca Maestri, Apple's CFO. "We returned almost $25 billion to investors through our capital return program during the quarter, including $20 billion in share repurchases."

Apple reports Q3 (Jun) earnings of $2.34 per share, $0.16 better than the Capital IQ Consensus of $2.18; revenues rose 17.3% year/year to $53.27 bln vs the $52.43 bln Capital IQ Consensus; gross margins 38.3% vs 38.3% ests and 38.5% last year (guidance 38.0-38.5%).

iPhone shipments 41.3 mln vs 42 mln ests vs 41 mln last year, ASP $724 vs. $694 ests

iPad of 11.5 mln vs 11.2 mln ests vs 11.4 mln last year; Macs of 3.7 mln vs 4.3 mln ests vs 4.3 mln units last year.

Service rev +31% to $9.55 bln vs. $9.2 bln ests.

Americas rev +20% to $24.5 bln; Europe +14% to $12.1 bln; China +19% to $9.55 bln; Japan +7% to $3.9 bln, A-Pac +16% to $3.2 bln

Co issues upside guidance for Q4, sees Q4 revs of $60-62 bln vs. $59.4 bln Capital IQ Consensus; gross margins of 38.0-38.5% vs 38.2% ests and 37.9% last year.

"We're thrilled to report Apple's best June quarter ever, and our fourth consecutive quarter of double-digit revenue growth," said Tim Cook, Apple's CEO. "Our Q3 results were driven by continued strong sales of iPhone, Services and Wearables, and we are very excited about the products and services in our pipeline." "Our strong business performance drove revenue growth in each of our geographic segments, net income of $11.5 billion, and operating cash flow of $14.5 billion," said Luca Maestri, Apple's CFO. "We returned almost $25 billion to investors through our capital return program during the quarter, including $20 billion in share repurchases."

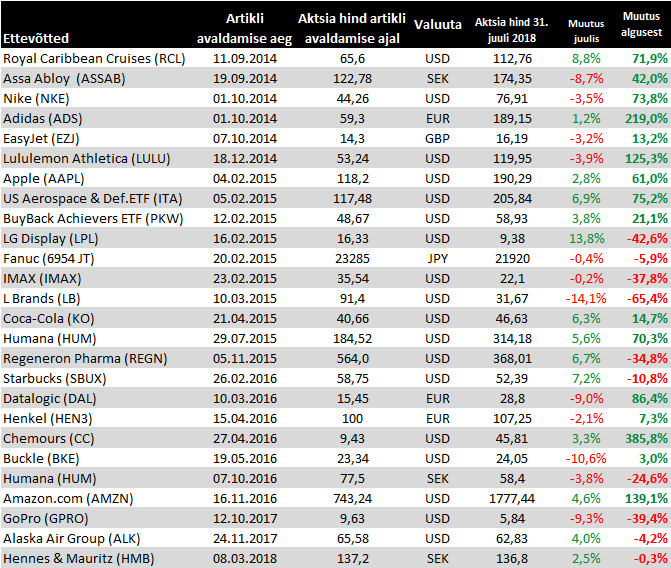

Muutused juuli seisuga

Chemours raporteeris ootuspärase käibe juures arvatust parema aktsiakasumi, usub et 2018.a korrigeeritud EBITDA jääb prognoosi ülemisse äärde ning samuti kinnitati järgneva kolme aasta sihid.

Chemours reports Q2 (Jun) earnings of $1.71 per share, excluding non-recurring items, $0.14 better than the Capital IQ Consensus of $1.57; revenues rose 14.4% year/year to $1.82 bln vs the $1.82 bln Capital IQ Consensus.

"Given our strong first half results and visibility into the rest of 2018, we believe that earnings will be in the top end of our previously announced range. As we look over the longer term, we remain confident in our ability to meet or exceed our three-year financial targets.

Authorized New $750M Share Buyback Program

Increased Div to 25c-Shr From 17c/Shr, Est. 17c

Chemours reports Q2 (Jun) earnings of $1.71 per share, excluding non-recurring items, $0.14 better than the Capital IQ Consensus of $1.57; revenues rose 14.4% year/year to $1.82 bln vs the $1.82 bln Capital IQ Consensus.

"Given our strong first half results and visibility into the rest of 2018, we believe that earnings will be in the top end of our previously announced range. As we look over the longer term, we remain confident in our ability to meet or exceed our three-year financial targets.

