Liikumised jäid eile turul suhteliselt tagasihoidlikuks. Stoxx 600 lõpetas 0,2% kõrgemal, S&P 500 aga 0,1% plussis, kui ühest küljest suutis Hispaania müüa soovitust suuremas mahus võlakirjasid ning seda varasemast madalamate laenukulude juures (pisut kõrgemad siiski eelmise päeva sulgemistasemest), teisalt aga jäädi tõenäoliselt ettevaatlikuks enne tänast USA tööjõuraportit. Midagi uut Ben Bernanke kõne eelarvekomitee ees ei sisaldanud, kandes sarnaselt negatiivse alatooniga sõnumit USA majanduse kohta nagu möödunud nädala FOMC intressimäära otsuse järel. Ühtlasi toonitas ta vajadust tegeleda riigi fiskaalsete probleemidega.

“…over the past few months, indicators of spending, production, and job-market activity have shown some signs of improvement…but the sluggish expansion has left the economy vulnerable to shocks,”

Täna avaldatakse mitmel pool Euroopas teenindussektori jaanuari PMI indekseid…eurotsooni oma kell 11.00, Suurbritannia oma kell 11.28. Euroopa statistikast avalikustatakse lisaks kell 12.00 eurotsooni detsembri jaemüügi muutus. Olulisem makro jääb USA poolele, kus kell 15.30 raporteeritakse jaanuaris loodud töökohtade arv (ootus 155K vs 200k detsembris) ning töötusemäär. Kell 17.00 oodatakse teenindussektori jaanuari ISM indeksit ja detsembri tehaste tellimuste muutust.

USA indeksite futuurid kauplevad hetkel nullis.

Hiina non-manufacturing PMI oli jaanuaris 52,9 ehk veidi halvem kui detsembri 56,0. Samas HSBC koostatav PMI indeks püsis 52,5 punktil (dets 52,5).

Prantsusmaa teenindussektori PMI 52,3 vs oodatud 51,7 (dets 51,7), Itaalia 44,8 vs oodatud 45,1 (dets 44,5), Hispaania 46,1 vs oodatud 43,0 (dets 42,1), Saksamaa 53,7 vs oodatud 54,5 (dets 54,5)

Eurotsooni teenindussektori PMI 50,4 vs oodatud 50,5 ning 50,5 detsembris.

UK teenindussektori PMI sarnaselt töötlevale tööstusele tublisti üle ootuste ning kõrgeim näit alates märtsist. Jaanuari PMI 56,0 vs oodatud 53,5 (dets 54,0). Markiti sõnul on jaanuari statistika viitamas majanduslanguse ühe vähenevale tõenäosusele.

EMU PMI detsembris 48,8?

Mis see nüüd siis tähendab - Euroopa pidi ju juba raudkindlalt recessionis olema? USA-s ei tulnud ja kas nüüd siis ka Euroopa osas täielik petmine? Mis toimub?

KES VASTUTAB? :-)

pops

EMU PMI detsembris 48,8?

jah, see vist revideeriti madalamale. Bloomberg igatahes seda ei kajastanud.

Hungarian flag-carrier Malev announced on Friday that it had stopped operating because its liquidity situation has become unsustainable and all its flights had been grounded as of 0500 GMT on Friday.

The airline had been placed under extraordinary protection from creditors and a receiver was appointed earlier this week.

The airline had been placed under extraordinary protection from creditors and a receiver was appointed earlier this week.

113366

Hungarian flag-carrier Malev announced on Friday that it had stopped operating because its liquidity situation has become unsustainable and all its flights had been grounded as of 0500 GMT on Friday.

The airline had been placed under extraordinary protection from creditors and a receiver was appointed earlier this week.

Isegi sellega korra Budapestist Bucharesti lennatud. Lennusaatjad olid kõik mehed ja sellised tahumatu olekuga karvased vennad. Ei tea, aga millegipärast tuli Borat meelde...

