Teatavasti andis jalatsitetootja CROX eile õhtul kasumihoiatuse ja selliste uudiste eest ei jäeta aktsiat karistamata. Eile õhtul kukkus aktsia alla $ 17 taseme ja täna eelturul on kauplemas $ 17,60 kandis ehk 33,5% miinuspoolel.

Piper Jeffray on täna aktsiat kaitsmas:

We believe GM rate was pressured due to channel mix in the Americas and pricing pressure in Europe. The company also announced wholesale bookings as of quarter end had risen 30% y/y, which indicates retailer and consumer demand remains robust despite macroeconomic headwinds. We have reduced our price target from $38 to $30 based on our revised estimates, but believe CROX can continue to generate 20%-plus EPS growth over the next several years through strong top line growth and margin expansion. Reiterate Overweight rating as CROX continues its transformation into a diversified, global footwear brand.

Analüütikud ütlevad, et brutokasumimarginaal vähenes Euroopas aset leidnud hinnasurve tõttu, aga samas teatas firma hulgimüügi tellimustest, mis kvartali lõpuks olid y/y tõusunud 30%. Analüütikute arvates näitab see ilmekalt, et vaatamata halvenevale makrokeskkonnale on tarbija nõudlus endiselt tugev. Analüütikud langetavad hinnasihi $ 38 pealt $ 30 peale, aga kinnitavad oma Osta soovitust, sest on veendunud, et CROX on järgnevate aastate jooksul suuteline 20%-ks kasumikasvuks.

CROX võiks meile täna väikese põrke pakkuda, aga nagu selliste olukordade puhul ikka, siis ettevaatlikus ja konservatiivsus tuleb igati kasuks.

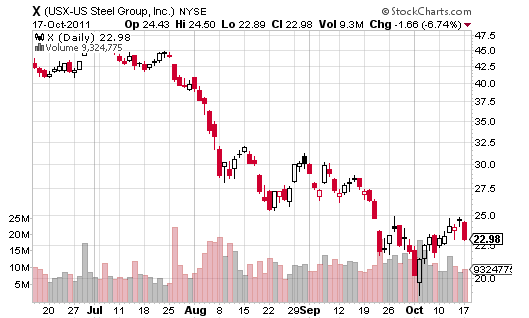

Goldman Sachs alandab täna US Steel (X) reitingu Hoia pealt Müü peale ja hinnasihi $ 30 pealt $ 20 peale ning tõstab AK Steel (AKS) reitingu Müü pealt Hoia peale koos $ 8 hinnasihiga.

We are downgrading US Steel to Sell from Neutral with a target price of $20 (down from $30) as we believe that 2H-2011 consensus estimates for X are too high and company’s qualitative guidance for 4Q will disappoint the market, driving the stock down. Additionally, 2012 Street estimates look too optimistic and we expect these to come down over coming months. In our view, X’s current share price does not appear to fully reflect the near- term downward pressure on steel prices as supply continues to exceed demand in the US. Also, the market is not fully accounting for the continued weakness in European markets, in our view. Further, the recent downward move in global iron ore prices could diminish investors’ positive perception of US Steel’s vertical integration. And lastly, the pension headwinds next year for US Steel would be another overhang.

Analüütikud usuvad, et konsenuse ootused X-i teise poolaasta tulemuste suhtes on liiga optimistlikud ja ei võeta arvesse terasehinna jätkuvat langust. Goldmani arvates kärbitakse lähiajal ilmselt prognoose ning X aktsiasse pole seda veel sisse arvestatud.

Upgrading AKS to Neutral post significant underperformance We are upgrading AKS to Neutral from Sell as we do not see more downside from current levels. Although the economic benefits of the recently announced investments in the upstream supply chain are a few years out, investors’ perception of AKS as a non-integrated and thus

disadvantaged steel producer should diminish, removing one of the overhangs on the stock. Although AKS faces the same weak supply- demand fundamentals in flat steel as X, we believe that 2H earnings expectations for AKS are more realistic and are priced in.

Vastupidselt X-le on analüütikute arvates AKS-i aktsiahinda juba halvad uudised sisse arvestatud ja ootused teise poolaasta tulemuste suhtes on reaalsed.

Mõlemad firmad peaks oma kvartalitulemused teatama 25. oktoobril, enne turu avanemist.

We are downgrading US Steel to Sell from Neutral with a target price of $20 (down from $30) as we believe that 2H-2011 consensus estimates for X are too high and company’s qualitative guidance for 4Q will disappoint the market, driving the stock down. Additionally, 2012 Street estimates look too optimistic and we expect these to come down over coming months. In our view, X’s current share price does not appear to fully reflect the near- term downward pressure on steel prices as supply continues to exceed demand in the US. Also, the market is not fully accounting for the continued weakness in European markets, in our view. Further, the recent downward move in global iron ore prices could diminish investors’ positive perception of US Steel’s vertical integration. And lastly, the pension headwinds next year for US Steel would be another overhang.

Analüütikud usuvad, et konsenuse ootused X-i teise poolaasta tulemuste suhtes on liiga optimistlikud ja ei võeta arvesse terasehinna jätkuvat langust. Goldmani arvates kärbitakse lähiajal ilmselt prognoose ning X aktsiasse pole seda veel sisse arvestatud.

Upgrading AKS to Neutral post significant underperformance We are upgrading AKS to Neutral from Sell as we do not see more downside from current levels. Although the economic benefits of the recently announced investments in the upstream supply chain are a few years out, investors’ perception of AKS as a non-integrated and thus

disadvantaged steel producer should diminish, removing one of the overhangs on the stock. Although AKS faces the same weak supply- demand fundamentals in flat steel as X, we believe that 2H earnings expectations for AKS are more realistic and are priced in.

