Shotspotter jäi ootustele alla ning kärpis prognoosi, tuues põhjuseks ühe kliendi kaotamise ja läbirääkimiste venimise kahe uue kliendiga.

Reports Q1 (Mar) GAAP loss of $0.03 per share, $0.01 worse than the S&P Capital IQ GAAP Consensus of ($0.02); revenues rose 38.8% year/year to $9.59 mln vs the $9.77 mln S&P Capital IQ Consensus.

"From an operational standpoint, we added 12 net new ‘go-live' square miles of coverage in Q1, bringing our total live miles to 660. While our go-live miles can vary quarter-to-quarter, we expect our quarterly go-live miles to increase in Q2 and the balance of the year. In fact, we expect to turn on approximately 50 new miles in the next 90+ days, putting us well on pace toward achieving our two-year goal of adding 300 gross net new miles."

Co lowers guidance for FY19, sees FY19 revs of $44.5-45.5 mln (Prior $45-47 mln) vs. $46.12 mln S&P Capital IQ Consensus citing delays in the contract negotiation and approval process with two new potential customers and the loss of one customer that had a contract of seven miles.

GoPro esimese kvartali müük oli oodatust parem ning tänu tõhusamale kulude juhtimisele jäi ka kahjum arvatust väiksemaks. Kogu majandusaasta aktsiakasumi keskpunkt jääb konsensuse omast 5 sendi võrra kõrgemale.

Reports Q1 (Mar) adj. loss of $0.07 per share, $0.02 better than the S&P Capital IQ Consensus of ($0.09); revenues rose 20.1% year/year to $243 mln vs the $234.41 mln S&P Capital IQ Consensus. Excluding the aerial business, revenue would have increased 27% year-over-year.

"We are innovating in all areas of our business and driving disciplined expense and inventory management. We believe this, combined with the release of exciting new products, will drive continued growth and as a result we are raising revenue and full-year non-GAAP profitability guidance for 2019."

expects FY 19 adj. EPS of $0.25-0.45 vs $0.30 consensus

expects FY 19 revenue growth of 7-10% vs 5-8% previous guidance and 6% estimate

notes revenue growth primarily from increased ASPs

Reports Q1 (Mar) adj. loss of $0.07 per share, $0.02 better than the S&P Capital IQ Consensus of ($0.09); revenues rose 20.1% year/year to $243 mln vs the $234.41 mln S&P Capital IQ Consensus. Excluding the aerial business, revenue would have increased 27% year-over-year.

"We are innovating in all areas of our business and driving disciplined expense and inventory management. We believe this, combined with the release of exciting new products, will drive continued growth and as a result we are raising revenue and full-year non-GAAP profitability guidance for 2019."

expects FY 19 adj. EPS of $0.25-0.45 vs $0.30 consensus

expects FY 19 revenue growth of 7-10% vs 5-8% previous guidance and 6% estimate

notes revenue growth primarily from increased ASPs

Täna alustasid Zoomi katmist mitmed analüüsimajad, nähes ettevõttes suurt potentsiaali, ent see on üldiselt nende arvates ka juba tänasesse hinda sisse arvestatud. Lähikvartalite tulemused näitavad, kas kasvu osas on veel ruumi üllatada või mitte.

JMP Securities initiated coverage of Zoom Video Communications Inc. with a recommendation of market perform.

Wells Fargo Securities initiated coverage of Zoom Video Communications Inc. with a recommendation of market

perform. PT set to $75

Stifel initiated coverage of Zoom Video Communications Inc. with a recommendation of hold. PT set to $75

Morgan Stanley initiated coverage of Zoom Video Communications Inc. with a recommendation of Equal-weight. PT set to $75

J.P. Morgan initiated coverage of Zoom Video Communications Inc. with a recommendation of overweight. PT set to $113

Goldman Sachs initiated coverage of Zoom Video Communications Inc. with a recommendation of neutral. PT set to $47

Piper Jaffray initiated coverage of Zoom Video Communications Inc. with a recommendation of overweight. PT set to $90

JMP Securities initiated coverage of Zoom Video Communications Inc. with a recommendation of market perform.

