Starbucks raporteeris ootuspärased numbrid ning kinnitas varasemat majandusaasta prognoosi. Kvartali jooksul täheldati võrreldava müügikasvu kiirenemist, mis on küll positiivne, kuid ilmselt ei kiirustata selle baasil veel põhjapanevaid järeldusi tegema

--Starbucks reports Q2 (Mar) earnings of $0.53 per share, excluding non-recurring items, in-line with the Capital IQ Consensus of $0.53; revenues rose 13.9% year/year to $6.03 bln vs the $5.93 bln Capital IQ Consensus.

---Global comparable store sales increased 2%, driven by a 3% increase in average ticket Americas and U.S. comp store sales increased 2%

--Co reaffirms guidance for FY18, sees EPS of $2.48-2.53, excluding non-recurring items, vs. $2.49 Capital IQ Consensus Estimate

--Continue to expect consolidated revenuegrowth in the high single digits when excluding approximately 2 points of net favorability from the East China acquisition and other streamline-driven activities

--Continue to expect 3-5% comparable store sales growth globally, expect to be near the low end of the range for the year

Starbucks On Call says Q2 comps accelerated throughout the quarter in both US and China; co went from comps of under 1% in January to over 3% in February/March

Amazonilt arvatust paremad Q1 tulemused ning teise kvartali ärikasumi väljavaade. Ettevõtte peamise kasumiallika AWSi käibe kasv kiirenes neljanda kvartali 45% pealt 49%le, ning "other" alla käiv reklaamitulu 60% pealt 132%le (Morgan Stanley kohaselt oli segmendi kasv 73% ilma raamatupidamisliku kasuta). Lisaks teatati USA Prime teenuse aastase tasu tõstmisest 20 dollari võrra 119 dollarile, pakkudes selle eest suuremat juurdepääsu meediatoodangule ja laiendades ka kahepäevase tarnega kaupade valikut.

Amazon reports Q1 (Mar) earnings of $3.27 per share, $2.02 better than the Capital IQ Consensus of $1.25; revenues rose 42.9% year/year to $51.04 bln vs the $49.94 bln Capital IQ Consensus. Operating income +92% to $1.93 bln vs. $1.04 bln ests and $0.30-1.0 bln guidance. Operating cash flow increased 4% to $18.2 billion for the trailing twelve months.

Amazon sees Q2 revs $51-54 mln vs $52.24 bln Capital IQ Consensus Estimate; operating income $1.1-1.9 bln vs. $1.14 bln ests

Amazon reports Q1 (Mar) earnings of $3.27 per share, $2.02 better than the Capital IQ Consensus of $1.25; revenues rose 42.9% year/year to $51.04 bln vs the $49.94 bln Capital IQ Consensus. Operating income +92% to $1.93 bln vs. $1.04 bln ests and $0.30-1.0 bln guidance. Operating cash flow increased 4% to $18.2 billion for the trailing twelve months.

Amazon sees Q2 revs $51-54 mln vs $52.24 bln Capital IQ Consensus Estimate; operating income $1.1-1.9 bln vs. $1.14 bln ests

IMAXilt oodatust paremad tulemused tänu filmide suuremale kassatulule ning installeeritud süsteemide kasvule. Kasumirida toetas lisaks rangem kulude kontroll. Teise kvartali on paljuluvavalt avanud Avengers: Infinity War edukas sooritus

Imax reports Q1 (Mar) earnings of $0.21 per share, excluding non-recurring items, $0.10 better than the Capital IQ Consensus of $0.11; revenues rose 23.7% year/year to $85 mln vs the $81.64 mln Capital IQ Consensus.

Avengers: Infinity War, which marks the first Hollywood film to ever be shot entirely with IMAX cameras, opened in IMAX theatres with a record-setting $41.5 million weekend global debut on 715 screens (excluding China), making it the best-ever IMAX opening for a Marvel title and the third largest IMAX opening of all time.

Imax reports Q1 (Mar) earnings of $0.21 per share, excluding non-recurring items, $0.10 better than the Capital IQ Consensus of $0.11; revenues rose 23.7% year/year to $85 mln vs the $81.64 mln Capital IQ Consensus.

