Assa Abloylt oodatust paremad tulemused ja kuigi Hiinas on nõudlus endiselt nõrgapoolne, siis languse asemel on müük stabiliseerunud. Kvartali jooksul alustati koostööd Amazoni, Walmarti ja Google'ga ning tegevjuhi sõnul on nutilukkude näol avanemas nende jaoks suur turg.

*Assa Abloy reported Ebit for the fourth quarter that was 1.2% above the average analyst estimate.

* 4Q Ebit SEK3.36 billion, estimate SEK3.32 billion (range SEK3.28 billion to SEK3.38 billion) (Bloomberg data)

* 4Q sales SEK20.11 billion, estimate SEK19.82 billion (range SEK19.44 billion to SEK20.12 billion) (BD)

* 4Q organic revenue +5%

* FY dividend per share SEK3.30, estimate SEK3.23 (range SEK3 to SEK3.50) (BD)

* Positive Trend on Most Mkts, Especially in Europe

* Demand Still Weak on Some Mkts Such as China, Brazil

Mõned nopped Assa pressikonverentsilt:

* Assa Abloy had an organic growth outlook of 2-4% for 2017 a year ago, and the outlook for 2018 is better than that, CEO Johan Molin says on conference call after 4Q earnings.

* Says January started well; 1H “certainly looks good”

* Says smart-lock sales currently about SEK2b, or 11-13% of residential sales

* If majority of private residences are converted to smart-door locks during the next decade, it will be “a major boost to turnover” for Assa Abloy

* On Amazon Key, “we haven’t seen much action yet” due to startup issues

* Assa Abloy had an organic growth outlook of 2-4% for 2017 a year ago, and the outlook for 2018 is better than that, CEO Johan Molin says on conference call after 4Q earnings.

* Says January started well; 1H “certainly looks good”

* Says smart-lock sales currently about SEK2b, or 11-13% of residential sales

* If majority of private residences are converted to smart-door locks during the next decade, it will be “a major boost to turnover” for Assa Abloy

* On Amazon Key, “we haven’t seen much action yet” due to startup issues

Humanalt ootuspärase käibe juures arvatust parem neljanda kvartali kasum. Väljavaade müügitulule jääb konsensuse prognoosile alla aga kasumiprognoos on positiivsem

Reports Q4 (Dec) earnings of $2.06 per share, excluding non-recurring items, $0.06 better than the Capital IQ Consensus of $2.00; revenues rose 2.4% year/year to $13.19 bln vs the $13.14 bln Capital IQ Consensus.

Co issues mixed guidance for FY18, sees EPS of $13.50-14.00, excluding non-recurring items, vs. $12.45 Capital IQ Consensus Estimate; sees FY18 revs of $55.8-56.4 bln vs. $56.57 bln Capital IQ Consensus Estimate.

Reports Q4 (Dec) earnings of $2.06 per share, excluding non-recurring items, $0.06 better than the Capital IQ Consensus of $2.00; revenues rose 2.4% year/year to $13.19 bln vs the $13.14 bln Capital IQ Consensus.

Co issues mixed guidance for FY18, sees EPS of $13.50-14.00, excluding non-recurring items, vs. $12.45 Capital IQ Consensus Estimate; sees FY18 revs of $55.8-56.4 bln vs. $56.57 bln Capital IQ Consensus Estimate.

L Brandsi müük sujus jaanuaris arvatust paremini, ühtlasi teatatakse, et rohkem kuist statistikat ei avaldata

L Brands reports January comps of +7% vs +LSD guidance and Consensus Est. Up 1.8%; sees Q4 EPS of $2.05 vs ~$2.00 prior guidance and $2.01; consensus on prelim Q4 sales of $4.823 bln vs $4.72 bln Capital IQ Consensus

Samuti läks arvatust paremini Buckle'i poodidel

Buckle Jan. Comp Sales up 0.2% vs. Est. Down 3.2%; prelim Q4 sales of $281.2 mln vs $280 mln Capital IQ Consensus

L Brands reports January comps of +7% vs +LSD guidance and Consensus Est. Up 1.8%; sees Q4 EPS of $2.05 vs ~$2.00 prior guidance and $2.01; consensus on prelim Q4 sales of $4.823 bln vs $4.72 bln Capital IQ Consensus