Eurotsooni jaemüük vähenes detsembris aastaga -1,6% ehk oodatud -1,3%st pisut enam. Novembri näitaja revideeriti aga -2,5% pealt -1,5%le.

Aeterna Zentaris reports 'positive' updated Phase 1 trial results for AEZS-108 in castration- and taxane-resistant prostate cancer

Co reported 'positive' updated results for the Phase 1 portion of its ongoing Phase 1/2 study in castration- and taxane-resistant prostate cancer (CRPC) with AEZS-108 (zoptarelin doxorubicin), the co's targeted cytotoxic luteinizing hormone-releasing hormone analog. Data showed that AEZS-108 was well tolerated and demonstrated early evidence of antitumor activity in men with CRPC.

Co reported 'positive' updated results for the Phase 1 portion of its ongoing Phase 1/2 study in castration- and taxane-resistant prostate cancer (CRPC) with AEZS-108 (zoptarelin doxorubicin), the co's targeted cytotoxic luteinizing hormone-releasing hormone analog. Data showed that AEZS-108 was well tolerated and demonstrated early evidence of antitumor activity in men with CRPC.

Gapping down

In reaction to disappointing earnings/guidance: THQI -25% (also announces business realignment), APKT -13.7% (also downgraded to Hold at Needham, downgraded to Underperform from Neutral at Mizuho), EW -8.3% (also downgraded to Market Perform from Outperform at Wells Fargo), EL -7.2%, ATML -6.9%, COLM -5%, WYNN -4%, ARR -2.8% (announces estimated Q4 results and 22 mln share stock offering), CYMI -2.2%, VRTX -2% (also downgraded to Neutral from Buy at Goldman, downgraded to Neutral from Outperform at Cowen), HAYN -1% (ticking lower), CAVM -0.9%, (light volume).

Other news: MNKD -8.9% (prices 31.25 mln units consisting of 1 share of common stock and a warrant to purchase 0.6 of a share of its common stock at $2.40 per unit), NBG -7.5% (still checking, potential weakness on continued Greece rescue plan speculation), BBEP -5% (announces offering of 8 mln common units), PAY -3% (still checking), MGM -0.7% (announced the launch of a proposed amendment to its aggregate $3.5 billion senior credit facilities).

Analyst comments: OPEN -2.3% (downgraded to Hold from Buy at ThinkEquity), RIMM -2% (downgraded to Underperform from Hold at Jefferies), CVC -1.1% (Cablevision downgraded to Underweight from Neutral at JP Morgan), EP -0.6% (downgraded to Neutral from Buy at Citigroup).

In reaction to disappointing earnings/guidance: THQI -25% (also announces business realignment), APKT -13.7% (also downgraded to Hold at Needham, downgraded to Underperform from Neutral at Mizuho), EW -8.3% (also downgraded to Market Perform from Outperform at Wells Fargo), EL -7.2%, ATML -6.9%, COLM -5%, WYNN -4%, ARR -2.8% (announces estimated Q4 results and 22 mln share stock offering), CYMI -2.2%, VRTX -2% (also downgraded to Neutral from Buy at Goldman, downgraded to Neutral from Outperform at Cowen), HAYN -1% (ticking lower), CAVM -0.9%, (light volume).

Other news: MNKD -8.9% (prices 31.25 mln units consisting of 1 share of common stock and a warrant to purchase 0.6 of a share of its common stock at $2.40 per unit), NBG -7.5% (still checking, potential weakness on continued Greece rescue plan speculation), BBEP -5% (announces offering of 8 mln common units), PAY -3% (still checking), MGM -0.7% (announced the launch of a proposed amendment to its aggregate $3.5 billion senior credit facilities).

Analyst comments: OPEN -2.3% (downgraded to Hold from Buy at ThinkEquity), RIMM -2% (downgraded to Underperform from Hold at Jefferies), CVC -1.1% (Cablevision downgraded to Underweight from Neutral at JP Morgan), EP -0.6% (downgraded to Neutral from Buy at Citigroup).