Avengers: Infinity War, which marks the first Hollywood film to ever be shot entirely with IMAX cameras, opened in IMAX theatres with a record-setting $41.5 million weekend global debut on 715 screens (excluding China), making it the best-ever IMAX opening for a Marvel title and the third largest IMAX opening of all time.

Apple aitas oodatust paremate teise kvartali numbrite ning kolmanda kvartali müügitulu prognoosiga leevendada analüütikute ja investorite hirmu. Ettevõte prioritiseerib kapitali tagastamisel aktsiate tagasioste, kuna juhtkonna arvates on aktsia odav.

Apple reports Q2 (Mar) earnings of $2.73 per share, $0.05 better than the Capital IQ Consensus of $2.68; revenues rose 15.6% year/year to $61.14 bln vs the $60.94 bln Capital IQ Consensus; gross margins of 38.3% versus 38.5% ests (guidance 38.0-38.5%)

iPhone shipments 52.2 mln versus 52 mln ests & 50.8 mln last year.

iPad shipments 9.1 mln versus 8.8 mln ests & 10.2 mln last year; Mac shipments 4.1 mln versus 4.1 mln ests & 4.2 mln last year

Americas rev +17% to $24.8 bln; Europe +9% to $13.85 bln; China +21% to $13.0 bln; Japan +22% to $5.5 bln, other Asia/Pac +4% to $3.96 bln.

Co issues upside guidance for Q3, sees Q3 revs of $51.5-53.5 bln vs. $51.51 bln Capital IQ Consensus Estimate; gross margins of 38.0-38.5% versus 38.4% ests vs 38.5% last year.

Adds $100 bln to share repurchase; raises dividend 16% to $0.73/share

Apple reports Q2 (Mar) earnings of $2.73 per share, $0.05 better than the Capital IQ Consensus of $2.68; revenues rose 15.6% year/year to $61.14 bln vs the $60.94 bln Capital IQ Consensus; gross margins of 38.3% versus 38.5% ests (guidance 38.0-38.5%)

iPhone shipments 52.2 mln versus 52 mln ests & 50.8 mln last year.

iPad shipments 9.1 mln versus 8.8 mln ests & 10.2 mln last year; Mac shipments 4.1 mln versus 4.1 mln ests & 4.2 mln last year

Americas rev +17% to $24.8 bln; Europe +9% to $13.85 bln; China +21% to $13.0 bln; Japan +22% to $5.5 bln, other Asia/Pac +4% to $3.96 bln.

Co issues upside guidance for Q3, sees Q3 revs of $51.5-53.5 bln vs. $51.51 bln Capital IQ Consensus Estimate; gross margins of 38.0-38.5% versus 38.4% ests vs 38.5% last year.

Adds $100 bln to share repurchase; raises dividend 16% to $0.73/share

Adidase esimese kvartali müügitulu jäi oodatust pisut lahjemaks, kuid tänu kõrgematele hindadele ning müügi paremele jagunemisele toodete ja riikide lõikes suudeti ärikasumi real näidata arvatust paremat tulemust.

* 1Q revenue EU5.55 billion, estimate EU5.62 billion (range EU5.53 billion to EU5.74 billion) (BD)

* 1Q operating profit EU746 million, estimate EU710.7 million (range EU689.0 million to EU744.0 million) (Bloomberg data)

* 1Q gross margin +51.1%, estimate +50.5% (BD)

* 1Q operating margin 13.4%

* 1Q net income from continuing ops EU542 million

* 1Q revenues grow 10% currency-neutral, gross margin increases 1.5pp, operating margin improves 1.8pp to 13.4%

* 2018 Outlook Confirmed: Still See '18 Sales up ABT 10%, Gross Margin up to 50.7%

* 1Q revenue EU5.55 billion, estimate EU5.62 billion (range EU5.53 billion to EU5.74 billion) (BD)

* 1Q operating profit EU746 million, estimate EU710.7 million (range EU689.0 million to EU744.0 million) (Bloomberg data)

* 1Q gross margin +51.1%, estimate +50.5% (BD)