Samuti läks arvatust paremini Buckle'i poodidel

Buckle Jan. Comp Sales up 0.2% vs. Est. Down 3.2%; prelim Q4 sales of $281.2 mln vs $280 mln Capital IQ Consensus

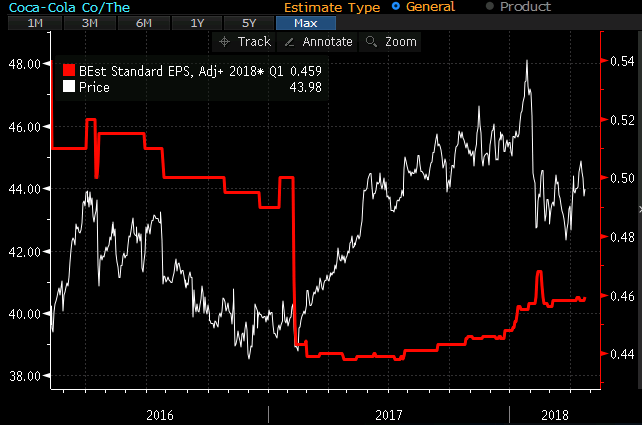

Coca-Colalt oodatust paremad numbrid ning parem prognoos

Reports Q4 (Dec) earnings of $0.39 per share, $0.01 better than the Capital IQ Consensus of $0.38; revenues fell 20.3% year/year to $7.5 bln vs the $7.36 bln Capital IQ Consensus. Organic revenues (non-GAAP) grew 6% for the quarter, driven by price/mix growth of 4% and concentrate sales growth of 1%.

Co issues upside guidance for FY18, sees EPS +8-10% to ~$2.06-2.10 vs. $1.99 Capital IQ Consensus; ~4% growth in organic revenues (non-GAAP), 8% to 9% growth in comparable currency neutral operating income (structurally adjusted).

Reports Q4 (Dec) earnings of $0.39 per share, $0.01 better than the Capital IQ Consensus of $0.38; revenues fell 20.3% year/year to $7.5 bln vs the $7.36 bln Capital IQ Consensus. Organic revenues (non-GAAP) grew 6% for the quarter, driven by price/mix growth of 4% and concentrate sales growth of 1%.

Co issues upside guidance for FY18, sees EPS +8-10% to ~$2.06-2.10 vs. $1.99 Capital IQ Consensus; ~4% growth in organic revenues (non-GAAP), 8% to 9% growth in comparable currency neutral operating income (structurally adjusted).

L Brandsi jaanuari oodatust parem müük polnud paraku signaaliks äritegevuse edasise paranemise kohta

L Brands reports Q4 (Jan) earnings of $2.11 per share, excluding non-recurring items, $0.06 better than the Capital IQ Consensus of $2.05; revenues rose 7.4% year/year to $4.82 bln vs the $4.72 bln Capital IQ Consensus.

Comps +2%; VS -1% and B&BW +6%

Co issues downside guidance for Q1, sees EPS of $0.15-0.20 vs. $0.31 Capital IQ Consensus Estimate.

Co issues downside guidance for FY19, sees EPS of $2.95-3.25 vs. $3.43 Capital IQ Consensus Estimate.

L Brands reports Q4 (Jan) earnings of $2.11 per share, excluding non-recurring items, $0.06 better than the Capital IQ Consensus of $2.05; revenues rose 7.4% year/year to $4.82 bln vs the $4.72 bln Capital IQ Consensus.

Comps +2%; VS -1% and B&BW +6%

Co issues downside guidance for Q1, sees EPS of $0.15-0.20 vs. $0.31 Capital IQ Consensus Estimate.

Co issues downside guidance for FY19, sees EPS of $2.95-3.25 vs. $3.43 Capital IQ Consensus Estimate.