January Nonfarm Payrolls 243K vs 155K Briefing.com consensus; December revised to 203K from 200K

January Nonfarm Private Payrolls 257K vs 168K Briefing.com consensus

January Unemployment 8.3% vs 8.5% Briefing.com consensus; Prior 8.5%

January Hourly Earnings +0.1% vs +0.2% Briefing.com consensus; Prior +0.2%

January Average Workweek 34.5 vs 34.4 Briefing.com consensus; Prior 34.4

January Nonfarm Private Payrolls 257K vs 168K Briefing.com consensus

January Unemployment 8.3% vs 8.5% Briefing.com consensus; Prior 8.5%

January Hourly Earnings +0.1% vs +0.2% Briefing.com consensus; Prior +0.2%

January Average Workweek 34.5 vs 34.4 Briefing.com consensus; Prior 34.4

Gapping up

In reaction to strong earnings/guidance: INFN +17.6%, (also upgraded to Neutral from Underweight at JP Morgan), ZOLT +10.5%, TRMB +10.1%, SIMO +7.9%, TSYS +7.6% (light volume), DRIV +7.5%, ACLS +7.5%, SUN +7.2%, PKI +6.9%, GNW +6.1%, GILD +5.5%, SIMG +5.3%, NSR +4.9%, N +4%, TSN +3.1%, BT +3.1%, WY +3.1%, TTWO +1.8%, AXL +1.4%, GLW +1.0%, MCHP +0.8%, BEBE +0.4% (light volume), NVLS +0.3%.

M&A related: BRCD +2.9% (Blackstone looking into LBO of BRCD, according to reports).

A few financial related names showing modest strength: IRE +3.5%, STD +2.9%, CS +2%, BBVA +1.3%, HBC +1.2%, BAC +0.9%, .

Other news: THLD +62.8% (light volume, Threshold Pharma and Merck KGaA announce global agreement to co-develop and commercialize Phase 3 Hypoxia-Targeted drug TH-302), SNE +9.4% (traded higher overseas), GMXR +6.5% (continued strength following yesterday's 60%+ surge higher), IDIX +4.6% (announces removal of the partial clinical hold on HCV Nucleotide Inhibitor, IDX184), IAG +4.4% (declares rare earth inferred resource of 467 million tonnes at a grade of 1.65% TREO), ZNGA +3.5% (continued strength following yesterday's 15% pop higher), SQNM +2.2% (Sequenom study published in Genetics in Medicine demonstrates Sequenom CMM Maternit21 test accurately detects two additional fetal trisomies), ARMH +2.2% (still checking), URBN +2.1% (announced the appointment of Tedford Marlow as Chief Executive Officer, Urban Outfitters Group, upgraded to Buy from Neutral at Janney Mntgmy Scott), MYGN +1.3% (Myriad Genetics Prolaris Test shown to significantly predict biochemical recurrence risk after prostatectomy), AGN +0.9% (positive mention on MadMoney).

Analyst comments: NOV +2.2% (upgraded to Overweight from Equal Weight at Morgan Stanley), DNDN +1.2% (light volume, upgraded to Neutral from Underperform at BofA/Merrill), THOR +0.8% (initiated with a Buy at ThinkEquity).

In reaction to strong earnings/guidance: INFN +17.6%, (also upgraded to Neutral from Underweight at JP Morgan), ZOLT +10.5%, TRMB +10.1%, SIMO +7.9%, TSYS +7.6% (light volume), DRIV +7.5%, ACLS +7.5%, SUN +7.2%, PKI +6.9%, GNW +6.1%, GILD +5.5%, SIMG +5.3%, NSR +4.9%, N +4%, TSN +3.1%, BT +3.1%, WY +3.1%, TTWO +1.8%, AXL +1.4%, GLW +1.0%, MCHP +0.8%, BEBE +0.4% (light volume), NVLS +0.3%.

