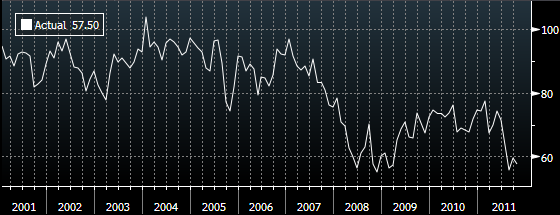

October Michigan Sentiment 57.5 vs 60.0 Briefing.com consensus; September 59.4

Sentiment on nõrk olnud juba mitmeid kuid - vähemalt nii kurdetakse küsitlejatele. Ja siis panevad nad telefoni ära ja lähevad autosid ostma nagu juhtus Septembris. Seega jälgige pigem, mida inimesed teevad mitte räägivad.

Erko Rebane

October Michigan Sentiment 57.5 vs 60.0 Briefing.com consensus; September 59.4

jaemüük üles, tarbijausaldus alla, see siis tähendab, et osteti petrooleumi, soola, tikke ja konserve? :)

Mis puudutab automüüki, siis Zerohedge vahendab huvitavat GSi analüüsi...

Based on the composition of sales, the main factor appears to be business investment spending. Vehicle sales are often thought of as an indicator of consumer demand, but companies account for about half of the dollar value of new purchases. Since vehicle sales bottomed, firms have accounted for about 70% of the growth in purchases. The outlook for business vehicle purchases arguably remains bright, mostly due to pent-up demand.

Based on the composition of sales, the main factor appears to be business investment spending. Vehicle sales are often thought of as an indicator of consumer demand, but companies account for about half of the dollar value of new purchases. Since vehicle sales bottomed, firms have accounted for about 70% of the growth in purchases. The outlook for business vehicle purchases arguably remains bright, mostly due to pent-up demand.

The Guardiani David Gow kirjutab blogis EFSFi teemal:

Brussels is bathed in autumnal sunshine, EU officials are sitting, tie-less if male, in parks - and the action has moved with the Thalys to Paris, just an hour and 20 minutes away, and the G20. Even so, we're now getting a bit more visibility here on how policy-makers plan to turn the euro zone rescue fund, the EFSF, into a "bazooka." The best way to "optimise its resources", it appears, is to forget about it being a bank but, rather, treat it as an insurer. That means guaranteeing the first, say, 20% of private sector losses on Spanish and Italian bonds, perhaps 30% on those of more peripheral, weaker countries. That way, you don't have to upset the ECB and its new Italian president-in-waiting, Mario Draghi, by pressing it to buy even more government bonds. The aim, above all, is to avoid anything that smacks of the CDOs that got the entire world into trouble in 2007.

The insurer idea has the merit of being acceptable to Berlin and not entirely anathema to Paris which had favoured the EFSF as a bank. Christophe Frankel, the fund's CFO and deputy chief executive, told reporters here today "any decision to use the EFSF's capacity more efficiently will not lead to an increase in guarantees from the member states" and, therefore, no impact on its own Triple A rating. Those guarantees of €780bn allow effective credit lending of €480bn but the insurer role could triple or quadruple its firepower.

It's another of the ideas being kicked around in EU capitals but one gaining substantial traction. As is the notion - being discussed by G20 finance ministers in Paris - of an IMF "stability" bond that would be backed by, inter alia, China and other BRICs. This apparently landed on Brussels desks a few days ago. But sometime next week we should get the definitive blueprint for the "comprehensive, cohesive" plan from Merkel and Sarkozy in time for the five top-level meetings, including two summits, taking place between Friday night and Sunday evening.

Jaapan valmistub järgmisest nädalast võtma uusi samme jeeni nõrgestamiseks. Korralik spike kõikides jeeni paarides.

Japanese government official says steps won't include forex tax.

Japanese government official says steps likely to include boosting of fund to encourage overseas M&A activity.

Japanese government official says steps likely to be finalised next week for inclusion in extra budget.

Täna suur müügisurve erinevatel kiipide tarnijatel, mingi põhjus ka teada?

Äkki prognooside kärpimine Infineoni poolt? Bloombergi lugu

Mõned MSi kommentaarid Infineoni kohta:

A very surprising profit warning: as, even if we were negative on Infineon since June, we thought that margins would remain resilient until the end of the year. We would stay away from Ifx until the shares stabilise

close to €5 and 2012 EPS closer to €0.40-0.45 (our bear case EPS).

For FYQ4, revenues are in line with expectations at €1,040m vs MSe €1,047 and consensus €1,044m. EBIT came below though at €195m (18.8%) vs. consensus €210m (20.1%). Even our forecasts were calling for EBIT margins of 20% as management had remained adamant during all the quarter that margins would remain at 20%.