* 1Q operating margin 13.4%

* 1Q net income from continuing ops EU542 million

* 1Q revenues grow 10% currency-neutral, gross margin increases 1.5pp, operating margin improves 1.8pp to 13.4%

* 2018 Outlook Confirmed: Still See '18 Sales up ABT 10%, Gross Margin up to 50.7%

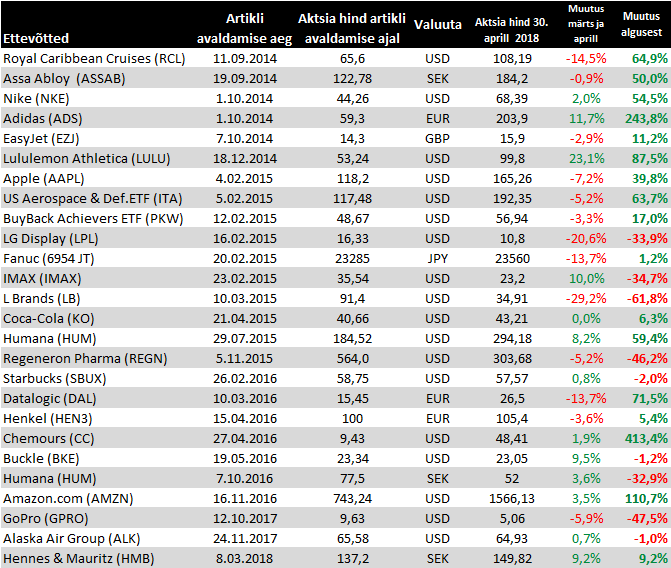

Ülevaade aprilli lõpu seisuga

Buffett suurendas Apple'i aktsiate arvu kvartaliga ligi poole võrra

Buffett's Berkshire Hathaway bought stunning 75 million Apple shares in first quarter

Buffett's Berkshire Hathaway bought stunning 75 million Apple shares in first quarter

GoPro sõnul oli HERO5 ja HERO6 Black läbimüük esimses kvartalis hea pärast hindade langetamist ja samuti hinnati julgustavaks hiljuti turule toodud odavama hinnaklassi HERO vastuvõttu, mis kokkuvõttes aitasid ettevõttel raporteerida kardetust parema käibe juures pisut väiksema kahjumi. Kuna GoPro on investorite ootusi varem korduvalt alt vedanud, siis tõenäoliselt tahetakse järgnevatel kvartalitel näha, kas progressi suudetakse hoida ja teisel poolaastal tulevad uued toode saavad olema piisavalt innovatiivsed.

GoPro reports Q1 (Mar) loss of $0.34 per share, excluding non-recurring items, $0.02 better than the Capital IQ Consensus of ($0.36); revenues fell 7.4% year/year to $202.35 mln vs the $182.26 mln Capital IQ Consensus.

GoPro reports Q1 (Mar) loss of $0.34 per share, excluding non-recurring items, $0.02 better than the Capital IQ Consensus of ($0.36); revenues fell 7.4% year/year to $202.35 mln vs the $182.26 mln Capital IQ Consensus.

Nestle hakkab müüma Starbucksi tooteid ning annab selle eest 7,2mld dollarit, mida Starbucks kasutab aktsiate tagasiostu programmi kiirendamiseks

Nestle Pays $7.2 Billion to Sell Coffee With Starbucks Brand

Nestle Pays $7.2 Billion to Sell Coffee With Starbucks Brand

Henkeli võrreldava müügi 1,1% kasv ületas pisut konsensuse 0,7% ootust, valuuta tugev negatiivne mõju jõudis aktsiakasumit eelmise aasta taseme lähedal

* 1Q Sales at 4,835 million euros (Est. EU4.92B): organic growth +1.1%, nominal -4.5%, impacted by negative currency effects of 8.6%

* 1Q Adj. Ebit EU842M, Est. EU850M

* 1Q adjusted EPS EU1.43, estimate EU1.43 (range EU1.34 to EU1.47) (BD)

* Still Sees 2018 Organic Sales up 2-4%, Adj. EPS up 5-8%

* "In the first quarter, we were confronted with exceptionally negative currency effects, which impacted our reported sales with 8.6 percent or about 440 million euros. Our operating profit and earnings per share were also affected by the adverse currency developments": CEO Hans Van Bylen

