Mx77, pigem aitab see mõttetegevust korras hoida. Vaata näiteks tänast "Tambiks veidi vasakpoolseid"-mõttelõnga! Muidu siiani terava mõistusega silma paistnud arvajad on täna selget mõttelaiskust- ja jäikust üles näidanud. Kaalun ka ise vabas teemas osalemisest loobumist. Mõelda ja arvata tuleb, aga samamoodi tuleb ka oma mõtlemisoskust tervena hoida.

mx77

Kas LHV vaba teema mittelugemine jääb kuskile agronatsluse ja twitteri avangadi vahele? :D

jahe

Mx77, pigem aitab see mõttetegevust korras hoida. Vaata näiteks tänast "Tambiks vasakpoolseid"-mõttelõnga! Muidu siiani terava mõistusega silma paistnud arvajad on täna selget mõttelaiskust- ja jäikust üles näidanud. Kaalun ka ise vabas teemas osalemisest loobumist. Mõelda ja arvata tuleb, aga samamoodi tuleb ka oma mõtlemisoskust tervena hoida.

Sitta sest muidu teravate mõttelaiskusest ja -jäikusest. See on OK. Probleemiks on pigem see, et 40% vaba teema sisust toodab üks peast haige rassist, kelle seisukohtade populaarsus lubab eeldada, et see on adekvaatne läbilõige isegi investeerimisfoorumi keskmisest lugejast. Kerge õud tuleb peale, mida see veel ühiskonna keskmise kohta ütleb...

Sellega pole absoluutselt nõus, et koos UK'ga saab parima reformi. Hobuseredis. Nad hea meelega reformiks EL'i olukorda, kus nad saavad valida, keda ja kuidas nad Ungari-Slovakkia sõjas toetavad. Ideaalvariandis mõlemat ja selliselt, et ka teised naabrid madinaga liituvad.

Jään eriarvamusele. UK on kõikide EL reformide juures olnud siiani ja üldiselt Eesti ja UK leiavad nendel teemadel alati üsna suure ühisosa, kui nende see rebate jm erandid kõrvale jätta. UK MEPid on väga mõistlikud näiteks, v.a. Farage gang. Nagu öö ja päev võrreldes mingite Kreeka anarhistide või Itaalia kommunistidega vms, kes Putini särgiga ringi käivad.

suffiks

Sitta sest muidu teravate mõttelaiskusest ja -jäikusest. See on OK. Probleemiks on pigem see, et 40% vaba teema sisust toodab üks peast haige rassist, kelle seisukohtade populaarsus lubab eeldada, et see on adekvaatne läbilõige isegi investeerimisfoorumi keskmisest lugejast. Kerge õud tuleb peale, mida see veel ühiskonna keskmise kohta ütleb...

Karumõmm? :O

Ainuke huvitav vabateema on Kalev Jaik. Kas on inimest, kes on kogu teema läbi lugenud?

Kalev, ära anna alla!

Kalev, ära anna alla!

EU's Jean-Claude Juncker set to wade into Brexit battle after poll ...

http://www.dailymail.co.uk/news/article-3641392/Is-Remain-s-chance-EU-s-bureaucrat-set-wade-Brexit-battle-poll-leads-Leave-mean-break-secret-deal-Cameron-quiet.html

http://www.dailymail.co.uk/news/article-3641392/Is-Remain-s-chance-EU-s-bureaucrat-set-wade-Brexit-battle-poll-leads-Leave-mean-break-secret-deal-Cameron-quiet.html

Lugesin ka Jaiki teemat alguses usinalt, aga seal läks ikka mõne foorumikasutaja poolt ikka väga veidi segase vanainimese arvelt odava ajaviite saamiseks kätte.

mx77

Lugesin ka Jaiki teemat alguses usinalt, aga seal läks ikka mõne foorumikasutaja poolt ikka väga veidi segase vanainimese arvelt odava ajaviite saamiseks kätte.

No jaiki küsimustele on üldiselt üpriski primitiivsed vastused ja need on enamasti juba esimese paari tuhande kommentaariga ära vastatud, a ikka leidub inimesi kes vanahärrale üritavad matemaatikat ja füüsikat õpetada :)

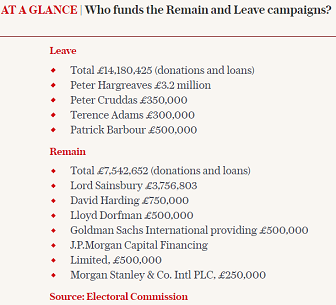

Kust raha tuleb?

Citi andis ka remainile 250k

http://www.telegraph.co.uk/news/2016/05/15/eu-referendum-more-than-300-business-leaders-back-a-brexit/

Citi andis ka remainile 250k

http://www.telegraph.co.uk/news/2016/05/15/eu-referendum-more-than-300-business-leaders-back-a-brexit/

Kuidas foorumlastel seis on, juba ammu rahasse ära mindud või plaanis lähipäevadel positsioone vähendada? Või jätab külmaks ja ei tee midagi?

http://www.aripaev.ee/uudised/2016/06/16/deutsche-banki-juht-brexit-oleks-katastroof

http://www.aripaev.ee/uudised/2016/06/16/deutsche-banki-juht-brexit-oleks-katastroof

Minul tekkis küll kergekujuline paanika. Läksin eelmise nädala lõpuks 100 % rahasse ja ootan põõsas kuni jaanik möödas.

See on Tallinna börsi suurim viga, et ei saa lühikeseks müüa, kui turg kukub, siis istud rahas ja imed näppu. Languse pealt kasumit pole võimalik teenida.