Pricing pressure. We believe Infineon has seen some price pressure and negative mix, combined with the end of the services contract with Intel. The latter is not a real issue for us, but cyclical pressure on pricing should be a concern for investors as it will increase the downward pressure on margins we are already expecting for 2012 (we currently forecast 17% in our base case but that could prove too optimistic). For FYQ1, Infineon is guiding for mid teens EBIT margins due to weakness in Industrial and Multi Markets as well as Chipcards. So far, Automotive has remained resilient, but any weakness there could push margins further down.

We expect consensus EPS estimates to decline significantly on the back of the profit warning, probably toward our bear case scenario of €0.43. We would continue to avoid the shares unless they are close to €5.

A very surprising profit warning: as, even if we were negative on Infineon since June, we thought that margins would remain resilient until the end of the year. We would stay away from Ifx until the shares stabilise

close to €5 and 2012 EPS closer to €0.40-0.45 (our bear case EPS).

For FYQ4, revenues are in line with expectations at €1,040m vs MSe €1,047 and consensus €1,044m. EBIT came below though at €195m (18.8%) vs. consensus €210m (20.1%). Even our forecasts were calling for EBIT margins of 20% as management had remained adamant during all the quarter that margins would remain at 20%.

Pricing pressure. We believe Infineon has seen some price pressure and negative mix, combined with the end of the services contract with Intel. The latter is not a real issue for us, but cyclical pressure on pricing should be a concern for investors as it will increase the downward pressure on margins we are already expecting for 2012 (we currently forecast 17% in our base case but that could prove too optimistic). For FYQ1, Infineon is guiding for mid teens EBIT margins due to weakness in Industrial and Multi Markets as well as Chipcards. So far, Automotive has remained resilient, but any weakness there could push margins further down.

We expect consensus EPS estimates to decline significantly on the back of the profit warning, probably toward our bear case scenario of €0.43. We would continue to avoid the shares unless they are close to €5.

Septembrikuu jaemüük ületas Morgan Stanley ootusi ning eeldatavalt tähendab see nende poolt Q3 SKT kasvu tõstmist 3,1% pealt 3,3% peale.

The upside surprise took our assessment of Q3 consumer spending up by 0.5 percentage points (from +1.6% to +2.1%). This pushes our tracking estimate of Q3 GDP from +3.1% to +3.3% (note: we tried to be conservative by offsetting some of the consumption strength with lower inventories and will revisit all this after the 10am inventory data). Also, we now have a much better ramp for consumer spending heading into Q4.

The upside surprise took our assessment of Q3 consumer spending up by 0.5 percentage points (from +1.6% to +2.1%). This pushes our tracking estimate of Q3 GDP from +3.1% to +3.3% (note: we tried to be conservative by offsetting some of the consumption strength with lower inventories and will revisit all this after the 10am inventory data). Also, we now have a much better ramp for consumer spending heading into Q4.

Google confirmed on its blog that it plans to shut down Google Buzz and the Buzz API; will focus instead on Google+

Alustanud siis Orkuti rahva sundüleviimisega plussi :)

September Treasury Budget -$64.6 bln vs -$67.0 bln Briefing.com consensus

ALARIÜ midagi eesti keeles ka komenteerida võiks? Midagi pahasti ei taha öelda.

Ega nii väikesed veel ei tohikski rumalaid sõnu kasutada.

Ei saa seesugune tõus ju olla jätkusuutlik...

Tõusu kohta vara veel rääkida. See, et langus polnud jätkusuutlik, on nüüd siililegi selge.

Me räägime erinevatest asjadest, Sina mullist, mina tõusust!

hoks

Ei saa seesugune tõus ju olla jätkusuutlik...

3 argumenti ka selle arvamuse toetuseks?

Volatiilsuse kiire langus on tõepoolest märkimisväärne ja langemine alla 30 on varasemalt suhteliselt täpselt märkinud turgude languse lõppu, mõnikord on peale esimest alla 30 langemist küll esinenud veel üks terav lühiajaline põrge volatiilsuses,

The CBOE Volatility Index, or VIX(Chicago Options:^VIX - News), fell 8 percent to end at 28.24, and closed lower for the ninth day in a row, a pattern suggesting more gains could be in store as investors find less need for protection against losses.

"This has only happened four other times in the last 15 years and each time following this decline, the market over the next two months went up or stayed flat," wrote Jay Pestrichelli, co-founder and principal of Zega Financial LLC, an investment advisory firm specializing in option strategies

The CBOE Volatility Index, or VIX(Chicago Options:^VIX - News), fell 8 percent to end at 28.24, and closed lower for the ninth day in a row, a pattern suggesting more gains could be in store as investors find less need for protection against losses.

"This has only happened four other times in the last 15 years and each time following this decline, the market over the next two months went up or stayed flat," wrote Jay Pestrichelli, co-founder and principal of Zega Financial LLC, an investment advisory firm specializing in option strategies