* On track to return to normal service levels in North America 2q

* 1Q Sales at 4,835 million euros (Est. EU4.92B): organic growth +1.1%, nominal -4.5%, impacted by negative currency effects of 8.6%

* 1Q Adj. Ebit EU842M, Est. EU850M

* 1Q adjusted EPS EU1.43, estimate EU1.43 (range EU1.34 to EU1.47) (BD)

* Still Sees 2018 Organic Sales up 2-4%, Adj. EPS up 5-8%

* "In the first quarter, we were confronted with exceptionally negative currency effects, which impacted our reported sales with 8.6 percent or about 440 million euros. Our operating profit and earnings per share were also affected by the adverse currency developments": CEO Hans Van Bylen

* On track to return to normal service levels in North America 2q

Konkurentide probleemid, lihavõtete osaline liikumine esimesse poolaastasse ning üleüldine soodne ärikeskkond aitasid Easyjetil kasvatada esimese poolaasta käivet ligi 20% 2,18 miljardi naelani.Maksueelset kahjumit suudeti oluliselt vähendada vaatamata Berliini lennujaamas laienemisega seotud kulutustele. Ettevõte kavatseb mitmete fookusinvesteeringutega tõsta kasumlikkust ning näeb terve aasta perspektiivis konsensusest kõrgemat maksueelse ärikasumit.

1H revenue GBP2.18 billion, estimate GBP2.11 billion (BD)

1H pretax loss GBP18 million, estimate loss GBP72.0 million (Bloomberg data), an improvement of £194 million YoY

1H operating loss GBP10 million, estimate loss GBP11.5 million (BD) (2 estimates)

Forward Bookings Are Ahead of Last Yr

Sees FY pretax profit GBP530 million to GBP580 million, Bloomberg FY pretax consensus est. is GBP493m

Turning to our strategy, I have today announced an increase in investment in easyJet Holidays to gain a greater

share of that market, showcased a series of initiatives to increase the number of passengers travelling on business

and revealed plans to introduce a new loyalty programme which will support and reinforce all of these initiatives

and will further increase passenger loyalty to easyJet. I also outlined new investments to harness the power of

our data to improve our customer proposition, reduce costs and increase revenue. All of these initiatives will

provide higher profit per seat and higher returns for our shareholders.

1H revenue GBP2.18 billion, estimate GBP2.11 billion (BD)

1H pretax loss GBP18 million, estimate loss GBP72.0 million (Bloomberg data), an improvement of £194 million YoY

1H operating loss GBP10 million, estimate loss GBP11.5 million (BD) (2 estimates)

Forward Bookings Are Ahead of Last Yr

Sees FY pretax profit GBP530 million to GBP580 million, Bloomberg FY pretax consensus est. is GBP493m

Turning to our strategy, I have today announced an increase in investment in easyJet Holidays to gain a greater

share of that market, showcased a series of initiatives to increase the number of passengers travelling on business

and revealed plans to introduce a new loyalty programme which will support and reinforce all of these initiatives

and will further increase passenger loyalty to easyJet. I also outlined new investments to harness the power of

our data to improve our customer proposition, reduce costs and increase revenue. All of these initiatives will

provide higher profit per seat and higher returns for our shareholders.

Kui L Brandsi esimese kvartali tulemused olid suuresti eelinfo baasil juba teada, siis negatiivne üllatus peitus arvatust madalamates prognoosides, mis näitab, et ettevõttel on raskusi saavutada tihenenud konkurentsis ja tarbijate muutunud eelistustega keskkonnas Victoria's Secreti pesu samasugust läbilööki nagu kunagi headel aegadel

L Brands reports Q1 (Apr) earnings of $0.17 per share, $0.02 better than the Capital IQ Consensus of $0.15; revenues rose 7.8% year/year to $2.63 bln vs the $2.59 bln Capital IQ Consensus.

Co issues downside guidance for Q2 (Jul), sees EPS of $0.30-0.35 vs. $0.40 Capital IQ Consensus Estimate.