Fake McCoy

See on Tallinna börsi suurim viga, et ei saa lühikeseks müüa, kui turg kukub, siis istud rahas ja imed näppu. Languse pealt kasumit pole võimalik teenida.

Tallinas on börs vöi?

Ega vist isegi habemega juut ei oska ennustada millised kõikumised tulevad. Mõni aeg tagasi kui väike Kreeka hääletas korraks EI oli normaalne liikumine turgudel. Muidu Euroopa majandusnäitajad on ju suht normaalsed, JA korral võiks tulla korralik tõus? Ei korral võivad suurte pankade bossid veel "vinti peale keerata" langusele?

pregu ei julge langusele ka mängida. kõige kindlam on rahas istuda ja kannatada.

Raha on ju lihtsalt kokkuleppelise väärtusega paber, targem ikka mingeid asju osta. Või soola.

Peegeldaks meenutuse aastast 1964 kui oodati sarnaseid kõikumisi ja nende tagajärgi.

Ei vihja seeläbi turulangusele ega tõusule.

The ultimate consequence of unchecked currency weakness is something that may be incomparably

more disastrous in its effects than family bankruptcy. This is devaluation, and devaluation of a key

world currency like the pound is the recurrent nightmare of all central bankers, whether in London,

New York, Frankfurt, Zurich, or Tokyo. If at any time the drain on Britain’s reserves became so great that the Bank of England was unable, or unwilling, to fulfill its obligation to maintain the pound at

$2.78, the necessary result would be devaluation. That is, the $2.78-to-$2.82 limitation would be

abruptly abrogated; by simple government decree the par value of the pound would be reduced to

some lower figure, and a new set of limits established around the new parity. The heart of the danger was the possibility that what followed might be chaos not confined to Britain. Devaluation, as the most heroic and most dangerous of remedies for a sick currency, is rightly feared. By making the devaluing country’s goods cheaper to others, it boosts exports, and thus reduces or eliminates a

deficit in international accounts, but at the same time it makes both imports and domestic goods more expensive at home, and thus reduces the country’s standard of living. It is radical surgery, curing a disease at the expense of some of the patient’s strength and well-being—and, in many cases, some of his pride and prestige as well. Worst of all, if the devalued currency is one that, like the pound, is widely used in international dealings, the disease—or, more precisely, the cure—is likely to prove contagious. To nations holding large amounts of that particular currency in their reserve vaults, the effects of the devaluation is the same as if the vaults had been burglarized. Such nations and others, finding themselves at an unacceptable trading disadvantage as a result of the devaluation, may have to resort to competitive devaluation of their own currencies. A downward spiral develops: Rumors of further devaluations are constantly in the wind; the loss of confidence in other people’s money leads to a disinclination to do business across national borders; and international trade, upon which depend the food and shelter of hundreds of millions of people around the world, tends to decline. Just such a disaster followed the classic devaluation of all time, the departure of the pound from the old gold standard in 1931—an event that is still generally considered a major cause of the worldwide Depression of the thirties.

Ei vihja seeläbi turulangusele ega tõusule.

The ultimate consequence of unchecked currency weakness is something that may be incomparably

more disastrous in its effects than family bankruptcy. This is devaluation, and devaluation of a key

world currency like the pound is the recurrent nightmare of all central bankers, whether in London,

New York, Frankfurt, Zurich, or Tokyo. If at any time the drain on Britain’s reserves became so great that the Bank of England was unable, or unwilling, to fulfill its obligation to maintain the pound at

$2.78, the necessary result would be devaluation. That is, the $2.78-to-$2.82 limitation would be

abruptly abrogated; by simple government decree the par value of the pound would be reduced to

some lower figure, and a new set of limits established around the new parity. The heart of the danger was the possibility that what followed might be chaos not confined to Britain. Devaluation, as the most heroic and most dangerous of remedies for a sick currency, is rightly feared. By making the devaluing country’s goods cheaper to others, it boosts exports, and thus reduces or eliminates a

deficit in international accounts, but at the same time it makes both imports and domestic goods more expensive at home, and thus reduces the country’s standard of living. It is radical surgery, curing a disease at the expense of some of the patient’s strength and well-being—and, in many cases, some of his pride and prestige as well. Worst of all, if the devalued currency is one that, like the pound, is widely used in international dealings, the disease—or, more precisely, the cure—is likely to prove contagious. To nations holding large amounts of that particular currency in their reserve vaults, the effects of the devaluation is the same as if the vaults had been burglarized. Such nations and others, finding themselves at an unacceptable trading disadvantage as a result of the devaluation, may have to resort to competitive devaluation of their own currencies. A downward spiral develops: Rumors of further devaluations are constantly in the wind; the loss of confidence in other people’s money leads to a disinclination to do business across national borders; and international trade, upon which depend the food and shelter of hundreds of millions of people around the world, tends to decline. Just such a disaster followed the classic devaluation of all time, the departure of the pound from the old gold standard in 1931—an event that is still generally considered a major cause of the worldwide Depression of the thirties.

Rinja

Raha on ju lihtsalt kokkuleppelise väärtusega paber, targem ikka mingeid asju osta. Või soola.

No mulle ei antud isegi pabereid. Ainult mingi number on kuvaril.

Huvitav, ma ei näe turgudel mingeid paanika märke. Ainus kahtlasem signaal on see, et kuld ületas 1300 USD/oz, kuid kulla tõusutrend oli paigas ka siis, kui BREXITi tõenäosused olid seal ca 25 juures.