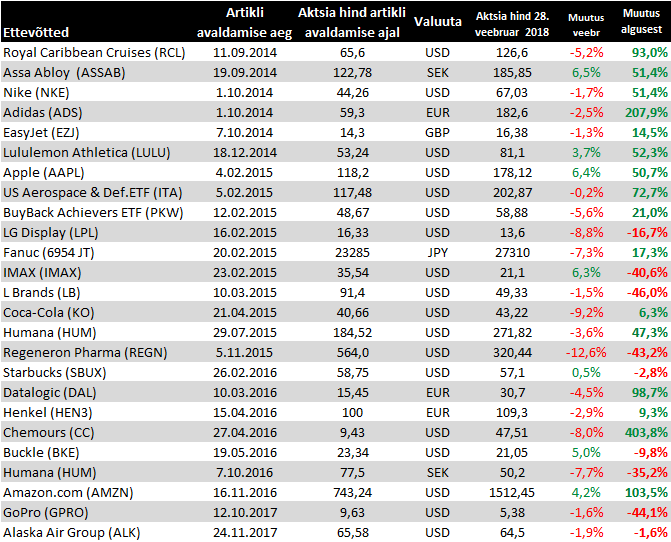

28. veebruari seisuga

Lisan nimekirja H&Mi. Saab olema huvitav näha, kuidas suudetakse tihenenud konkurentsitingimustes emalaeva ümber pöörata.

H&Mi aktsionärid tormavad väljapääsu suunas

H&Mi aktsionärid tormavad väljapääsu suunas

H&M on esimeses kvartalis teinud kõva müügikampaaniat, et varudest lahti saada aga ikka on müük jäämas alla ootuste

* 1Q sales SEK46.18 billion, estimate SEK46.95 billion (range SEK45.94 billion to SEK47.71 billion) (Bloomberg data)

* Says 1Q sales excluding VAT SEK46.2b vs SEK47.0b y/y

* 1Q sales SEK46.18 billion, estimate SEK46.95 billion (range SEK45.94 billion to SEK47.71 billion) (Bloomberg data)

* Says 1Q sales excluding VAT SEK46.2b vs SEK47.0b y/y

Q4 käibenumbri raporteeris Buckle juba veebruari alguses, kuid üllatada suutis USA rõivaste jaemüüja kasumiga

Buckle reports Q4 (Jan) earnings of $0.87 per share, excluding non-recurring items, $0.15 better than the Capital IQ Consensus of $0.72; revenues rose 0.4% year/year to $281.2 mln vs the $280.04 mln Capital IQ Consensus

Buckle reports Q4 (Jan) earnings of $0.87 per share, excluding non-recurring items, $0.15 better than the Capital IQ Consensus of $0.72; revenues rose 0.4% year/year to $281.2 mln vs the $280.04 mln Capital IQ Consensus

Nike on viimaks nägemas pööret paremuse suunas oma Põhja-Ameerika äris

NIKE Reports Q3 (Feb) earnings of $0.68 per share, excluding non-recurring items, $0.15 better than the Capital IQ Consensus of $0.53; revenues rose 6.5% year/year to $8.98 bln vs the $8.85 bln Capital IQ Consensus.

By region: NA sales (ex-FX) -6%, EMEA +9%, China +19%, APac,LA +11%

"As we close Q3, we now see a significant reversal of trend in North America, as momentum accelerates through the scaling of new innovation platforms and differentiated NIKE Consumer Experiences expand across the marketplace."

Nike North America revenue is projected to be roughly flat to prior-year in Q4 and return to growth in the first half of fiscal year 2019.

Expects Q4 reported revenue to grow in the high single-digit range (Capital IQ consensus of +7.8%).

Expects fiscal year 2019 reported revenue growth in the mid to high single-digit range (Cap IQ consensus of + 6.9%).

NIKE Reports Q3 (Feb) earnings of $0.68 per share, excluding non-recurring items, $0.15 better than the Capital IQ Consensus of $0.53; revenues rose 6.5% year/year to $8.98 bln vs the $8.85 bln Capital IQ Consensus.

By region: NA sales (ex-FX) -6%, EMEA +9%, China +19%, APac,LA +11%

"As we close Q3, we now see a significant reversal of trend in North America, as momentum accelerates through the scaling of new innovation platforms and differentiated NIKE Consumer Experiences expand across the marketplace."

Nike North America revenue is projected to be roughly flat to prior-year in Q4 and return to growth in the first half of fiscal year 2019.

Expects Q4 reported revenue to grow in the high single-digit range (Capital IQ consensus of +7.8%).

Expects fiscal year 2019 reported revenue growth in the mid to high single-digit range (Cap IQ consensus of + 6.9%).

Kui H&M esimese kvartali müügitulu oli juba varem teada, siis täna avaldatud täpsemad detailid näitavad, et väga heitlike ilmade tõttu tuli teha arvatust veelgi suuremaid allahindlusi, mis jättis maksueelse kasumi ootustele alla ning varude ja müügitulu suhe kvartaliga hoopis halvenes.