Wells Fargo Securities initiated coverage of Zoom Video Communications Inc. with a recommendation of market

perform. PT set to $75

Stifel initiated coverage of Zoom Video Communications Inc. with a recommendation of hold. PT set to $75

Morgan Stanley initiated coverage of Zoom Video Communications Inc. with a recommendation of Equal-weight. PT set to $75

J.P. Morgan initiated coverage of Zoom Video Communications Inc. with a recommendation of overweight. PT set to $113

Goldman Sachs initiated coverage of Zoom Video Communications Inc. with a recommendation of neutral. PT set to $47

Piper Jaffray initiated coverage of Zoom Video Communications Inc. with a recommendation of overweight. PT set to $90

Easyjeti esimese poolaasta müügitulu osutus ootuspäraseks, teise poolaasta müügitulu istme kohta peaks näitama väikest langust, mille taga on Brexit ja Euroopa majanduse jahtumine. Maksueelse kasumi prognoos jäeti siiski samaks.

* 1H revenue GBP2.34 billion, estimate GBP2.34 billion

* 1H headline pretax loss GBP275 million

* EasyJet says revenue per seat at constant currency for 2H now seen ‘slightly’ down

*EasyJet says says headline pretax views for financial year 2019 remain unchanged and in line,

according to a statement.

* Says rev per seat being down not helped by ongoing negative impact of Brexit-related market uncertainty, as well as wider macroeconomic slowdown in Europe

* 3Q forward bookings are 3 pct points behind last year at 72%

* Exchange rate movements likely to have around GBP10m positive impact on headline pretax compared to 12 months to Sept. 30 2018

* 1H revenue GBP2.34 billion, estimate GBP2.34 billion

* 1H headline pretax loss GBP275 million

* EasyJet says revenue per seat at constant currency for 2H now seen ‘slightly’ down

*EasyJet says says headline pretax views for financial year 2019 remain unchanged and in line,

according to a statement.

* Says rev per seat being down not helped by ongoing negative impact of Brexit-related market uncertainty, as well as wider macroeconomic slowdown in Europe

* 3Q forward bookings are 3 pct points behind last year at 72%

* Exchange rate movements likely to have around GBP10m positive impact on headline pretax compared to 12 months to Sept. 30 2018

Bath & Body Works üksuse arvatust parem tulemus aitas L-Brandsil jõuda teises kvartalis ootamatult kasumisse ning pisut kergitati ka kogu majandusaasta aktsiakasumi prognoosi alumist otsa

L Brands beats by $0.14, beats on revs; guides Q2 EPS below consensus; raises low end of FY20 EPS, in-line

Reports Q1 (Apr) earnings of $0.14 per share, $0.14 better than the S&P Capital IQ Consensus of ($0.00); revenues rose 0.1% year/year to $2.63 bln vs the $2.56 bln S&P Capital IQ Consensus.

The first quarter earnings per share result of $0.14 exceeded the company's guidance of about breakeven, driven by record results at Bath & Body Works

Comparable sales for the first quarter ended May 4, 2019, were flat vs. -1.3% ests.

First quarter comparable sales declined 5% at the Victoria's Secret segment and increased 13% at Bath & Body Works.

Co issues downside guidance for Q2, sees EPS of $0.15-0.20 vs. $0.23 S&P Capital IQ Consensus.

Co issues in-line guidance for FY20, sees EPS of $2.30-2.60 from $2.20-2.60 vs. $2.37 S&P Capital IQ Consensus.

L Brands beats by $0.14, beats on revs; guides Q2 EPS below consensus; raises low end of FY20 EPS, in-line

Reports Q1 (Apr) earnings of $0.14 per share, $0.14 better than the S&P Capital IQ Consensus of ($0.00); revenues rose 0.1% year/year to $2.63 bln vs the $2.56 bln S&P Capital IQ Consensus.

The first quarter earnings per share result of $0.14 exceeded the company's guidance of about breakeven, driven by record results at Bath & Body Works

Comparable sales for the first quarter ended May 4, 2019, were flat vs. -1.3% ests.

First quarter comparable sales declined 5% at the Victoria's Secret segment and increased 13% at Bath & Body Works.

Co issues downside guidance for Q2, sees EPS of $0.15-0.20 vs. $0.23 S&P Capital IQ Consensus.

Co issues in-line guidance for FY20, sees EPS of $2.30-2.60 from $2.20-2.60 vs. $2.37 S&P Capital IQ Consensus.