Co issues downside guidance for FY19, sees EPS of $2.70-3.00 vs. $3.01 Capital IQ Consensus Estimate and vs prior guidance of $2.95-3.25.

L Brands reports Q1 (Apr) earnings of $0.17 per share, $0.02 better than the Capital IQ Consensus of $0.15; revenues rose 7.8% year/year to $2.63 bln vs the $2.59 bln Capital IQ Consensus.

Co issues downside guidance for Q2 (Jul), sees EPS of $0.30-0.35 vs. $0.40 Capital IQ Consensus Estimate.

Co issues downside guidance for FY19, sees EPS of $2.70-3.00 vs. $3.01 Capital IQ Consensus Estimate and vs prior guidance of $2.95-3.25.

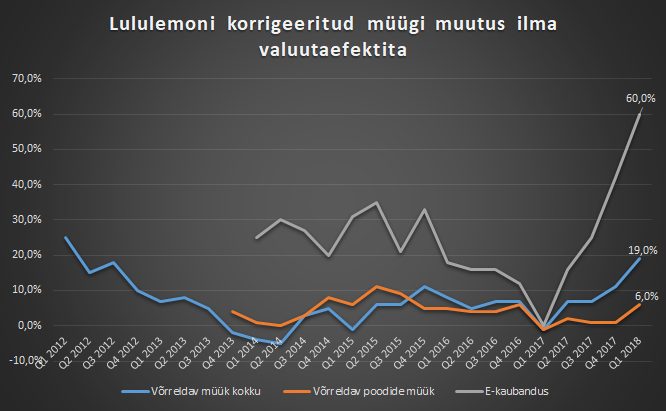

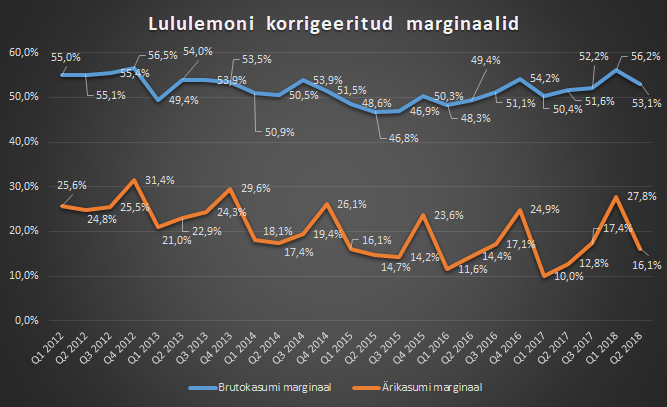

Lululemoni esimese kvartali tulemustele vastu minnes olid ootused kahtlemata kõrged, kuid ettevõte suutis neid ületadad ning lisaks kergitatati prognoose. Vaatamata sellele, et ettevõte jätkuvalt otsib endale uut juhti ning konkurents on spordirõivaste turul karm, müüvad firma tooted piisvalt hästi, et särada esimeses kvartalis võrreldava müügi 19% kasvuga (saades osaliselt tuge madalast võrdlusbaasist) ning mullusest tugevamate marginaalidega.

Lululemon reports Q1 (Apr) earnings of $0.55 per share, $0.09 better than the Capital IQ Consensus of $0.46; revenues rose 24.9% year/year to $649.7 mln vs the $616.69 mln Capital IQ Consensus

Comparable sales increase 20%, or 19% on a constant dollar basis

Co issues upside guidance for Q2, sees EPS of $0.46-0.48 vs. $0.44 Capital IQ Consensus Estimate; sees Q2 revs of $660-665 mln vs. $645.22 mln Capital IQ Consensus Estimate; Q2 sales forecast based on a total comparable sales increase in the high single digits on a constant dollar basis

Co raises guidance for FY19, sees EPS of $3.10-3.18 vs. $3.09 Capital IQ Consensus Estimate; sees FY19 revs of $3.04-3.08 bln vs. $3.03 bln Capital IQ Consensus Estimate; FY19 sales forecast based on a total comparable sales increase in the high single digits on a constant dollar basis

