Nikkei225: -14% praegu. Meenub juba oktoobrit 1987.

Huvitav on siinjuures USD/JPY stabiilsus. Kui Jaapan oli varem JPY sularaha täis, siis nüüd ilmselt aina enam niimoodi. Samas ikka pakub see sularaha kindlust, aga sealgi võib kuskil olla "tipping point".

Arvaksin, et varsti oleks pigem Nikkei võimsas tõusus, ja JPY korralikus languses.

Arvaksin, et varsti oleks pigem Nikkei võimsas tõusus, ja JPY korralikus languses.

Viimase tunni jooksul Nikkei +4%.

oops juba +6% viie veerandtunni jooksul.

Paradoksaalsel kombel võib see katastroof anda Jaapani majandusele peale esimest tagasilööki korraliku boosti hoopiski.

Mis seis praegu on nendel turgudel.

Nikkei225 sulgus -10,55% peal

Tänud! Eestis siis ka oodata langust.

USD/JPY 79,40 praegu.

Suhtarv (Jaapani erasektori omanduses JPY raha maht/Jaapanlaste aastane palgasumma) tõuseb kiiresti ja töötamine et eksportida muutub aina mõttetumaks.

=> mis minu arust peaks lõppema JPY krahhiga ja hyperinflatsiooniga Jaapanis, ehk maavärin finantsturul.

Lähikuudel võiks oodata suurenevat importi ja vähenevat eksporti, mis peaks tekitama JPY nõrgendamist. Seda mis praegu näeme on ilmselt välismaa finantsinvesteeringute repatrieerimist, aga minu meelest peaks aegamööda tulema 180 kraadine pööre JPY arenduses. Elame-näeme.

Nüüd täielik paanika USD/JPY 77,50.

Tagasilöök ülespoole tuleb võimas, ma pakun.

Tagasilöök ülespoole tuleb võimas, ma pakun.

2% JPY tugevnemine 10 minutiga vms.

77,34

(kirjutan ajalooraamatutele)

(kirjutan ajalooraamatutele)

BOJ võiks nüüd sisse astuda helikopteritega ja tekitada inflatsiooni, vastasel juhul siis täielik eksporditöötuse krahh ja lõpuks ikkagi inflatsioon - ma arvan.

77,09

põhi oli vist 76,18 CNBC järgi.

Nüüd põrge ja 78,07

Nüüd põrge ja 78,07

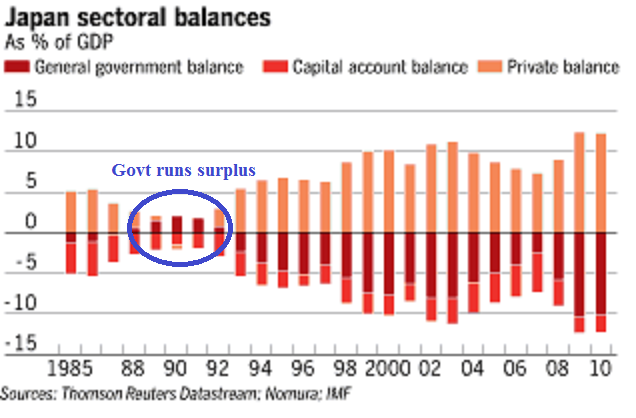

Japan’s policies over the years have been terribly misguided. Much like our own policies are currently misguided. In the late 80′s Japan experienced dual bubbles in real estate and equities on the back of a stellar period of growth. They had deregulated their banking system, allowed their economy to become financialized and to top it off their government decided it was wise to take advantage of this period of stellar economic growth by running a budget surplus to “get their financial house in order”. In essence, this was almost exactly what the United States did in the years running up to our own dual bubbles.

Like the budget surplus in the USA in 1999 the surplus in Japan exacerbated the private sector debt problem as the public sector surplus resulted in private sector deficit. This ultimately resulted in en epic bubble collapse. Their solution was less than precise. Rather than take the Swedish approach the Japanese decided to let their banks earn their way out of the crisis. This only prolonged the inevitable deleveraging. This was combined with insufficient budget deficits that would have allowed the private sector to deleverage more quickly. This debt deleveraging resulted in anemic economic growth and persistent deflation. What ensued was a series of start and stop recessions and recoveries that happened to overlap with a difficult period of economic growth in many other parts of the world. As we all know it hasn’t been a pretty picture.

Like the budget surplus in the USA in 1999 the surplus in Japan exacerbated the private sector debt problem as the public sector surplus resulted in private sector deficit. This ultimately resulted in en epic bubble collapse. Their solution was less than precise. Rather than take the Swedish approach the Japanese decided to let their banks earn their way out of the crisis. This only prolonged the inevitable deleveraging. This was combined with insufficient budget deficits that would have allowed the private sector to deleverage more quickly. This debt deleveraging resulted in anemic economic growth and persistent deflation. What ensued was a series of start and stop recessions and recoveries that happened to overlap with a difficult period of economic growth in many other parts of the world. As we all know it hasn’t been a pretty picture.