Saksamaa veebruari tehaste tellimused +2,4% vs oodatud +0,5% (M/M) ja aastases lõikes +20,1% vs oodatud +17,4%. Euro kaupleb 0,62% kõrgemal $1,4309 tasemel.

Risto varasemale kommentaarile veel täienduseks, et 12 kuu võlakirjade nõudlus ületas pakkumist 2,6x vs 2,2x eelmisel korral. Seega sarnaselt möödunud nädala oksjonile kujunes nõudluse pool tugevaks ning see on ka pisut EUR/USD-i ja turgusid toetamas. EUR on dollari suhtes tugevnenud 1,4305 dollarile ja USA indeksite futuurid liiguvad hetkel 0,4-0,6% plusspoolel.

Millisest EUR/USD-i kursist hakkab kallis EUR Euroopa eksportijaid oluliselt segama?

1,500 ?

Keeruline öelda aga see piir võiks kusagilt sealt joosta. Üks empiiriline uuring on jõunud järeldusele, et Saksa eksportijate valuläveks on 1,55 dollarit. When Does It Hurt? The Exchange Rate “Pain Threshold” for German Exports

Kui kevad eelneb suvele, mis on ehituses kõrghooaeg ja sügis talvele, mis on ehituses madalhooaeg, siis millised on šansid et ehitusmaterjalitootja (OSB on USAs levinud sõrestikmajade üks peamisi kattematerjale), aktsiad tõusevad kevadel ja langevad sügisel? Kah mul Newtoni binoom.

Monsanto tulemused ootuspärased ning aktsiale eelturul suuremat mõju ei avalda (MON -0,16% @ 73,2 USD)

Monsanto prelim $1.87 vs $1.84 Thomson Reuters consensus; revs $4.13 bln vs $4.15 bln Thomson Reuters consensus

Monsanto reaffirms FY11 EPS of $2.72-2.82 vs $2.86 Thomson Reuters consensus

Monsanto prelim $1.87 vs $1.84 Thomson Reuters consensus; revs $4.13 bln vs $4.15 bln Thomson Reuters consensus

Monsanto reaffirms FY11 EPS of $2.72-2.82 vs $2.86 Thomson Reuters consensus

Gapping up

In reaction to strong earnings/guidance: BDCO +3.8%, VRNT +1.6%.

M&A news: AMLJ +12.8% (Microsemi announces superior offer to Acquire AML Communications for $2.50 per share in cash), ORCH (Orchid Cellmark to be acquired by LabCorp (LH) for $2.80/share for a total purchase price to stockholders and optionholders of ~$85.4 mln).

Select financial related names showing strength: IRE +6.9%, LYG +3.6%, BCS +3.6%, RBS +3.5%, NBG +2.9%, HBC +2.4%, BAC +1%.

Select metals/mining stocks trading higher: MT +2.2%, EXK +2.2%, GRS +2.1%, AG +2.0%, HL +1.8%, SVM +1.8%, HMY +1.8%, FCX +1.6%.

Other news: FRPT +4.2% (receives $46.6 mln award for delivery of 40 Buffalo vehicles), GLNG +3.9% (continued momentum), NXPI +3.2% (announced idOnDemand and NXPI will partner to bring smart card security to mobile device authentication), CLD +3.0% (positive mention in financial newspaper), NKTR +2.2% (continued strength), SI +1.2% (still checking for anything specific), LGCY +0.8% (announced it has entered into an agreement to purchase Permian Basin natural gas properties for $67 mln in cash).

Analyst comments: WPRT +4.3% (upgraded to Buy from Hold at Jefferies), RCL +1.8% (upgraded to Outperform from Neutral at Credit Suisse), BRCM +1.7% (upgraded to Outperform from Perform at Oppenheimer), URBN +1.4% (upgraded to Overweight from Neutral at Piper Jaffray), WTSLA +1.1% (upgraded to Overweight from Neutral at Piper Jaffray).

In reaction to strong earnings/guidance: BDCO +3.8%, VRNT +1.6%.

M&A news: AMLJ +12.8% (Microsemi announces superior offer to Acquire AML Communications for $2.50 per share in cash), ORCH (Orchid Cellmark to be acquired by LabCorp (LH) for $2.80/share for a total purchase price to stockholders and optionholders of ~$85.4 mln).

Select financial related names showing strength: IRE +6.9%, LYG +3.6%, BCS +3.6%, RBS +3.5%, NBG +2.9%, HBC +2.4%, BAC +1%.

Select metals/mining stocks trading higher: MT +2.2%, EXK +2.2%, GRS +2.1%, AG +2.0%, HL +1.8%, SVM +1.8%, HMY +1.8%, FCX +1.6%.