M&A related: BRCD +2.9% (Blackstone looking into LBO of BRCD, according to reports).

A few financial related names showing modest strength: IRE +3.5%, STD +2.9%, CS +2%, BBVA +1.3%, HBC +1.2%, BAC +0.9%, .

Other news: THLD +62.8% (light volume, Threshold Pharma and Merck KGaA announce global agreement to co-develop and commercialize Phase 3 Hypoxia-Targeted drug TH-302), SNE +9.4% (traded higher overseas), GMXR +6.5% (continued strength following yesterday's 60%+ surge higher), IDIX +4.6% (announces removal of the partial clinical hold on HCV Nucleotide Inhibitor, IDX184), IAG +4.4% (declares rare earth inferred resource of 467 million tonnes at a grade of 1.65% TREO), ZNGA +3.5% (continued strength following yesterday's 15% pop higher), SQNM +2.2% (Sequenom study published in Genetics in Medicine demonstrates Sequenom CMM Maternit21 test accurately detects two additional fetal trisomies), ARMH +2.2% (still checking), URBN +2.1% (announced the appointment of Tedford Marlow as Chief Executive Officer, Urban Outfitters Group, upgraded to Buy from Neutral at Janney Mntgmy Scott), MYGN +1.3% (Myriad Genetics Prolaris Test shown to significantly predict biochemical recurrence risk after prostatectomy), AGN +0.9% (positive mention on MadMoney).

Analyst comments: NOV +2.2% (upgraded to Overweight from Equal Weight at Morgan Stanley), DNDN +1.2% (light volume, upgraded to Neutral from Underperform at BofA/Merrill), THOR +0.8% (initiated with a Buy at ThinkEquity).

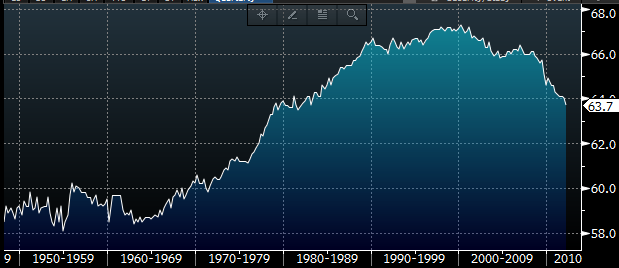

Labour participation rate tuli kuuga taas 0,3 protsendipunkti võrra alla, mille arvelt siis ka töötusemäär parem

Huvitav, mille arvelt see tuleb? Kas lootusetute osakaal tõusnud? Või on sõjajärgsete beebibuumerite pensionile jäämine suurenenud? Või midagi muud? Kui te leiate sellele kusagilt viiteid, siis oleksin tänulik.

Eks põhjuseid ole palju ja siin artiklis on nendest mõned välja toodud. Huvitaval kombel on langus kirjutatud viimasel ajal just mustanahaliste naiste arvele. Via CEPR

The drop in participation was entirely among women and especially black women. (Among married women, employment rose by 194,000, so this was not a case of women as second earners dropping out of the labor force.) Participation numbers among white women fell by 199,000, a decline of 0.2 percentage points. The drop among black women was 164,000, a drop of 1.2 percentage points. These monthly numbers are highly erratic, and it is likely that at least part of this drop will be reversed in future months. Nonetheless there had been a trend of declining participation rates among both white and black women even prior to the November plunge. This suggests that there is a real issue of women losing access to jobs; although the December figures may show some reversal.

The drop in participation was entirely among women and especially black women. (Among married women, employment rose by 194,000, so this was not a case of women as second earners dropping out of the labor force.) Participation numbers among white women fell by 199,000, a decline of 0.2 percentage points. The drop among black women was 164,000, a drop of 1.2 percentage points. These monthly numbers are highly erratic, and it is likely that at least part of this drop will be reversed in future months. Nonetheless there had been a trend of declining participation rates among both white and black women even prior to the November plunge. This suggests that there is a real issue of women losing access to jobs; although the December figures may show some reversal.