* 1Q gross margin +49.9%, estimate +50.1% (Bloomberg data)

* 1Q net income SEK1.37 billion, estimate SEK1.12 billion (range SEK664.0 million to SEK1.85 billion) (BD)

* 1Q pretax profit SEK1.26 billion, estimate SEK1.44 billion (range SEK862.0 million to SEK2.37 billion) (BD)

* 1Q stock-in-trade as share of sales excluding VAT 17.6% vs. 16.9% q/q

* Still sees FY net addition of stores about 220

* 1Q gross margin +49.9%, estimate +50.1% (Bloomberg data)

* 1Q net income SEK1.37 billion, estimate SEK1.12 billion (range SEK664.0 million to SEK1.85 billion) (BD)

* 1Q pretax profit SEK1.26 billion, estimate SEK1.44 billion (range SEK862.0 million to SEK2.37 billion) (BD)

* 1Q stock-in-trade as share of sales excluding VAT 17.6% vs. 16.9% q/q

* Still sees FY net addition of stores about 220

Chemours prognoosib 2018.a aktsiakasumit varasema ootuse vahemiku ülemises ääres

Chemours sees year adjusted EPS to be at high end of its February 14 view of $4.95 to $5.60, estimate $5.41 (9 estimates)

* Sees year adjusted Ebitda at high end of previously communicated $1.7 billion to $1.85 billion range

* Company to release first-quarter results after market close on May 3; may update its long-term targets on earnings call

Chemours sees year adjusted EPS to be at high end of its February 14 view of $4.95 to $5.60, estimate $5.41 (9 estimates)

* Sees year adjusted Ebitda at high end of previously communicated $1.7 billion to $1.85 billion range

* Company to release first-quarter results after market close on May 3; may update its long-term targets on earnings call

Lululemon raporteeris oodatust paremad neljanda kvartali tulemused ning positiivne väljavaade alanud majandusaastale näitab, et veebruaris ootamatult ametist tagasi astunud tegevjuhile uue asemiku otsimine pole pärssimas firma kasvu

Lululemon reports Q4 (Jan) earnings of $1.33 per share, excluding non-recurring items, $0.06 better than the Capital IQ Consensus of $1.27; revenues rose 17.6% year/year to $929 mln vs the $912.41 mln Capital IQ Consensus.

Total comparable sales increased 12%, or increased 11% on a constant dollar basis vs. high single digit guidance. Comparable store sales increased 2%, or increased 1% on a constant dollar basis. Direct to consumer net revenue increased 44%, or increased 42% on a constant dollar basis.

Adjusted gross margin was 56.2%, an increase of 200 basis points.

Co issues upside guidance for Q1, sees EPS of $0.44-0.46 vs. $0.40 Capital IQ Consensus Estimate; sees Q1 revs of $612-617 mln vs. $585.52 mln Capital IQ Consensus Estimate; low double digit comps ex-FX

Co issues guidance for FY19, sees EPS of $3.00-3.08 vs. $3.03 Capital IQ Consensus Estimate; sees FY19 revs of $2.985-3.022 bln vs. $2.95 bln Capital IQ Consensus Estimate; mid to high single digit comps ex-FX.

Lululemon reports Q4 (Jan) earnings of $1.33 per share, excluding non-recurring items, $0.06 better than the Capital IQ Consensus of $1.27; revenues rose 17.6% year/year to $929 mln vs the $912.41 mln Capital IQ Consensus.

Total comparable sales increased 12%, or increased 11% on a constant dollar basis vs. high single digit guidance. Comparable store sales increased 2%, or increased 1% on a constant dollar basis. Direct to consumer net revenue increased 44%, or increased 42% on a constant dollar basis.

Adjusted gross margin was 56.2%, an increase of 200 basis points.

Co issues upside guidance for Q1, sees EPS of $0.44-0.46 vs. $0.40 Capital IQ Consensus Estimate; sees Q1 revs of $612-617 mln vs. $585.52 mln Capital IQ Consensus Estimate; low double digit comps ex-FX

Co issues guidance for FY19, sees EPS of $3.00-3.08 vs. $3.03 Capital IQ Consensus Estimate; sees FY19 revs of $2.985-3.022 bln vs. $2.95 bln Capital IQ Consensus Estimate; mid to high single digit comps ex-FX.