Lululemon reports Q1 (Apr) earnings of $0.55 per share, $0.09 better than the Capital IQ Consensus of $0.46; revenues rose 24.9% year/year to $649.7 mln vs the $616.69 mln Capital IQ Consensus

Comparable sales increase 20%, or 19% on a constant dollar basis

Co issues upside guidance for Q2, sees EPS of $0.46-0.48 vs. $0.44 Capital IQ Consensus Estimate; sees Q2 revs of $660-665 mln vs. $645.22 mln Capital IQ Consensus Estimate; Q2 sales forecast based on a total comparable sales increase in the high single digits on a constant dollar basis

Co raises guidance for FY19, sees EPS of $3.10-3.18 vs. $3.09 Capital IQ Consensus Estimate; sees FY19 revs of $3.04-3.08 bln vs. $3.03 bln Capital IQ Consensus Estimate; FY19 sales forecast based on a total comparable sales increase in the high single digits on a constant dollar basis

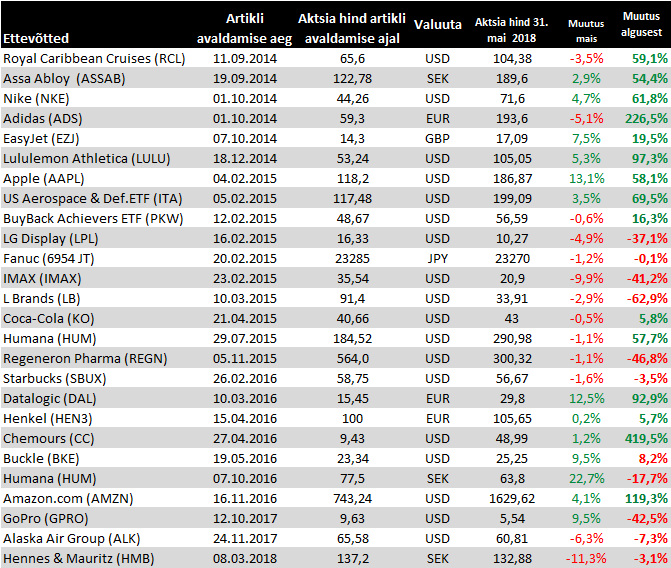

Muutused 31. mai seisuga

H&Mi juhi ja peamise aktsionäri aktsiaostud on hiljaaegu viinud taas spekulatsioonideni, et Perssonil on huvi ettevõte börsilt ära viia, kuid see ei pea tema sõnul paika

H&M Chairman Stefan Persson says speculation that he would take company private has "no bearing" at all, Breakit reports, citing Persson.

H&M Chairman Stefan Persson says speculation that he would take company private has "no bearing" at all, Breakit reports, citing Persson.

H&M raporteeris teise kvartali müügi, mis jäi ootusele alla. Poolaasta aruanne avaldatakse 28. juunil, kuid pigem süvendab number kahtlust, et juhtkonna prognoositud ärikasumi tänavust paranemist saab olema keeruline saavutada.

* 2Q sales SEK51.98 billion, estimate SEK52.55 billion (range SEK51.48 billion to SEK53.40 billion) (Bloomberg data)

* 2Q sales incl. VAT was up 2% y/y to SEK60.5b

* On a constant currency basis total sales came in flat year on year (vs consensus of +0.5%).

* 2Q sales SEK51.98 billion, estimate SEK52.55 billion (range SEK51.48 billion to SEK53.40 billion) (Bloomberg data)

* 2Q sales incl. VAT was up 2% y/y to SEK60.5b

* On a constant currency basis total sales came in flat year on year (vs consensus of +0.5%).