Authorized New $750M Share Buyback Program

Increased Div to 25c-Shr From 17c/Shr, Est. 17c

GoPro teatas kardust väiksemast kahjumist teises kvartalis. Tegevjuhi sõnul peaks ettevõte suutma tänu uutele toodetele saavutada aasta teises pooles käibe kasvu ning muutuma ka kasumlikuks,

GoPro reports Q2 (Jun) loss of $0.15 per share, excluding non-recurring items, $0.07 better than the Capital IQ Consensus of ($0.22); revenues fell 4.7% year/year to $282.7 mln vs the $270.27 mln Capital IQ Consensus

"GoPro is executing," said founder and CEO Nicholas Woodman. "We are on track; sell-through is solid in all regions indicating strong demand, and we believe GoPro will be profitable in the second half of 2018. Our plan is to exit the year with an improved margin profile we believe translates into a profitable 2019."

Q3: Sees revs of $260-280 mln vs $268.18 mln Capital IQ Consensus Estimate; GM 34% +/- 1%

Q4: Sees revs of $380-400 mln vs $402.05 mln Capital IQ Consensus Estimate; GM 40% +/- 1%

GoPro reports Q2 (Jun) loss of $0.15 per share, excluding non-recurring items, $0.07 better than the Capital IQ Consensus of ($0.22); revenues fell 4.7% year/year to $282.7 mln vs the $270.27 mln Capital IQ Consensus

"GoPro is executing," said founder and CEO Nicholas Woodman. "We are on track; sell-through is solid in all regions indicating strong demand, and we believe GoPro will be profitable in the second half of 2018. Our plan is to exit the year with an improved margin profile we believe translates into a profitable 2019."

Q3: Sees revs of $260-280 mln vs $268.18 mln Capital IQ Consensus Estimate; GM 34% +/- 1%

Q4: Sees revs of $380-400 mln vs $402.05 mln Capital IQ Consensus Estimate; GM 40% +/- 1%

L Brandsi oodatust nõrgemad prognoosid ei paku paraku märke, et äritegevus võiks lähiajal ümber pöörata

Reports Q2 (Jul) earnings of $0.36 per share, $0.01 better than the S&P Capital IQ Consensus of $0.35; revenues rose 8.3% year/year to $2.98 bln vs the $2.92 bln S&P Capital IQ Consensus. Guided EPS to high end of $0.30-0.35 guidance with comps +3% on August 10.

Co issues downside guidance for Q3, sees EPS of $0.00-0.05 vs. $0.15 S&P Capital IQ Consensus.

Co issues downside guidance for FY19, lowers EPS to $2.45-2.70 from $2.70-3.00 vs. $2.77 S&P Capital IQ Consensus.

Reports Q2 (Jul) earnings of $0.36 per share, $0.01 better than the S&P Capital IQ Consensus of $0.35; revenues rose 8.3% year/year to $2.98 bln vs the $2.92 bln S&P Capital IQ Consensus. Guided EPS to high end of $0.30-0.35 guidance with comps +3% on August 10.

Co issues downside guidance for Q3, sees EPS of $0.00-0.05 vs. $0.15 S&P Capital IQ Consensus.

Co issues downside guidance for FY19, lowers EPS to $2.45-2.70 from $2.70-3.00 vs. $2.77 S&P Capital IQ Consensus.

Morgan Stanley tõstab Amazoni hinnasihi 1850 pealt 2500 peale, bull case 3150 dollarit nüüd

We see AMZN's rapidly growing, high margin revs allowing it to continue to invest while also generating higher profits. We adjust our PT methodology to a 5-part sum-of-the-parts that more accurately captures the profit impact of these businesses. Our $2,500 PT represents ~30% upside.

We see AMZN's rapidly growing, high margin revs allowing it to continue to invest while also generating higher profits. We adjust our PT methodology to a 5-part sum-of-the-parts that more accurately captures the profit impact of these businesses. Our $2,500 PT represents ~30% upside.

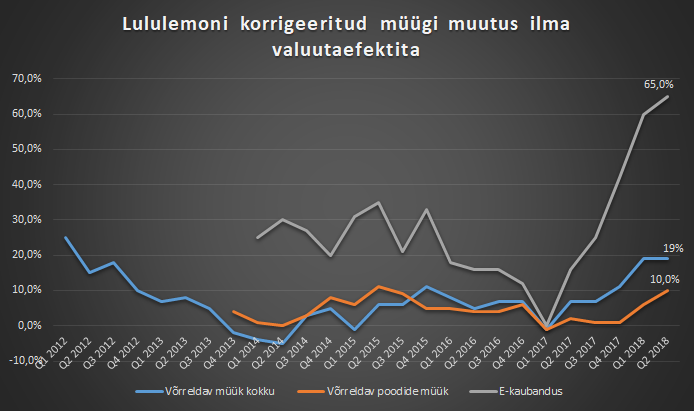

Lululemon jätkab head hoogu tänu tooteinnovatsioonile, mille tulemusel püsis võrreldav müük teises kvartalis 19% peal ning kasumirida toetas omakorda brutokasumimarginaali paranemine aastaga 320 baaspunkti võrra 54,8%le ning ärikasumimarginaali tõus 570 baaspunkti võrra 18,5%le. Nõnda jätkatakse 2020 visiooni elluviimist, mis näeb ette selleks ajaks müügituluga 4 miljardi dollarini jõudmise (2017.a 2,6 mld) ning tänastelt tasemetelt marginaalide edasist parandamist.