Aetna plaan võtta üle USA ravikindlustusfirma jooksis eelmise aasta alguses liiva, nüüd aga on väidetavalt ostuhuvi Humana vastu näidanud Walmart.

Walmart in Early-Stage Acquisition Talks With Humana

Walmart in Early-Stage Acquisition Talks With Humana

Coca-Colalt oodatust parema käibe pealt pisut parem aktsiakasum ning 2018.a prognoos jäetakse samaks.

Coca-Cola reports Q1 (Mar) earnings of $0.47 per share, excluding non-recurring items, $0.01 better than the Capital IQ Consensus of $0.46; revenues fell 16.6% year/year to $7.6 bln vs the $7.32 bln Capital IQ Consensus (Organic revenues (non-GAAP) grew 5% for the quarter)

Co reaffirms guidance for FY18, sees EPS of +8-10% to ~$2.06-2.10 vs. $2.10 Capital IQ Consensus Estimate. Co sees approximately 4% growth in organic revenues (non-GAAP) -- No Change;

Coca-Cola reports Q1 (Mar) earnings of $0.47 per share, excluding non-recurring items, $0.01 better than the Capital IQ Consensus of $0.46; revenues fell 16.6% year/year to $7.6 bln vs the $7.32 bln Capital IQ Consensus (Organic revenues (non-GAAP) grew 5% for the quarter)

Co reaffirms guidance for FY18, sees EPS of +8-10% to ~$2.06-2.10 vs. $2.10 Capital IQ Consensus Estimate. Co sees approximately 4% growth in organic revenues (non-GAAP) -- No Change;

Assa Abloy üllatas vaatamata väiksemale päevade arvule arvatust tugevama müügi kasvuga, kuid marginaal valmistas kerge pettumuse

* 1Q sales SEK18.55 billion, estimate SEK18.52 billion (range SEK18.14 billion to SEK19.09 billion)

* 1Q Ebit SEK2.83 billion, estimate SEK2.88 billion (range SEK2.80 billion to SEK2.96 billion)

* 1Q organic revenue +4% Says year took off with good organic growth despite the negative calendar effect of two trading days less due to an early Easter

* Says achieved strong or good growth in all divisions

* Operating cash flow was seasonally low totaling SEK 575 Mln for the quarter

* Continues to focus on cost-efficiency and to deliver on current restructuring program and still expects to announce a new program by the end of 2018

* 1Q sales SEK18.55 billion, estimate SEK18.52 billion (range SEK18.14 billion to SEK19.09 billion)

* 1Q Ebit SEK2.83 billion, estimate SEK2.88 billion (range SEK2.80 billion to SEK2.96 billion)

* 1Q organic revenue +4% Says year took off with good organic growth despite the negative calendar effect of two trading days less due to an early Easter

* Says achieved strong or good growth in all divisions

* Operating cash flow was seasonally low totaling SEK 575 Mln for the quarter

* Continues to focus on cost-efficiency and to deliver on current restructuring program and still expects to announce a new program by the end of 2018

Jaapani tööstusrobotite tootja Fanuc raporteeris laias laastus ootuspärased neljanda kvartali tulemused aga üllatas prognoosiga, mis näeb uuel fiskaalaastal ette -34% ärikasumi langust. Ettevõtte sõnul toetas 2018 tulemusi ühekordne IT nõudluse hüpe, mille kahanemine peaks jätma jälje firma 2019 tulemustesse

4Q net sales 190.60 billion yen, estimate 187.80 billion yen (range 180 billion yen to 195 billion yen)

4Q operating income 60.37 billion yen, estimate 62.53 billion yen (range 57.80 billion yen to 65.77 billion yen)

Sees FY net sales 634.2 billion yen, estimate 766 billion yen (range 681 billion yen to 815 billion yen)

Sees FY operating income 151.7 billion yen, estimate 250.21 billion yen

4Q net sales 190.60 billion yen, estimate 187.80 billion yen (range 180 billion yen to 195 billion yen)

4Q operating income 60.37 billion yen, estimate 62.53 billion yen (range 57.80 billion yen to 65.77 billion yen)

Sees FY net sales 634.2 billion yen, estimate 766 billion yen (range 681 billion yen to 815 billion yen)

Sees FY operating income 151.7 billion yen, estimate 250.21 billion yen