Ei tea, kas see tehnoloogia kunagi ilmavalgust näeb, aga taas üks viis tarbijate vajaduste tuvastamiseks

Amazon Is Working on a Device That Can Read Human Emotions

Amazon Is Working on a Device That Can Read Human Emotions

Shockwave Medical on põnev ettevõte aga väga kallis. Siiski lisan nimekirja ja hoiame edaspidi silma peal.

Uus tehnoloogia ateroskleroosi ravis

Uus tehnoloogia ateroskleroosi ravis

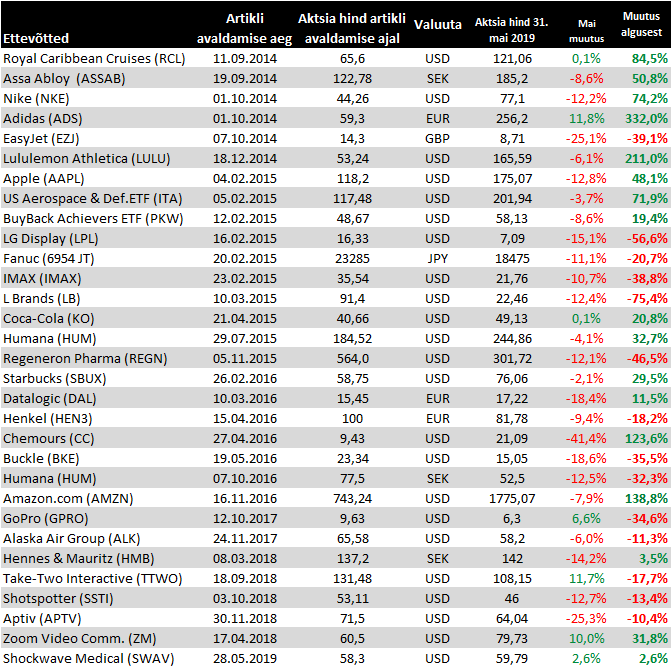

Muutused mai lõpu seisuga

Zoom raporteeris börsiettevõttena oma esimesed tulemused, prognoosides tänavu 63% müügitulu kasvu 538 miljoni dollarini võrreldes mullusega (2018.a 118%) ning see osutuks arvatust veidi suuremaks. Selle baasil kaupleb ettevõte 38x EV/Sales kordajaga, mis mõistagi on väga kõrge.

Reports Q1 (Apr) adj. earnings of $0.03 per share, $0.02 better than the S&P Capital IQ Consensus of $0.01; revenues rose 103.1% year/year to $122 mln vs the $111.66 mln S&P Capital IQ Consensus.

At the end of the first quarter of fiscal 2020, Zoom had: Approximately 58,500 customers with more than 10 employees, up ~86% from the same quarter last year. 405 customers contributing more than $100,000 in trailing 12 months revenue, up ~120% from the same quarter last year. A trailing 12-month net dollar expansion rate in customers with greater than 10 employees above 130% for the 4th consecutive quarter.

Co issues upside guidance for Q2, sees EPS of $0.01-0.02, excluding non-recurring items, vs. $0.01 S&P Capital IQ Consensus; sees Q2 revs of $129-130 mln vs. $122.06 mln S&P Capital IQ Consensus.

Co issues upside guidance for FY20, sees EPS of $0.02-0.03, excluding non-recurring items, vs. ($0.01) S&P Capital IQ Consensus; sees FY20 revs of $535-540 mln vs. $520.25 mln S&P Capital IQ Consensus.

Reports Q1 (Apr) adj. earnings of $0.03 per share, $0.02 better than the S&P Capital IQ Consensus of $0.01; revenues rose 103.1% year/year to $122 mln vs the $111.66 mln S&P Capital IQ Consensus.

At the end of the first quarter of fiscal 2020, Zoom had: Approximately 58,500 customers with more than 10 employees, up ~86% from the same quarter last year. 405 customers contributing more than $100,000 in trailing 12 months revenue, up ~120% from the same quarter last year. A trailing 12-month net dollar expansion rate in customers with greater than 10 employees above 130% for the 4th consecutive quarter.

Co issues upside guidance for Q2, sees EPS of $0.01-0.02, excluding non-recurring items, vs. $0.01 S&P Capital IQ Consensus; sees Q2 revs of $129-130 mln vs. $122.06 mln S&P Capital IQ Consensus.

Co issues upside guidance for FY20, sees EPS of $0.02-0.03, excluding non-recurring items, vs. ($0.01) S&P Capital IQ Consensus; sees FY20 revs of $535-540 mln vs. $520.25 mln S&P Capital IQ Consensus.