Lululemon reports Q2 (Jul) earnings of $0.71 per share, $0.22 better than the S&P Capital IQ Consensus of $0.49; revenues rose 24.5% year/year to $723.5 mln vs the $667.83 mln S&P Capital IQ Consensus. Comps 20% vs 9.6% estimate

Co issues upside guidance for Q3, sees EPS of $0.65-0.67 vs. $0.63 S&P Capital IQ Consensus; sees Q3 revs of $720-730 mln vs. $707.41 mln S&P Capital IQ Consensus.

Co issues upside guidance for FY19, sees EPS of $3.45-3.53 vs. $3.24 S&P Capital IQ Consensus; sees FY19 revs of $3.185-3.235 bln vs. $3.09 bln S&P Capital IQ Consensus.

Lululemon reports Q2 (Jul) earnings of $0.71 per share, $0.22 better than the S&P Capital IQ Consensus of $0.49; revenues rose 24.5% year/year to $723.5 mln vs the $667.83 mln S&P Capital IQ Consensus. Comps 20% vs 9.6% estimate

Co issues upside guidance for Q3, sees EPS of $0.65-0.67 vs. $0.63 S&P Capital IQ Consensus; sees Q3 revs of $720-730 mln vs. $707.41 mln S&P Capital IQ Consensus.

Co issues upside guidance for FY19, sees EPS of $3.45-3.53 vs. $3.24 S&P Capital IQ Consensus; sees FY19 revs of $3.185-3.235 bln vs. $3.09 bln S&P Capital IQ Consensus.

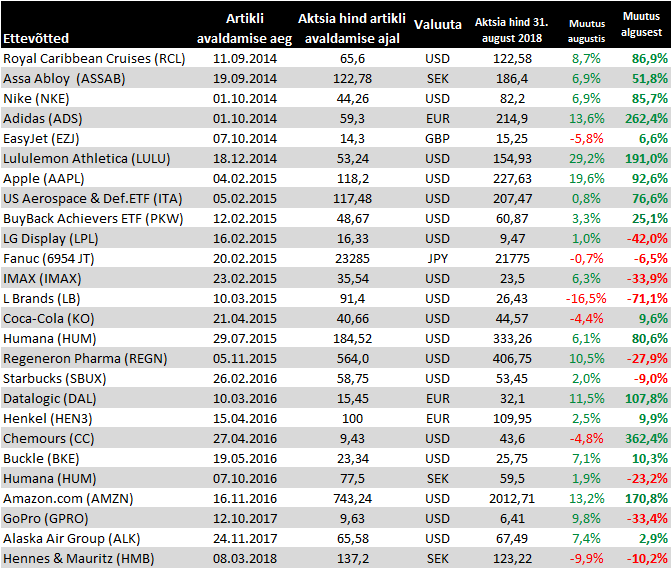

31. augusti seisuga

H&M pakub täna häid uudiseid, raporteerides oodatust parema kolmanda kvartali müügi. Täpsemad detailid selguvad 27. septembril, kuid ettevõte hoiatab, et uute logistikasüsteemide juurutamine tõi osadel olulistel turgudel kaasa tagasilöögi müügile ja kuludele.

3Q sales SEK55.82 billion, estimate SEK54.03 billion (range SEK53.22 billion to SEK55.49 billion) (Bloomberg data)

Says that sales and cost development in some of the group’s important markets, such as the U.S., France, Italy and Belgium were in the third quarter considerably affected by the issues that emerged during the implementation of new logistics systems in the spring

3Q sales SEK55.82 billion, estimate SEK54.03 billion (range SEK53.22 billion to SEK55.49 billion) (Bloomberg data)

Says that sales and cost development in some of the group’s important markets, such as the U.S., France, Italy and Belgium were in the third quarter considerably affected by the issues that emerged during the implementation of new logistics systems in the spring

Lisan Take-Two Interactive'i siia nimekirja, kuna saab olema huvitav näha, kui edukalt suudab Red Dead Redemption 2 kõrgeid ootusi täita ning kujuneda firma jaoks GTA kõrvale veel üheks oluliseks taasesineva müügitulu allikaks GTA looja toob turule aasta oodatuima mängu

Nike avaldas eile ootuspärase esimese kvartali käibe juures arvatust veidi kõrgema aktsiakasumi ning näeb sarnaste positiivsete trendide jätkumist ülejäänud fiskaalaastal. Kuna aktsia on viimase kahe kuu lõikes üsna jõuliselt üles liikunud ning näitas järelkauplemise ajal miinust, siis lootsid ilmselt paljud optimistlikumat väljavaadet.