Starbucks tõdes eile kasvu aeglustumist ja kuigi uue tegevjuhi sõnul pakuvad nii USA kui ka Hiina turg jätkuvalt suurt kasvupotentsiaali, siis tõenäoliselt jäävad investorid ettevõtte ümberpööramiseks võetavate abimeeteme suhtes skeptiliseks, kuniks pole ette näidata tulemuste paranemist

STARBUCKS SEES 3Q GLOBAL SAME-STORE SALES UP 1%, EST. UP 2.9%

SBUX SEES FY18 ADJ EPS $2.39-$2.43, SAW $2.48-$2.53, EST. $2.49

STARBUCKS SEES 3Q GLOBAL SAME-STORE SALES UP 1%, EST. UP 2.9%

SBUX SEES FY18 ADJ EPS $2.39-$2.43, SAW $2.48-$2.53, EST. $2.49

H&M raporteeris teise kvartali täpsemad tulemused, kust on näha, et arvatust veidi suuremad kulud jätsid maksueelse kasumi prognoositust väiksemaks. Ja kuigi ettevõte on teise poolaasta osas optimislikum, siis kõrged varud on endiselt kasvamas

*Sees FY net addition of stores 240, saw about 220.0

* 2Q pretax profit SEK6.01 billion, estimate SEK6.28 billion (range SEK5.69 billion to SEK6.96 billion) (Bloomberg data)

* 2Q gross margin +56.1%, estimate +55.8% (BD)

* 2Q net income SEK4.64 billion, estimate SEK4.79 billion (range SEK4.53 billion to SEK5.36 billion) (BD)

* 2Q stock-in-trade as share of sales excluding VAT 18.2% vs. 17.6% q/q

* As Signaled Previously, It Was Going to Be Tough 1H

* Closing Inventory Level Is Still Too High

* Went Into 2Q Carrying Too Much Stock

* Increased Markdowns in Relation to Sales in 3Q vs 3Q 2017

* Total Sales for Quarter Were Not Satisfactory

*Sees FY net addition of stores 240, saw about 220.0

* 2Q pretax profit SEK6.01 billion, estimate SEK6.28 billion (range SEK5.69 billion to SEK6.96 billion) (Bloomberg data)

* 2Q gross margin +56.1%, estimate +55.8% (BD)

* 2Q net income SEK4.64 billion, estimate SEK4.79 billion (range SEK4.53 billion to SEK5.36 billion) (BD)

* 2Q stock-in-trade as share of sales excluding VAT 18.2% vs. 17.6% q/q

* As Signaled Previously, It Was Going to Be Tough 1H

* Closing Inventory Level Is Still Too High

* Went Into 2Q Carrying Too Much Stock

* Increased Markdowns in Relation to Sales in 3Q vs 3Q 2017

* Total Sales for Quarter Were Not Satisfactory

Pressikonverentsil tõdes H&Mi juht, et ärikasumi parandamise lubaduse täitmine on muutunud raskemaks pärast oodatust kesisemat esimest poolaastat

H&M CEO Karl-Johan Persson says it has become "tougher" to reach the company’s goal of an improved operating profit in 2018 vs 2017 after the 1H of this year was more challenging than the company had expected.

* "But there is still six months to go, so we’ll see," CEO says

* Sees "gradual improvement" in 2H and says 2H 2018 will be stronger than both 1H 2018 and 2H 2017

* H&M still aims grow sales for online and new business by more than 25% during the year

H&M CEO Karl-Johan Persson says it has become "tougher" to reach the company’s goal of an improved operating profit in 2018 vs 2017 after the 1H of this year was more challenging than the company had expected.

* "But there is still six months to go, so we’ll see," CEO says

* Sees "gradual improvement" in 2H and says 2H 2018 will be stronger than both 1H 2018 and 2H 2017

* H&M still aims grow sales for online and new business by more than 25% during the year

Veel üks nope H&Mi konverenstikõnelt, kus tegevjuhi arvates ei ole nad olukorras, kus kõrgeid varusid peaks hakkama maha kandma

*H&M CEO Karl-Johan Persson says that while the company could write down inventory, "it believes there is a big value in the products we have, in that excess inventory."

* "We think the best way to handle this is through the summer sale, and then we’ll see where we are after that," CEO says at press conference in Stockholm after 2Q earnings

* Expects inventory to be in better shape after the summer and autumn

*H&M CEO Karl-Johan Persson says that while the company could write down inventory, "it believes there is a big value in the products we have, in that excess inventory."

* "We think the best way to handle this is through the summer sale, and then we’ll see where we are after that," CEO says at press conference in Stockholm after 2Q earnings

* Expects inventory to be in better shape after the summer and autumn