Lisan nimekirja Mellanoxi, et jälgida, kas ettevõtte ülevõtmine Nvidia poolt lõpuks õnnestub või mitte. Üks sarnane juhtum on siin 2015. aastast Humana näol juba olemas, mis teatavasti jooksis liiva, kuid sellele vaatamata on ettevõtte edasine kasv viinud aktsiahinna tänaseks juba kõrgemale.

Aktsiaturul pakutakse ühte kerget saaki?

Aktsiaturul pakutakse ühte kerget saaki?

Erinealt paljudest teistest rõivaste jaemüüjatest läheb Lululemonil jätkuvalt hästi ning lisaks kergitati vaatamata tariifidest tingitud kulude kasvule kogu majandusaasta väljavaadet.

Lululemon reports Q1 (Apr) earnings of $0.74 per share, $0.04 better than the S&P Capital IQ Consensus of $0.70; revenues rose 20.4% year/year to $782.3 mln vs the $755.92 mln S&P Capital IQ Consensus.

Based on a shifted calendar, total comparable sales increased 14%, or increased 16% on a constant dollar basis vs. low double digit guidance. Comparable store sales increased 6%, or increased 8% on a constant dollar basis. Direct to consumer net revenue increased 33%, or increased 35% on a constant dollar basis. Gross margin was 53.9%, an increase of 80 basis points compared to the first quarter of fiscal 2018.

Co issues in-line guidance for Q2, sees EPS of $0.86-0.88 vs. $0.88 S&P Capital IQ Consensus; sees Q2 revs of $825-835 mln vs. $834.76 mln S&P Capital IQ Consensus; low-double digit comps ex-FX.

Co issues downside guidance for FY20, raises EPS to $4.51-4.58 from $4.48-4.55 vs. $4.62 S&P Capital IQ Consensus; raises FY20 revs to $3.73-3.77 bln from $3.70-3.74 bln vs. $3.77 bln S&P Capital IQ Consensus; reaffirms low-double digit comps ex-FX.

Lululemon reports Q1 (Apr) earnings of $0.74 per share, $0.04 better than the S&P Capital IQ Consensus of $0.70; revenues rose 20.4% year/year to $782.3 mln vs the $755.92 mln S&P Capital IQ Consensus.

Based on a shifted calendar, total comparable sales increased 14%, or increased 16% on a constant dollar basis vs. low double digit guidance. Comparable store sales increased 6%, or increased 8% on a constant dollar basis. Direct to consumer net revenue increased 33%, or increased 35% on a constant dollar basis. Gross margin was 53.9%, an increase of 80 basis points compared to the first quarter of fiscal 2018.

Co issues in-line guidance for Q2, sees EPS of $0.86-0.88 vs. $0.88 S&P Capital IQ Consensus; sees Q2 revs of $825-835 mln vs. $834.76 mln S&P Capital IQ Consensus; low-double digit comps ex-FX.

Co issues downside guidance for FY20, raises EPS to $4.51-4.58 from $4.48-4.55 vs. $4.62 S&P Capital IQ Consensus; raises FY20 revs to $3.73-3.77 bln from $3.70-3.74 bln vs. $3.77 bln S&P Capital IQ Consensus; reaffirms low-double digit comps ex-FX.

H&M avaldas eile oma teise kvartali müügi, mis osutus oodatust veidi paremaks, ent olulisem saab olema 27. juunil selguv täiendav info varude ja kasumlikkuse kohta

* 2Q sales SEK57.47 billion, estimate SEK57.14 billion (range SEK55.93 billion to SEK58.20 billion) (Bloomberg data)

* 2Q sales in local currencies +6%

* "The rapid changes in the fashion industry continue and we can see that our own transformation work is taking us in the right direction, although hard work and many challenges still remain," H&M says

* "As customer satisfaction and sales increase, we have intensified our transformation work even further"

* 2Q sales SEK57.47 billion, estimate SEK57.14 billion (range SEK55.93 billion to SEK58.20 billion) (Bloomberg data)

* 2Q sales in local currencies +6%

* "The rapid changes in the fashion industry continue and we can see that our own transformation work is taking us in the right direction, although hard work and many challenges still remain," H&M says

* "As customer satisfaction and sales increase, we have intensified our transformation work even further"

H&M teise kvartali maksueelne kasum kujunes üsna ootuspäraseks, julgustava märgina on juuni alanud ettevõtte jaoks edukalt, mida ilmselt on soosinud hea ilm.