Nike reports Q1 (Aug) earnings of $0.67 per share, $0.04 better than the S&P Capital IQ Consensus of $0.63; revenues rose 9.7% year/year to $9.95 bln vs the $9.92 bln S&P Capital IQ Consensus. EPS +18%, driven by strong revenue growth, gross margin expansion, selling and administrative expense leverage, and a lower average share count, partially offset by a higher effective tax rate.

North American revenue ex-FX +6% to $4.1B, EMEA +9% to $2.6B, Greater China +20% to $1.4B, APacLatAM +14% to $1.3B

Gross margin increased 50 bps to 44.2% vs. 44.3% estimates, primarily due to higher average selling prices, favorable full-price sales mix and margin expansion in NIKE Direct, partially offset by higher product costs.

NIKE discusses Q2 outlook - expects FX neutral revenue growth to be in-line with Q1 9% growth (current Q2 consensus is +8.3%)

NIKE maintains full year guidance. Prior guidance was for FY19 revs up slightly to high single digit range; gross margin expansion of ~50 basis points or slightly greater (LT financial model of 50-100 bps).

Nike reports Q1 (Aug) earnings of $0.67 per share, $0.04 better than the S&P Capital IQ Consensus of $0.63; revenues rose 9.7% year/year to $9.95 bln vs the $9.92 bln S&P Capital IQ Consensus. EPS +18%, driven by strong revenue growth, gross margin expansion, selling and administrative expense leverage, and a lower average share count, partially offset by a higher effective tax rate.

North American revenue ex-FX +6% to $4.1B, EMEA +9% to $2.6B, Greater China +20% to $1.4B, APacLatAM +14% to $1.3B

Gross margin increased 50 bps to 44.2% vs. 44.3% estimates, primarily due to higher average selling prices, favorable full-price sales mix and margin expansion in NIKE Direct, partially offset by higher product costs.

NIKE discusses Q2 outlook - expects FX neutral revenue growth to be in-line with Q1 9% growth (current Q2 consensus is +8.3%)

NIKE maintains full year guidance. Prior guidance was for FY19 revs up slightly to high single digit range; gross margin expansion of ~50 basis points or slightly greater (LT financial model of 50-100 bps).

Nagu H&M juba hoiatas, mõjutasid logistikaprobleemid kolmanda kvartali kasumit. Varud on endiselt väga kõrged, kuid tegevjuhi sõnul on varude tasakaal paranenud ning mitmed märgid viitavad, et nad liiguvad õiges suunas.

H&M 3Q PRETAX SEK4.01B, EST. SEK4.20B

H&M 3Q GROSS MARGIN +50.3%, EST. +50.2%

Logistics problems affected store sales in U.S., France, Italy and Belgium and resulted in extraordinary costs of around SEK400m in 3Q

Online sales rose more than 30% in 3Q; H&M is now online in 47 markets

H&M’s stock-in-trade rose 15% in 3Q y/y to SEK38.7b and was up 12% in local currencies.

* The stock-in-trade amounted to 18.9% of sales excluding VAT vs 18.2% in 2Q and 16.6% in 3Q a year earlier

* Says the "inventory level is still high, but the quality and balance is better than at the same point last year"

* "One sign that the group’s improvement work is starting to bear fruit is that stock turnover on new products is gradually increasing"

* Says the overall inventory situation "is entirely manageable"

* Company assess that markdowns in relation to sales will not increase in 4Q compared with the same period last year.

H&M 3Q PRETAX SEK4.01B, EST. SEK4.20B

H&M 3Q GROSS MARGIN +50.3%, EST. +50.2%

Logistics problems affected store sales in U.S., France, Italy and Belgium and resulted in extraordinary costs of around SEK400m in 3Q

Online sales rose more than 30% in 3Q; H&M is now online in 47 markets

H&M’s stock-in-trade rose 15% in 3Q y/y to SEK38.7b and was up 12% in local currencies.

* The stock-in-trade amounted to 18.9% of sales excluding VAT vs 18.2% in 2Q and 16.6% in 3Q a year earlier

* Says the "inventory level is still high, but the quality and balance is better than at the same point last year"

* "One sign that the group’s improvement work is starting to bear fruit is that stock turnover on new products is gradually increasing"

* Says the overall inventory situation "is entirely manageable"

* Company assess that markdowns in relation to sales will not increase in 4Q compared with the same period last year.