Vastupidselt X-le on analüütikute arvates AKS-i aktsiahinda juba halvad uudised sisse arvestatud ja ootused teise poolaasta tulemuste suhtes on reaalsed.

Mõlemad firmad peaks oma kvartalitulemused teatama 25. oktoobril, enne turu avanemist.

Oleme ka seekord pannud kokku tabeli erinevatest ettevõtetest, mille kvartalitulemusi näeb siin.

Bank of America on Conference Call- says modeling for a 2.6% decline in housing prices by the end of 2012

Eile ilmus Investors.com saidil uudis USA kulude kärpimise teemal. Nimelt on vabariiklased lubanud alates jaanuarist, kui esindajatekojas enamus võeti, teha korralikke kärpeid keskvalitsuse kuludes, kuid nagu välja tuleb, siis siiani on kulutused jätkuvalt kasvamas.

In the first nine months of this year, federal spending was $120 billion higher than in the same period in 2010, the data show. That's an increase of almost 5%. And deficits during this time were $23.5 billion higher.

These spending hikes haven't stopped many analysts from claiming that the country is in an age of budget austerity, one that's hurting economic growth.

A July article in USA Today, for example, claimed that "Already in 2011, softer government spending has sapped growth."

Jared Bernstein, former chief economic adviser to Vice President Biden, wrote over the summer that "government spending cutbacks have been a large drag on growth in recent quarters and have led to sharp losses in state and local employment."

Economist and New York Times columnist Paul Krugman argued in September that "the turn toward austerity (is) a major factor in our growth slowdown."

If government spending is related to growth, as these and others claim, then the economy presumably should be growing faster, not slower, given the current higher rates of federal outlays.

China rare earth production halted, according to Rare Metal blog

Turg on ilmselt hoogu juurde saamas The Guardian`s ilmunud artiklist, kus kirjutatakse, et Saksamaa ja Prantsusmaa on valmis 2 triljoni euro suurust päästefondi kinnitama.

Selle peale võttis isegi CROX suuna üles :)

CROX on ikkagi suhteliselt õnnetu olnud täna terve päeva ja peale eelturul tehtud põrget jõudu paraku enam rohkemaks polnud.

Crocs jalanõudest rääkides meenub Crocsi viimane innovatsioon - golfisandaalid. Ju siis on lubatud, kuna 2012-2016 reeglites pole nad keelatud.

Olenemata kuivõrd koledad nad ei paista, ka mitte golfijalanõuna, on kasutajad rahul nende mugavuse ja praktilisusega. Haiglates näiteks kasutatakse seepärast, et ta ei tekita staatilist.

Aga nad on koledad kui krokodillid öös.

Olenemata kuivõrd koledad nad ei paista, ka mitte golfijalanõuna, on kasutajad rahul nende mugavuse ja praktilisusega. Haiglates näiteks kasutatakse seepärast, et ta ei tekita staatilist.

Aga nad on koledad kui krokodillid öös.

Market dropping as headlines crossing wires puting Guardian story in doubt

INTC teatas oodatust parematest tulemustest:

Intel prelim $0.69 vs $0.63 Capital IQ Consensus Estimate; revs $14.2 bln vs $13.84 bln Capital IQ Consensus Estimate

Aktsia järelturul kauplemas 4,6% plusspoolel, $ 24,35 kandis.

Intel prelim $0.69 vs $0.63 Capital IQ Consensus Estimate; revs $14.2 bln vs $13.84 bln Capital IQ Consensus Estimate

Aktsia järelturul kauplemas 4,6% plusspoolel, $ 24,35 kandis.

AAPL:

Apple prelim $7.05 vs $7.27 Capital IQ Consensus Estimate; revs $28.27 bln vs $29.28 bln Capital IQ Consensus Estimate

Apple sees Q1 EPS of $9.30 vs $8.97 Capital IQ Consensus Estimate; sees revs $37.0 bln vs $36.64 bln Capital IQ Consensus Estimate

Tulemused alla ootuste, aga prognoosid annab kõrgemad, mis pole AAPL-i puhul väga tavapärane.

Aktsia kauplemas 5% miinuspoolel, $ 400 kandis.

Apple prelim $7.05 vs $7.27 Capital IQ Consensus Estimate; revs $28.27 bln vs $29.28 bln Capital IQ Consensus Estimate

Apple sees Q1 EPS of $9.30 vs $8.97 Capital IQ Consensus Estimate; sees revs $37.0 bln vs $36.64 bln Capital IQ Consensus Estimate

Tulemused alla ootuste, aga prognoosid annab kõrgemad, mis pole AAPL-i puhul väga tavapärane.

Aktsia kauplemas 5% miinuspoolel, $ 400 kandis.

AAPL tulemused alla ootuste pole tavapärane, eelmisel aastal mälu pealt guidis ka üles

Nelli Janson

AAPL:

[/i]

Tulemused alla ootuste, aga prognoosid annab kõrgemad, mis pole AAPL-i puhul väga tavapärane.

Huh? AAPL on siiamaani väga konservatiivse guidancega olnud.

Analüütikutel keeruline, enam ei saa järgmise kvartali ootusi arvutada guidance x 1.2 vms. Ja lisaks küsimus, et mis muutusi siis Cook veel teeb. Mõni suur ost äkki?

Fondijuhid igatahes lasevad püksid täis, nende parim safe haven rikuti ära. AAPL on kuni järgmiste tulemusteni guilty until proven innocent.