H&M reported pretax profit for the second quarter of SEK5.93 billion vs est. SEK6.0 billion.

* 2Q gross margin 55.4%, estimate 55.5% (Bloomberg data)

* 2Q net income SEK4.57 billion, estimate SEK4.62 billion (range SEK4.31 billion to SEK4.80 billion) (BD)

* Says composition of stock-in-trade continues to improve

* Online sales rose by 27% in SEK and 20% in local currencies

OUTLOOK

* Sales of the summer collections got off to a "very good" start; net sales in the month of June is estimated to increase by 12% in local currencies compared with the corresponding month the previous year (Q2 +6%)

* Sees costs of markdowns in relation to sales decreasing by around 1.5 percentage points in 3Q 2019 compared with 3Q 2018

* To accelerate adaptation to customers’ changed shopping patterns and therefore net addition of new stores for 2019 will be around 130, 45 fewer than previously communicated

* Thailand, Indonesia and Egypt will become new H&M online markets via franchise during 2H 2019

H&M reported pretax profit for the second quarter of SEK5.93 billion vs est. SEK6.0 billion.

* 2Q gross margin 55.4%, estimate 55.5% (Bloomberg data)

* 2Q net income SEK4.57 billion, estimate SEK4.62 billion (range SEK4.31 billion to SEK4.80 billion) (BD)

* Says composition of stock-in-trade continues to improve

* Online sales rose by 27% in SEK and 20% in local currencies

OUTLOOK

* Sales of the summer collections got off to a "very good" start; net sales in the month of June is estimated to increase by 12% in local currencies compared with the corresponding month the previous year (Q2 +6%)

* Sees costs of markdowns in relation to sales decreasing by around 1.5 percentage points in 3Q 2019 compared with 3Q 2018

* To accelerate adaptation to customers’ changed shopping patterns and therefore net addition of new stores for 2019 will be around 130, 45 fewer than previously communicated

* Thailand, Indonesia and Egypt will become new H&M online markets via franchise during 2H 2019

Nike'i müügitulu kasvas neljandas kvartalis 10% võrreldes aastatagusega, kuid dollari tugevnemine sõi sellest üsna suure osa ära ning raporteeritud kavuks kujunes 4%, mis osutus ootuspäraseks. Kasumireale avaldasid täiendavat survet suuremad kulud ja kõrgem maksumäär, millest tulenevalt osutus EPS oodatust madalamaks. Valuutaneutraalseid tulemusi vaadates kasvas kogu 2019 fiskaalaasta käive 11% ja ärikasum 14% ning 2020.a peaks ettevõtte kohaselt jätkuma üsna korralik kasv (valuutaneutraalne müügitulu kõrge ühekohalise protsendi jagu, millele lisaks nähakse marginaalide paranemise ruumi).

Nike reports Q4 (May) earnings of $0.62 per share, $0.04 worse than the S&P Capital IQ Consensus of $0.66; driven by strong revenue growth, gross margin expansion, and a lower average share count, which were slightly offset by higher selling and administrative expense and a higher tax rate (20.4%).

Revenues rose 4.0% year/year to $10.18 bln vs the $10.15 bln S&P Capital IQ Consensus. Revenues for the NIKE Brand were $9.7 billion, up 10 percent on a currency-neutral basis, driven by growth across NIKE Direct and wholesale, key categories including Sportswear, Jordan and Basketball, and continued growth across footwear and apparel. Revenues for Converse were $491 million, flat to prior year on a currency-neutral basis, mainly driven by double-digit growth in Asia and digital which was offset by declines in the U.S. and Europe.

North American sales +8% ex-FX; EMEA +9% ex-FX; Greater China +22%, APacLatAm +9%

Footwear +12% ex-FX, Apparel +8%, Equipment +11%

The outlook for the full year reported revenue growth remains in the high single digit range, slightly exceeding reported revenue growth in fiscal year 2019. Expects another year of broad based growth in all four geographies. Expects gross margin expansion potentially approaching 50 basis points. Sees continued strong operational margin expansion.