Other news: FRPT +4.2% (receives $46.6 mln award for delivery of 40 Buffalo vehicles), GLNG +3.9% (continued momentum), NXPI +3.2% (announced idOnDemand and NXPI will partner to bring smart card security to mobile device authentication), CLD +3.0% (positive mention in financial newspaper), NKTR +2.2% (continued strength), SI +1.2% (still checking for anything specific), LGCY +0.8% (announced it has entered into an agreement to purchase Permian Basin natural gas properties for $67 mln in cash).

Analyst comments: WPRT +4.3% (upgraded to Buy from Hold at Jefferies), RCL +1.8% (upgraded to Outperform from Neutral at Credit Suisse), BRCM +1.7% (upgraded to Outperform from Perform at Oppenheimer), URBN +1.4% (upgraded to Overweight from Neutral at Piper Jaffray), WTSLA +1.1% (upgraded to Overweight from Neutral at Piper Jaffray).

Gapping down

In reaction to disappointing earnings/guidance: AMSC -43.7%, (also downgraded to Market Perform from Strong Buy at Raymond James, downgraded to Hold at Brean Murray, downgraded to Underperform from Buy at Jefferies), MIND -6.5%, ANGO -4.3%, NTE -4.2%, MON -1.1%.

M&A news: CEPH -0.6% (Cephalon's Board of Directors rejects Valeant Pharmaceuticals' unsolicited proposal of $73).

Select AMSC peers and related names ticking lower: CWS -3.3%, ZOLT -1.8%, APWR -0.7%.

Other news: DLLR -5.3% (announces launch of common stock offering of 5 mln share), CNAM -4.5% (clarifies relationship between Usiminas and Mineracao Usiminas S.A.), KRC -3.7% (announces commencement of 4.5 mln share public offering of common stock), TM -1.6% (Moody's reviews co and subsidiaries for possible downgrade), MXWL -1.4% (files for a $125 mln mixed shelf offering), HMC -1.4% (discloses notice concerning impact of Tohoku Pacific Coast Earthquake; comments on death and injuries; made the decision to extend the suspension of production of finished units).

Analyst comments: LPX -3.3% (downgraded to Neutral from Outperform at Credit Suisse), CVC -2.4% (weakness attributed to tier 1 firm downgrade).

In reaction to disappointing earnings/guidance: AMSC -43.7%, (also downgraded to Market Perform from Strong Buy at Raymond James, downgraded to Hold at Brean Murray, downgraded to Underperform from Buy at Jefferies), MIND -6.5%, ANGO -4.3%, NTE -4.2%, MON -1.1%.

M&A news: CEPH -0.6% (Cephalon's Board of Directors rejects Valeant Pharmaceuticals' unsolicited proposal of $73).

Select AMSC peers and related names ticking lower: CWS -3.3%, ZOLT -1.8%, APWR -0.7%.

Other news: DLLR -5.3% (announces launch of common stock offering of 5 mln share), CNAM -4.5% (clarifies relationship between Usiminas and Mineracao Usiminas S.A.), KRC -3.7% (announces commencement of 4.5 mln share public offering of common stock), TM -1.6% (Moody's reviews co and subsidiaries for possible downgrade), MXWL -1.4% (files for a $125 mln mixed shelf offering), HMC -1.4% (discloses notice concerning impact of Tohoku Pacific Coast Earthquake; comments on death and injuries; made the decision to extend the suspension of production of finished units).

Analyst comments: LPX -3.3% (downgraded to Neutral from Outperform at Credit Suisse), CVC -2.4% (weakness attributed to tier 1 firm downgrade).

Abandon Reason and Logic

By Rev Shark

RealMoney.com Contributor

4/6/2011 8:31 AM EDT

More is better and too much is never enough.

-- Luella Bartley

In the early going, the indications are pointing to a strong open. Oil and gold are up, the dollar is weak and citing rising risks, Moody's has cut the credit ratings on seven Portuguese banks, so I'm a bit uncertain about what is prompting the strong buying action. German economic reports were pretty good and Reuters reports that the early strength is due to "optimism for economic recovery and mergers-and-acquisition activity." That is probably as good of an explanation as any, but trying to navigate this market based on headline news is a sure way to end up confused.

The biggest trap for the bears recently has been trying to anticipate a market reversal based on negative headlines. Higher oil, the European debt issues, lousy home sales, the budget impasses, the Japanese earthquake and so on have been shrugged off by this market. There are any number of good excuses for the market to pull back, but so far, they just haven't mattered. One of these days the market will correct and the explanations for it will be easy to find. But this morning the mood is very positive once again.

We saw a couple negative developments yesterday -- particularly the poor close after strength at midday and the breakout of gold on a weaker dollar. That is not action that is normally associated with an uptrending market.

On the other hand, the flat action of the last few days has helped to ease the overbought technical conditions and the mergers-and-acquisition talk is helping the mood. In addition, a slew of market players are once again anxious to try to call a top in this market. You would think they have learned their lesson after the endless short squeezes and one-way moves we have seen over the past couple years. But for many folks it is just impossible to resist the temptation to try to catch market turns. It has been a horrible strategy for the bearishly inclined, but many are pathologically driven to keep on trying until they finally have some success.

Of course, these one-way markets aren't all that easy for bulls either -- particularly for those who take profits into strength. There are so few opportunities to reload on weakness that it is impossible not to be underinvested if you tend to lock in profits in a systematic way.

I keep repeating the same advice, which is to avoid trying to anticipate a market turn. Stay with the trend as long as you can even, if it doesn't feel like it can keep on going. Trying to apply reason and logic in the face of this sort of momentum will leave you very frustrated.

If you don't trust this market, then the way to deal with it is to trade very short term and keep trying to knock out some fast trades. Building big, longer-term positions is quite difficult in this environment since so many names have become extended. And, of course, shorting is just plain painful.

We'll see if the bears try to fade this strong open, but the bulls have obviously caught them by surprise once again. Gold is the top sector on my watch list.

By Rev Shark

RealMoney.com Contributor

4/6/2011 8:31 AM EDT

More is better and too much is never enough.

-- Luella Bartley

In the early going, the indications are pointing to a strong open. Oil and gold are up, the dollar is weak and citing rising risks, Moody's has cut the credit ratings on seven Portuguese banks, so I'm a bit uncertain about what is prompting the strong buying action. German economic reports were pretty good and Reuters reports that the early strength is due to "optimism for economic recovery and mergers-and-acquisition activity." That is probably as good of an explanation as any, but trying to navigate this market based on headline news is a sure way to end up confused.

The biggest trap for the bears recently has been trying to anticipate a market reversal based on negative headlines. Higher oil, the European debt issues, lousy home sales, the budget impasses, the Japanese earthquake and so on have been shrugged off by this market. There are any number of good excuses for the market to pull back, but so far, they just haven't mattered. One of these days the market will correct and the explanations for it will be easy to find. But this morning the mood is very positive once again.

We saw a couple negative developments yesterday -- particularly the poor close after strength at midday and the breakout of gold on a weaker dollar. That is not action that is normally associated with an uptrending market.

On the other hand, the flat action of the last few days has helped to ease the overbought technical conditions and the mergers-and-acquisition talk is helping the mood. In addition, a slew of market players are once again anxious to try to call a top in this market. You would think they have learned their lesson after the endless short squeezes and one-way moves we have seen over the past couple years. But for many folks it is just impossible to resist the temptation to try to catch market turns. It has been a horrible strategy for the bearishly inclined, but many are pathologically driven to keep on trying until they finally have some success.

Of course, these one-way markets aren't all that easy for bulls either -- particularly for those who take profits into strength. There are so few opportunities to reload on weakness that it is impossible not to be underinvested if you tend to lock in profits in a systematic way.

I keep repeating the same advice, which is to avoid trying to anticipate a market turn. Stay with the trend as long as you can even, if it doesn't feel like it can keep on going. Trying to apply reason and logic in the face of this sort of momentum will leave you very frustrated.

If you don't trust this market, then the way to deal with it is to trade very short term and keep trying to knock out some fast trades. Building big, longer-term positions is quite difficult in this environment since so many names have become extended. And, of course, shorting is just plain painful.

We'll see if the bears try to fade this strong open, but the bulls have obviously caught them by surprise once again. Gold is the top sector on my watch list.

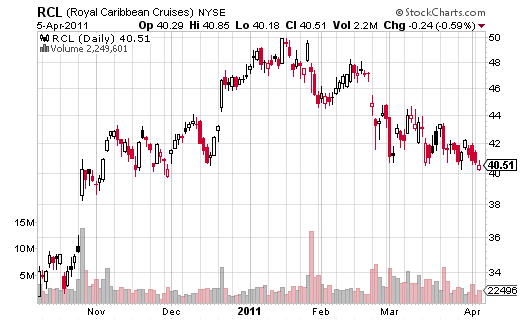

Credit Suisse analüütikud on täna väljas positiivse reitingumuutusega Royal Caribbean Cruises (RCL) kohta.