Nike reports Q4 (May) earnings of $0.62 per share, $0.04 worse than the S&P Capital IQ Consensus of $0.66; driven by strong revenue growth, gross margin expansion, and a lower average share count, which were slightly offset by higher selling and administrative expense and a higher tax rate (20.4%).

Revenues rose 4.0% year/year to $10.18 bln vs the $10.15 bln S&P Capital IQ Consensus. Revenues for the NIKE Brand were $9.7 billion, up 10 percent on a currency-neutral basis, driven by growth across NIKE Direct and wholesale, key categories including Sportswear, Jordan and Basketball, and continued growth across footwear and apparel. Revenues for Converse were $491 million, flat to prior year on a currency-neutral basis, mainly driven by double-digit growth in Asia and digital which was offset by declines in the U.S. and Europe.

North American sales +8% ex-FX; EMEA +9% ex-FX; Greater China +22%, APacLatAm +9%

Footwear +12% ex-FX, Apparel +8%, Equipment +11%

The outlook for the full year reported revenue growth remains in the high single digit range, slightly exceeding reported revenue growth in fiscal year 2019. Expects another year of broad based growth in all four geographies. Expects gross margin expansion potentially approaching 50 basis points. Sees continued strong operational margin expansion.

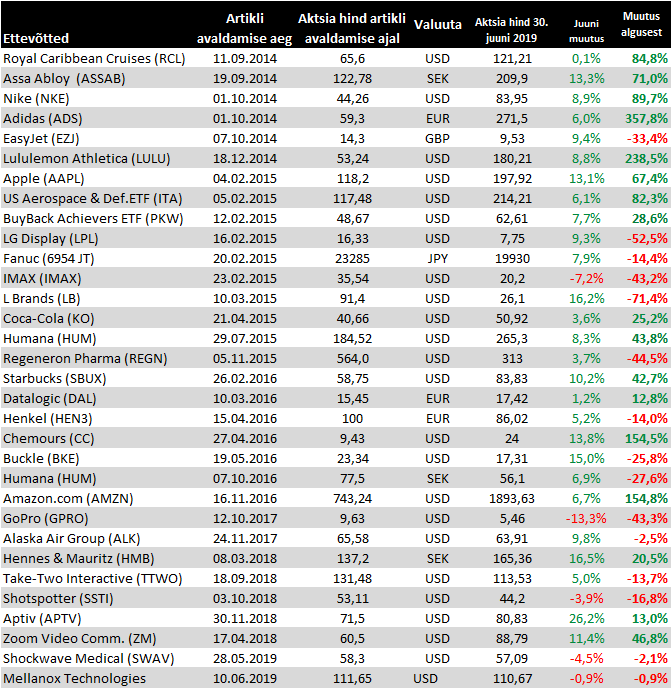

Muutused juuni lõpu seisuga

Assa Abloy teise kvartali tulemused kujunesid üsna ootuspäraseks

* 2Q adjusted operating profit SEK3.73 billion, estimate SEK3.69 billion (range SEK3.61 billion to SEK3.81 billion) (Bloomberg data)

* 2Q sales SEK23.54 billion, estimate SEK23.46 billion (range SEK23.22 billion to SEK23.83 billion) (BD)

* 2Q organic revenue +3%

* CEO says demand ''has generally been good in 2019, but with variations between different markets. In some markets, uncertainty has increased at the same time due to weaker construction indices and geopolitical challenges''

* 2Q adjusted operating profit SEK3.73 billion, estimate SEK3.69 billion (range SEK3.61 billion to SEK3.81 billion) (Bloomberg data)

* 2Q sales SEK23.54 billion, estimate SEK23.46 billion (range SEK23.22 billion to SEK23.83 billion) (BD)

* 2Q organic revenue +3%

* CEO says demand ''has generally been good in 2019, but with variations between different markets. In some markets, uncertainty has increased at the same time due to weaker construction indices and geopolitical challenges''

Starbucks tõestas eile avaldatud oodatust paremate tulemuste ning kasumiprognoosiga, et on suutnud ettevõtte taas kasvama panna. Suureneva konkurentsi tingimustes on pandud kinni ebaefektiivseid kohvikuid, lisatud menüüdesse uusi joogi- ja söögipakkumisi ning samuti on olulise panuse andnud aprillis muudetud lojaalsusproramm, mis on aidanud tuua kliente juurde, pannud nad rohkem kulutama ja tihemini Starbucksi külastama.

Reports Q3 (Jun) earnings of $0.78 per share, $0.05 better than the S&P Capital IQ Consensus of $0.73; revenues rose 8.1% year/year to $6.82 bln vs the $6.67 bln S&P Capital IQ Consensus.

Global comparable store sales increased 6%, driven by a 3% increase in average ticket and a 3% increase in comparable transactions

Americas comparable store sales increased 7%, driven by a 4% increase in average ticket and a 3% increase in transactions; U.S. comparable store sales increased 7%, with transactions up 3%

China/Asia Pacific comparable store sales increased 5%, driven by a 3% increase in average ticket and a 2% increase in transactions; China comparable store sales increased 6%, with transactions up 2%

Non-GAAP operating margin of 18.3% declined 20 basis points compared to the prior year.

Co issues upside guidance for FY19, sees EPS of $2.80-2.82, excluding non-recurring items, vs. $2.80 S&P Capital IQ Consensus.

Global comparable store sales growth of approximately 4% (previously 3% to 4%)

Consolidated GAAP revenue growth of approximately 7% (previously 5% to 7%)

Reports Q3 (Jun) earnings of $0.78 per share, $0.05 better than the S&P Capital IQ Consensus of $0.73; revenues rose 8.1% year/year to $6.82 bln vs the $6.67 bln S&P Capital IQ Consensus.

Global comparable store sales increased 6%, driven by a 3% increase in average ticket and a 3% increase in comparable transactions

Americas comparable store sales increased 7%, driven by a 4% increase in average ticket and a 3% increase in transactions; U.S. comparable store sales increased 7%, with transactions up 3%

China/Asia Pacific comparable store sales increased 5%, driven by a 3% increase in average ticket and a 2% increase in transactions; China comparable store sales increased 6%, with transactions up 2%

Non-GAAP operating margin of 18.3% declined 20 basis points compared to the prior year.

Co issues upside guidance for FY19, sees EPS of $2.80-2.82, excluding non-recurring items, vs. $2.80 S&P Capital IQ Consensus.

Global comparable store sales growth of approximately 4% (previously 3% to 4%)

Consolidated GAAP revenue growth of approximately 7% (previously 5% to 7%)

Amazon ületas küll müügitulu ootust aga kasum jäi arvatust väiksemaks ning samuti tõotab see olla arvatust tagasihoilikum jooksval kvartalil peamiselt ühepäevasesse tarnesse tehtavate investeeringute tõttu. Küsimusi võib tekitada ka AWS müügitulu kasvu aeglustumine 41,4% pealt 37,3%le,

Amazon reports Q2 (Jun) earnings of $5.22 per share, $0.32 worse than the S&P Capital IQ Consensus of $5.63; revenues rose 19.9% year/year to $63.4 bln vs the $62.59 bln S&P Capital IQ Consensus.

Operating income +3% to $3.0 bln vs. $2.6-3.6 bln guidance and $3.65 bln ests.

AWS rev +37% to $8.38 bln; operating margin -140 bps.

North American sales accelerate to +20% to $38.65 bln; operating margin -170 bps to 4.0%

Co issues in-line guidance for Q3, sees Q3 revs of $66-70 bln vs. $67.36 bln S&P Capital IQ Consensus. Operating income is expected to be between $2.1 billion and $3.1 billion vs. $4.38 bln ests, compared with $3.7 billion in third quarter 2018.

Amazon reports Q2 (Jun) earnings of $5.22 per share, $0.32 worse than the S&P Capital IQ Consensus of $5.63; revenues rose 19.9% year/year to $63.4 bln vs the $62.59 bln S&P Capital IQ Consensus.

Operating income +3% to $3.0 bln vs. $2.6-3.6 bln guidance and $3.65 bln ests.

AWS rev +37% to $8.38 bln; operating margin -140 bps.

North American sales accelerate to +20% to $38.65 bln; operating margin -170 bps to 4.0%

Co issues in-line guidance for Q3, sees Q3 revs of $66-70 bln vs. $67.36 bln S&P Capital IQ Consensus. Operating income is expected to be between $2.1 billion and $3.1 billion vs. $4.38 bln ests, compared with $3.7 billion in third quarter 2018.

Apple avaldas eile ootuspärase kolmanda kvartali müügitulu juures arvatust parema aktsiakasumi ning prognoosib konsensusest tugevamat neljanda kvartali käivet

Apple reports Q3 (Jun) earnings of $2.18 per share, $0.08 better than the S&P Capital IQ Consensus of $2.10; revenues rose 1.0% year/year to $53.81 bln vs the $53.39 bln S&P Capital IQ Consensus.

iPhone revenue -12% to $26 bln vs. $26 bln ests

Service rev +13% to $11.46 bln; iPad +8% to $5.0 bln; wearables, home accessories +48% to $5.5 bln

Americas rev +2% to $25.06 bln Europe rev -2% to $11.9 bln China rev -4% to $9.16 bln Japan rev +6% to $4.08 bln Asia Pac +13% to $3.59 bln

Q3 gross margin of 37.6% vs ests of 38.1% vs 38.3% last year; services gross margins 64.1% vs ests for slight improvement from 63.8% last quarter

Co issues upside guidance for Q4, sees Q4 revs of $61-64 bln vs. $60.92 bln S&P Capital IQ Consensus; sees gross margin 37.5-38.5% vs ests of 38.3% and 38.3% last year.

Apple reports Q3 (Jun) earnings of $2.18 per share, $0.08 better than the S&P Capital IQ Consensus of $2.10; revenues rose 1.0% year/year to $53.81 bln vs the $53.39 bln S&P Capital IQ Consensus.

iPhone revenue -12% to $26 bln vs. $26 bln ests

Service rev +13% to $11.46 bln; iPad +8% to $5.0 bln; wearables, home accessories +48% to $5.5 bln

Americas rev +2% to $25.06 bln Europe rev -2% to $11.9 bln China rev -4% to $9.16 bln Japan rev +6% to $4.08 bln Asia Pac +13% to $3.59 bln

Q3 gross margin of 37.6% vs ests of 38.1% vs 38.3% last year; services gross margins 64.1% vs ests for slight improvement from 63.8% last quarter

Co issues upside guidance for Q4, sees Q4 revs of $61-64 bln vs. $60.92 bln S&P Capital IQ Consensus; sees gross margin 37.5-38.5% vs ests of 38.3% and 38.3% last year.

Aptivilt teenis ootuspärase müügitulu baasil arvatust parema aktsiakasumi, kergitab majandusaasta käibe konsensuse ootuse juurde, aktsiakasumi aga kõrgemale

Aptiv reports Q2 (Jun) earnings of $1.33 per share, excluding non-recurring items, $0.19 better than the S&P Capital IQ Consensus of $1.14; revenues fell 1.5% year/year to $3.63 bln vs the $3.64 bln S&P Capital IQ Consensus. Revenue increased 4% adjusted for currency exchange, commodity movements and divestitures. This reflects growth of 7% in Europe, 2% in Asia, which includes a decline of 6% in China, 1% in North America and 14% in South America.

Co issues in-line guidance for Q3, sees EPS of $1.27-1.33, excluding non-recurring items, vs. $1.32 S&P Capital IQ Consensus; sees Q3 revs of $3.6-3.7 bln vs. $3.64 bln S&P Capital IQ Consensus.

Co issues guidance for FY19, raises EPS to $5.05-5.15 from $4.90-5.10, excluding non-recurring items, vs. $4.98 S&P Capital IQ Consensus; sees FY19 revs of $14.525-14.725 bln from $14.425-14.825 bln vs. $14.68 bln S&P Capital IQ Consensus.

Aptiv reports Q2 (Jun) earnings of $1.33 per share, excluding non-recurring items, $0.19 better than the S&P Capital IQ Consensus of $1.14; revenues fell 1.5% year/year to $3.63 bln vs the $3.64 bln S&P Capital IQ Consensus. Revenue increased 4% adjusted for currency exchange, commodity movements and divestitures. This reflects growth of 7% in Europe, 2% in Asia, which includes a decline of 6% in China, 1% in North America and 14% in South America.

Co issues in-line guidance for Q3, sees EPS of $1.27-1.33, excluding non-recurring items, vs. $1.32 S&P Capital IQ Consensus; sees Q3 revs of $3.6-3.7 bln vs. $3.64 bln S&P Capital IQ Consensus.

Co issues guidance for FY19, raises EPS to $5.05-5.15 from $4.90-5.10, excluding non-recurring items, vs. $4.98 S&P Capital IQ Consensus; sees FY19 revs of $14.525-14.725 bln from $14.425-14.825 bln vs. $14.68 bln S&P Capital IQ Consensus.