Credit Suisse tõstab RCL reitingu „hoia“ pealt „osta“ peale ja hinnasihi $44,70 pealt $55,00 peale.

Royal Caribbean is the second-largest cruise vacation company, operating combined 40 ships with 92,300 berths under five core brands including Royal Caribbean, Celebrity, Pullmantur, Azamara Cruises and CDF Croisieres de France. RCL has 3 vessels with an anticipated cost of approximately $2.4bn under construction, which are expected to be placed into service through 2014, with an option for another ship in 2015.

Royal Caribbean on suuruselt teine kruiisilaevade firma, mis tegutseb 40 laevaga viie erineva kaubamärgi all. Ettevõttel on ka kolm laeva ehitamisel, mis peaksid kasutusele tulema 2014. aastal.

Investment Case: While the new cruise cycle is still in its early innings, investing in these stocks requires a view that industry pricing power will continue to recover in the face of a still sluggish global economy. We believe RCL is well-positioned to benefit from one of the most attractive and youngest fleets in the industry, strong relative earnings leverage (1% in net yield adds 7.3% to 2011 EPS versus 5.8% for CCL), disciplined fuel hedging strategies, and balance sheet deleveraging initiatives, which should allow it to generate earnings power above prior peak levels during the next few years. In addition, slowing supply growth and a better commitment to expanding returns over cost of capital should further assist in driving increased long-term earnings power.

Analüütikud ütlevad, et kuigi uus tsükkel on veel üsna varajases järgus, siis antud sektorisse investeerimisel tuleb arvesse võtta, et tööstuse maksejõulisus on jätkuvalt vaatamata nõrgale majandusele paranemas. Analüütikud usuvad, et just RCL on esmane kasusaaja, kuna on üks uuema ja uhkema laevastikuga firmasid antud sektoris ja lisaks sellele on ettevõttel distsiplineeritud kütuseriski maandamise strateegia ning laenukoorma vähendamine lubab firmal järgnevate aastate jooksul kasumit genereerida.

Tegemist pole väga tugeva calliga, aga kuna reitingumuutus tuleb Credit Suisse`lt, siis usun, et turu toetusel tänast ostusoovitust ka märgatakse. Firma tegutseb väga volatiilses sektoris ja kuna ettevõtte konkurent CCL kärpis hiljuti ka oma 2011. aasta prognoose, siis võidetakse antud calli kasutada ka positsioonist väljumiseks.

Hetkel kaupleb aktsia eelturul 1,95% plusspoolel ($41,30)

Credit Suisse tõstab RCL reitingu „hoia“ pealt „osta“ peale ja hinnasihi $44,70 pealt $55,00 peale.

Royal Caribbean is the second-largest cruise vacation company, operating combined 40 ships with 92,300 berths under five core brands including Royal Caribbean, Celebrity, Pullmantur, Azamara Cruises and CDF Croisieres de France. RCL has 3 vessels with an anticipated cost of approximately $2.4bn under construction, which are expected to be placed into service through 2014, with an option for another ship in 2015.

Royal Caribbean on suuruselt teine kruiisilaevade firma, mis tegutseb 40 laevaga viie erineva kaubamärgi all. Ettevõttel on ka kolm laeva ehitamisel, mis peaksid kasutusele tulema 2014. aastal.

Investment Case: While the new cruise cycle is still in its early innings, investing in these stocks requires a view that industry pricing power will continue to recover in the face of a still sluggish global economy. We believe RCL is well-positioned to benefit from one of the most attractive and youngest fleets in the industry, strong relative earnings leverage (1% in net yield adds 7.3% to 2011 EPS versus 5.8% for CCL), disciplined fuel hedging strategies, and balance sheet deleveraging initiatives, which should allow it to generate earnings power above prior peak levels during the next few years. In addition, slowing supply growth and a better commitment to expanding returns over cost of capital should further assist in driving increased long-term earnings power.

Analüütikud ütlevad, et kuigi uus tsükkel on veel üsna varajases järgus, siis antud sektorisse investeerimisel tuleb arvesse võtta, et tööstuse maksejõulisus on jätkuvalt vaatamata nõrgale majandusele paranemas. Analüütikud usuvad, et just RCL on esmane kasusaaja, kuna on üks uuema ja uhkema laevastikuga firmasid antud sektoris ja lisaks sellele on ettevõttel distsiplineeritud kütuseriski maandamise strateegia ning laenukoorma vähendamine lubab firmal järgnevate aastate jooksul kasumit genereerida.

Tegemist pole väga tugeva calliga, aga kuna reitingumuutus tuleb Credit Suisse`lt, siis usun, et turu toetusel tänast ostusoovitust ka märgatakse. Firma tegutseb väga volatiilses sektoris ja kuna ettevõtte konkurent CCL kärpis hiljuti ka oma 2011. aasta prognoose, siis võidetakse antud calli kasutada ka positsioonist väljumiseks.

Hetkel kaupleb aktsia eelturul 1,95% plusspoolel ($41,30)

Eile kasumihoiatuse andnud AMSC on hea näide sellest, mis võib juhtuda, kui lõviosa ettevõtte käibest sõltub ühest kliendist. Firma oli sunnitud oma prognoose märkimisväärselt kärpima, kuna AMSC klient, Hiina päritolu tuuleturbiine tootev firma Sinovel, peatas eelnevalt tellitud tarned. Sinovelilt tuleb AMSC-le 75% käibest ning on ütlematagi selge, et selline sündmuste käik on ettevõttele suur löök.

AMSC kaupleb praegu 48% miinuspoolel ning tsiteerides Business Insiderit, ei tasu neil ( ilmselt silmas peetud eelkõige investoreid), kes täna just söönud on, firma aktsiahinda täna vaadata.

AMSC kaupleb praegu 48% miinuspoolel ning tsiteerides Business Insiderit, ei tasu neil ( ilmselt silmas peetud eelkõige investoreid), kes täna just söönud on, firma aktsiahinda täna vaadata.

Euro on enne homset Euroopa keskpanga intressimäära otsust rallimas, jõudes uude 15 kuu tippu $1,4338 juures.

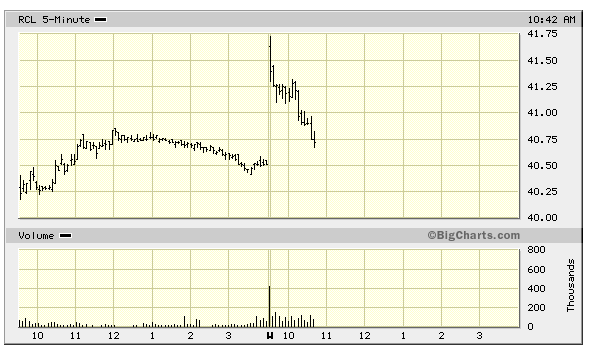

Kahjuks osutus RCL-i puhul mu hommikune kartus täna õigeks ning Credit Suisse upgrade`i kasutati pigem müügiks. Kui eelturul oli näha mõningast ostuhuvi ja aktsia kauples enne avanemist juba $41,70 kandis (+3%), siis peale avanemist asendus ostuhuvi kiirelt müügisurvega ning aktsia on järjekindlalt alla müüdud. Hetkel kaupleb RCL $40,75 kandis ehk 0,6% plusspoolel.

The Fed purchased $1.97 bln of 2028-2041 maturities through Permanent Open Market Operations as dealers looked to put back $7.86 bln

Portugal needs EU financing, finance minister tells newspaper

Ja nüüd siis suuremad pealkirjad ka väljas:

Portugal's Socrates asked EU for financial assistance - Bloomberg TV

Portugal's Socrates asked EU for financial assistance - Bloomberg TV

Kuna Portugalis on peaminister tagasiastunud ja valitsus vahetub, siis ei ole veel selge, kes ja kuidas päästeplaani vastu võtab:

It was not immediately clear what form a request would take, but the outgoing government has previously said that it did not have the political authority to negotiate a rescue agreement to received funds for the European financial stability facility, the EU’s bail-out fund. (FT link)

It was not immediately clear what form a request would take, but the outgoing government has previously said that it did not have the political authority to negotiate a rescue agreement to received funds for the European financial stability facility, the EU’s bail-out fund. (FT link)

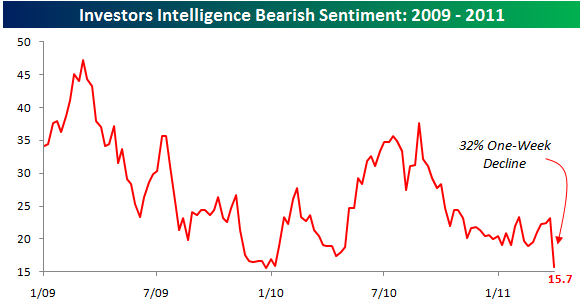

Järgmisel nädalal avab mitteametlikult 1Q11 tulemustehooaja Alcoa. Tänane Investors Intelligence küsitlus näitab, et negatiivseid üllatusi ootavad ettevõtetelt väga vähesed: