Ohhoo...saab ka ilma Elionita Euroopa CNBC'd vaadata http://www.rentadrone.tv/cnbc-live-stream/

Lõppenud aasta enamus fondidele midagi rõõmustavat endaga kaasa ei toonud, kuna rekordarv firmasid pidi oma uksed hoopis kinni panema. Teisalt võib Business Insideri vahendusel lugeda, et leidus ka piisavalt neid fonde, kelle tootlusega võivad investorid igati rahule jääda ja HSBC on kokku pannud ka 15 parima tootlusega fondi aastal 2011. Olgu öeldud, et hinnatud on riskifondide all tegutsevaid fonde eraldi.

Esikoha saavutas Renaissance Institutional Equities LP (B), mis on osa Renaissance Technologiest ja möödunud aastal pakkus investoritele 34,66%-se tootluse.Hallatav raha $ 240 miljonit ja fondihalduriks James Simons.

Teiste fondide kohta saab lugeda siin.

Esikoha saavutas Renaissance Institutional Equities LP (B), mis on osa Renaissance Technologiest ja möödunud aastal pakkus investoritele 34,66%-se tootluse.Hallatav raha $ 240 miljonit ja fondihalduriks James Simons.

Teiste fondide kohta saab lugeda siin.

Karum6mm

Mõlemas kanalis näitab ju näiteks Marc Faber'it, kes on igati kõrge meelelahutusliku väärtusega tegelane, kelle jutus kipub aeg-ajalt ka päris suur iva olema. Ei tasu unustada, et onu oli üks esialgsetest BSD-dest. ;)

Marc Faberi puhul ei pea õnneks muretsema, et mõni tema intervjuudest nägemata jääb, kuna muu meedia korjab neid päris usinalt üles

Tänasel Prantsuse oksjonil müüdi suurima mahuga 10a võlakirju (kokku 4 miljardi euro eest). Yieldiks kujunes 3,29% vs 3,18% eelmisel sarnasel oksjonil oktoobris ning bid to cover 1,643 vs 3,046 eelmisel korral.

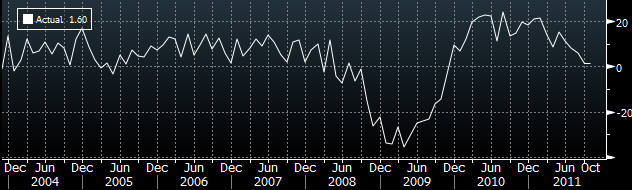

Käes on küll juba uus aasta ja seetõttu ei pruugi nii vana info nagu eurotsooni oktoobri tehaste tellimuste muutus huvi pakkuda, kuid neljanda kvartali SKT näitu oodates ei olnud oktoober tellimuste poolel paljulubav. Tellimused kasvasid aasta baasil 1,6%, mis tähendab püsimist samal tasemel võrreldes septembriga. Analüütikud olid oodanud aga ligi kaks korda kiiremat kasvu

Eile andis Seagate Technology (STX) peale turu sulgumist eelteate oma neljanda kvartali tulemuste kohta, mis oli märkimisväärselt parem kui viimane prognoos. Tänu sellele kauples aktsia järelturul ka 7% kõrgemal.

Citi analüütikud kinnitava oma Osta soovitust ja tõstavad STX hinnasihi $ 26 pealt $ 28 peale.

Kuigi nad on STX suhtes positiivsed, siis soosivad analüütikud pigem Western Digital (WDC)-d

Favoring WDC — While we see meaningful upside to both HDD stocks (STX and WDC) during the next several months, we have a bias towards WDC at current levelsgiven that: 1) the completion of the HGST merger remains a significant catalyst nearterm, and 2) we see disproportionate upside to consensus units and gross margin estimates as the company’s output is recovering quicker than expected, while thepotential earnings accretion from HGST is underappreciated.

Ehk analüütikute arvates ei hinda konsensus ettevõtte väljavaadete paranemist piisavalt ja HGST-ga ühinemise protsessi lõpule viimine tähistab analüütikute sõnul samuti olulist katalüsaatorit.

Citil on WDC-le Osta soovitus koos $ 48 hinnasihiga.

Seega võiks STX kõrval ehk täna ka WDC ostuhuvi leida.

Citi analüütikud kinnitava oma Osta soovitust ja tõstavad STX hinnasihi $ 26 pealt $ 28 peale.

Kuigi nad on STX suhtes positiivsed, siis soosivad analüütikud pigem Western Digital (WDC)-d

Favoring WDC — While we see meaningful upside to both HDD stocks (STX and WDC) during the next several months, we have a bias towards WDC at current levelsgiven that: 1) the completion of the HGST merger remains a significant catalyst nearterm, and 2) we see disproportionate upside to consensus units and gross margin estimates as the company’s output is recovering quicker than expected, while thepotential earnings accretion from HGST is underappreciated.

Ehk analüütikute arvates ei hinda konsensus ettevõtte väljavaadete paranemist piisavalt ja HGST-ga ühinemise protsessi lõpule viimine tähistab analüütikute sõnul samuti olulist katalüsaatorit.

Citil on WDC-le Osta soovitus koos $ 48 hinnasihiga.

Seega võiks STX kõrval ehk täna ka WDC ostuhuvi leida.

Morgan Stanley annab vägagi konkreetse prognoosi QE3 kohta ja usub, et uus abiprogramm tuleb suurusjärgus $ 500-750 miljardit märts-juuni vahel.:

The unwind of the negative shocks from Japan’s earthquake and the run-up in energy prices earlier in the year are responsible for the recent run of strong data in the US economy, argues our Chief US Economist Vincent Reinhart in today’s lead piece. Once these tailwinds have played out and a shallow fiscal pothole emerges, growth should slow to around 2% in early 2012. As a result, the Fed will probably mark down its growth and inflation forecasts. The deceleration will likely be enough to convince the FOMC that the downside risks to its dual objectives of maximum employment and stable prices need to be addressed. However, given the ambiguity in the Federal Reserve Act about how to weigh these objectives against each other, disagreement within the FOMC itself about the relative weights and Bernanke’s efforts to create a more democratic process for decision-making, progress on another QE package is likely to be slow and full of compromise. Eventually though, we believe that a package of Treasury and MBS purchases of US$500-750 billion will arrive some time between March and June.

The unwind of the negative shocks from Japan’s earthquake and the run-up in energy prices earlier in the year are responsible for the recent run of strong data in the US economy, argues our Chief US Economist Vincent Reinhart in today’s lead piece. Once these tailwinds have played out and a shallow fiscal pothole emerges, growth should slow to around 2% in early 2012. As a result, the Fed will probably mark down its growth and inflation forecasts. The deceleration will likely be enough to convince the FOMC that the downside risks to its dual objectives of maximum employment and stable prices need to be addressed. However, given the ambiguity in the Federal Reserve Act about how to weigh these objectives against each other, disagreement within the FOMC itself about the relative weights and Bernanke’s efforts to create a more democratic process for decision-making, progress on another QE package is likely to be slow and full of compromise. Eventually though, we believe that a package of Treasury and MBS purchases of US$500-750 billion will arrive some time between March and June.

Nelli Janson

Morgan Stanley annab vägagi konkreetse prognoosi QE3 kohta ja usub, et uus abiprogramm tuleb suurusjärgus $ 500-750 miljardit märts-juuni vahel.:

The unwind of the negative shocks from Japan’s earthquake and the run-up in energy prices earlier in the year are responsible for the recent run of strong data in the US economy, argues our Chief US Economist Vincent Reinhart in today’s lead piece. Once these tailwinds have played out and a shallow fiscal pothole emerges, growth should slow to around 2% in early 2012. As a result, the Fed will probably mark down its growth and inflation forecasts. The deceleration will likely be enough to convince the FOMC that the downside risks to its dual objectives of maximum employment and stable prices need to be addressed. However, given the ambiguity in the Federal Reserve Act about how to weigh these objectives against each other, disagreement within the FOMC itself about the relative weights and Bernanke’s efforts to create a more democratic process for decision-making, progress on another QE package is likely to be slow and full of compromise. Eventually though, we believe that a package of Treasury and MBS purchases of US$500-750 billion will arrive some time between March and June.

Ja mida annab QE3? Ajutist suurt tõusu US and A börsil!

Ei tea, kas Bernanke ei saa aru, et see tema pidev ''ajutine'' asjade lahendamine on pikemas perspektiivis pigem väga kahjulik?

SODA-le hea uudis. KFT ja SODA teatasid, et on sõlminud strateegilise koostööleppe, mille käigus hakatakse kasutama KFT kaubamärgiga erinevaid maitsesiirupeid SODA karboniseeritud jookides.

SodaStream & Kraft Foods (KFT) announced a strategic partnership for the manufacturing, marketing, distribution and sale of KFT branded flavors for use with the SODA soda making system.

This will be the first time that KFT flavors will be available specifically for use in a carbonated beverage.

SODA kaupleb eelturul üle 9% plusspoolel, $ 41 taseme juures.

SodaStream & Kraft Foods (KFT) announced a strategic partnership for the manufacturing, marketing, distribution and sale of KFT branded flavors for use with the SODA soda making system.

This will be the first time that KFT flavors will be available specifically for use in a carbonated beverage.

SODA kaupleb eelturul üle 9% plusspoolel, $ 41 taseme juures.

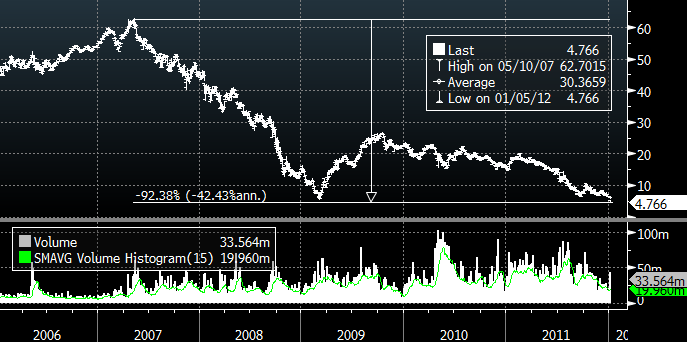

40 miljoni kliendiga ja rohkem kui 20. erinevas riigis tegutsev Itaalia pank Unicredit on 2007. aasta tipust tänaseks kaotanud 92.4% oma väärtusest.

December ADP Employment Change 325K vs 180K Briefing.com consensus

Gapping up

In reaction to strong earnings/guidance/SSS: ZUMZ +12%, OCLR +8.8%, STX +6.4%, ULTA +5%, MON +1.1%, MOS +0.7%.

A few optical related names are modestly higher following OCLR guidance: JDSU +1.6%, FNSR +1.3%.

Other news: GALE +13% (announces investigational new drug approval for phase 2 Trial for NeuVax), SODA +12.6% (SodaStream & Kraft Foods announced a strategic partnership for the manufacturing, marketing, distribution and sale of KFT branded flavors for use with the SODA soda making system), WDC +2.6% (trading higher with STX), IRWD +2.5% (Ironwood Pharmaceuticals and Bionomics announce collaboration, research, and license agreement), MRVL +2.2% (Marvell says Foresight Platform designed into Google TV), ALXN +1% (mentioned positively on MadMoney).

Analyst comments: NOK +3.3% (upgraded to Outperform from Underperform at Credit Suisse), LSI +2.1% (upgraded to Outperform from Neutral at Wedbush).

In reaction to strong earnings/guidance/SSS: ZUMZ +12%, OCLR +8.8%, STX +6.4%, ULTA +5%, MON +1.1%, MOS +0.7%.

A few optical related names are modestly higher following OCLR guidance: JDSU +1.6%, FNSR +1.3%.

Other news: GALE +13% (announces investigational new drug approval for phase 2 Trial for NeuVax), SODA +12.6% (SodaStream & Kraft Foods announced a strategic partnership for the manufacturing, marketing, distribution and sale of KFT branded flavors for use with the SODA soda making system), WDC +2.6% (trading higher with STX), IRWD +2.5% (Ironwood Pharmaceuticals and Bionomics announce collaboration, research, and license agreement), MRVL +2.2% (Marvell says Foresight Platform designed into Google TV), ALXN +1% (mentioned positively on MadMoney).

Analyst comments: NOK +3.3% (upgraded to Outperform from Underperform at Credit Suisse), LSI +2.1% (upgraded to Outperform from Neutral at Wedbush).

Google (GOOG)-i aktsia, mis on viimase kolme kuuga läbi teinud muljetavaldava ligi 40% tõusu ehk rallinud $ 480 pealt $ 670 peale saab täna downgrade`i osaliseks.

Benchmark alandab GOOG-i reitingu Osta pealt Hoia peale koos $ 700 hinnasihiga.

4Q11 data and channel checks indicate strong domestic online advertising but a severe slowdown in Europe. The 1H12 US outlook appears increasingly uncertain with advertisers expressing hesitation. While Google’s stock is up in anticipation of a strong 4Q11, we fear 1H12 may prove disappointing. We trim our estimates and

downgrade Google from Buy to Hold.

Channel checks reveal that European online advertising has dropped from over 20% y/y growth in 1H11 to up only 5% in 4Q11. Europe represents around 35%-40% of Google’s revenue. Google currently has 90% or more search market share in Europe. This dominant position limits the potential for share gains to offset macro headwinds. The 1H12 outlook for Europe is sustained softness.

Peamise murelapsena toovad analüütikud välja Euroopa, kus nähakse kasvu aeglustumist. Nimelt on uuringute põhjal näha, et Euroopa reklaamitulud on oluliselt kahanenud. GOOG käibest moodustab Euroopa ca 35-40% ning on absoluutne turuliider koos 90% turuosaga, mis omakorda seab piirangud ka kahaneva reklaamitulu kompenseerimiseks turuosa võitmise arvelt.

Benchmark alandab GOOG-i reitingu Osta pealt Hoia peale koos $ 700 hinnasihiga.

4Q11 data and channel checks indicate strong domestic online advertising but a severe slowdown in Europe. The 1H12 US outlook appears increasingly uncertain with advertisers expressing hesitation. While Google’s stock is up in anticipation of a strong 4Q11, we fear 1H12 may prove disappointing. We trim our estimates and

downgrade Google from Buy to Hold.

Channel checks reveal that European online advertising has dropped from over 20% y/y growth in 1H11 to up only 5% in 4Q11. Europe represents around 35%-40% of Google’s revenue. Google currently has 90% or more search market share in Europe. This dominant position limits the potential for share gains to offset macro headwinds. The 1H12 outlook for Europe is sustained softness.

Peamise murelapsena toovad analüütikud välja Euroopa, kus nähakse kasvu aeglustumist. Nimelt on uuringute põhjal näha, et Euroopa reklaamitulud on oluliselt kahanenud. GOOG käibest moodustab Euroopa ca 35-40% ning on absoluutne turuliider koos 90% turuosaga, mis omakorda seab piirangud ka kahaneva reklaamitulu kompenseerimiseks turuosa võitmise arvelt.

Continuing Claims falls to 3.595 mln from 3.617 mln

Initial Claims 372K vs 375K Briefing.com consensus; Prior revised to 387K from 381K

Initial Claims 372K vs 375K Briefing.com consensus; Prior revised to 387K from 381K

Gapping down

In reaction to disappointing earnings/guidance/SSS: AEO -14.2%, PLCE -10.5%, TSO -6.5%, TGT -4.3%, LLY -3.6%, SONC -2.2% (light volume).

A few financial related names showing weakness: BBVA -5.7%, STD -4.5%, DB -4.2%, UBS -3.3%, ING -1.9%, C -1%.

Select metals/mining stocks trading lower: BBL -1.7%, VALE -1.7% (downgraded to Neutral from Buy at UBS), BHP -1.6%, MT -1.5%, RIO -0.6%.

Select oil/gas related names showing early weakness: E -2.2%, RDS.A -1.7%, TOT -1.3%, BP -0.7%, STO -0.6%.

Other news: CSE -1.4% (announced last night that John Delaney is taking a leave of absence from his position as Executive Chairman, without pay), CCL -1.3% (still checking for anything specific), RPRX -1.2% (announced its Investigational New Drug Application for Proellex-V, or vaginally delivered Proellex, has been accepted by the FDA).

Analyst comments: SNY -2.9% (downgraded to Neutral from Overweight at JP Morgan), AZN -2.2% (downgraded to Underweight from Neutral at JP Morgan), YHOO -1.5% (downgraded to Hold from Buy at Jefferies), PLL -1.4% (downgraded to Underperform from Neutral at Macquarie), SAM -1.4% (downgraded to Sell from Neutral at Goldman), GOOG -0.5% (downgraded to Hold from Buy at Benchmark).

In reaction to disappointing earnings/guidance/SSS: AEO -14.2%, PLCE -10.5%, TSO -6.5%, TGT -4.3%, LLY -3.6%, SONC -2.2% (light volume).

A few financial related names showing weakness: BBVA -5.7%, STD -4.5%, DB -4.2%, UBS -3.3%, ING -1.9%, C -1%.

Select metals/mining stocks trading lower: BBL -1.7%, VALE -1.7% (downgraded to Neutral from Buy at UBS), BHP -1.6%, MT -1.5%, RIO -0.6%.

Select oil/gas related names showing early weakness: E -2.2%, RDS.A -1.7%, TOT -1.3%, BP -0.7%, STO -0.6%.

Other news: CSE -1.4% (announced last night that John Delaney is taking a leave of absence from his position as Executive Chairman, without pay), CCL -1.3% (still checking for anything specific), RPRX -1.2% (announced its Investigational New Drug Application for Proellex-V, or vaginally delivered Proellex, has been accepted by the FDA).

Analyst comments: SNY -2.9% (downgraded to Neutral from Overweight at JP Morgan), AZN -2.2% (downgraded to Underweight from Neutral at JP Morgan), YHOO -1.5% (downgraded to Hold from Buy at Jefferies), PLL -1.4% (downgraded to Underperform from Neutral at Macquarie), SAM -1.4% (downgraded to Sell from Neutral at Goldman), GOOG -0.5% (downgraded to Hold from Buy at Benchmark).

Where's the Remote?

By James "Rev Shark" DePorre

Jan 05, 2012 | 8:29 AM EST

"We shall have no better conditions in the future if we are satisfied with all those which we have at present." --Thomas Edison

We are running a repeat of 2011 this morning as the market struggles on worries about European sovereign debt. The euro is at fresh multi-month lows, a couple of European banks have been halted and bond yields are rising sharply. It's like watching a repeat of a bad television show with the knowledge that you're sure to see it again very soon.

While the Europe issues are nothing new, it's still a concern. Positive seasonality is starting to fall off, the indices are slightly extended and the recent momentum has been tepid, which increases the risk of profit-taking.

Also troubling is an American Association of Individual Investors (AAII) sentiment poll has only 17% bears. According to SentimenTrader.com, that is the second-lowest showing in six years, the only lower reading coming the week before Christmas of 2010.

Given all the angst about Europe, it's hard to understand how bearishness could be so low but it is troubling if there really is that much complacency about the problems that exist. It raises the chances of a sharp correction substantially when there is the possibility that this many people could be caught leaning the wrong way. All we seem to hear about lately is how Europe is going to be a problem, but people seem to be numb to negativity after having to deal with it for years now.

While it is worrisome to see complacency, it is important to keep in mind that the sentiment polls are not accurate timing devices. Just look at what happened after the very low level of bears in December of last year. The market continued to run until Feb. 18, 2011 before a correction finally kicked in. If you shorted based on the low level of bearishness in December, you were killed. Sentiment is just one consideration among many to consider when looking at market direction.

I bring up sentiment because it is a headwind and may prevent us from "climbing the wall of worry," which has been the tendency for a couple of years. If we have so few bears, then there may not be much idle cash to keep driving us up, despite a laundry list of negatives.

I've been leaning more defensively the last day or two, as I want to make sure I protect profits from the Santa Claus rally. It has been nice to see a little bit of hot money, momentum action in small-cap energy stocks, but this market still lacks leadership or themes.

One of the things that really plagued us in the second half of 2011 was that the Investor's Business Daily momentum style did not work well. We just never had groups or sectors, and there were only a few big names trading at their highs.

Stocks were too highly correlated and moved in tandem with European news. Stock-picking took a backseat to short-term market timing, and I'm not convinced that is about to change.

I'm going to lean a bit more defensive here, especially since I don't see many places to load up for position trades. We need to muddle through the European issues again and then deal with an earnings season that has already seen the most warnings in years. The fact that there are so few bears doesn't give us much short-squeeze fuel, either. I'll be looking to pick off some longs again, like we were able to do in the energy sector yesterday, but I'm afraid upside momentum offerings are going to be slim.

By James "Rev Shark" DePorre

Jan 05, 2012 | 8:29 AM EST

"We shall have no better conditions in the future if we are satisfied with all those which we have at present." --Thomas Edison

We are running a repeat of 2011 this morning as the market struggles on worries about European sovereign debt. The euro is at fresh multi-month lows, a couple of European banks have been halted and bond yields are rising sharply. It's like watching a repeat of a bad television show with the knowledge that you're sure to see it again very soon.

While the Europe issues are nothing new, it's still a concern. Positive seasonality is starting to fall off, the indices are slightly extended and the recent momentum has been tepid, which increases the risk of profit-taking.

Also troubling is an American Association of Individual Investors (AAII) sentiment poll has only 17% bears. According to SentimenTrader.com, that is the second-lowest showing in six years, the only lower reading coming the week before Christmas of 2010.

Given all the angst about Europe, it's hard to understand how bearishness could be so low but it is troubling if there really is that much complacency about the problems that exist. It raises the chances of a sharp correction substantially when there is the possibility that this many people could be caught leaning the wrong way. All we seem to hear about lately is how Europe is going to be a problem, but people seem to be numb to negativity after having to deal with it for years now.

While it is worrisome to see complacency, it is important to keep in mind that the sentiment polls are not accurate timing devices. Just look at what happened after the very low level of bears in December of last year. The market continued to run until Feb. 18, 2011 before a correction finally kicked in. If you shorted based on the low level of bearishness in December, you were killed. Sentiment is just one consideration among many to consider when looking at market direction.

I bring up sentiment because it is a headwind and may prevent us from "climbing the wall of worry," which has been the tendency for a couple of years. If we have so few bears, then there may not be much idle cash to keep driving us up, despite a laundry list of negatives.

I've been leaning more defensively the last day or two, as I want to make sure I protect profits from the Santa Claus rally. It has been nice to see a little bit of hot money, momentum action in small-cap energy stocks, but this market still lacks leadership or themes.

One of the things that really plagued us in the second half of 2011 was that the Investor's Business Daily momentum style did not work well. We just never had groups or sectors, and there were only a few big names trading at their highs.

Stocks were too highly correlated and moved in tandem with European news. Stock-picking took a backseat to short-term market timing, and I'm not convinced that is about to change.

I'm going to lean a bit more defensive here, especially since I don't see many places to load up for position trades. We need to muddle through the European issues again and then deal with an earnings season that has already seen the most warnings in years. The fact that there are so few bears doesn't give us much short-squeeze fuel, either. I'll be looking to pick off some longs again, like we were able to do in the energy sector yesterday, but I'm afraid upside momentum offerings are going to be slim.

DNDN rallib eelturul, kauplemas 18% plusspoolel, $ 9 kandis.

Firma alandab prognoose, aga tähtsam uudis ilmselt Provenge osas:

Dendreon sees Q4 revs below consensus; provides PROVENGE updates (7.60)

Co issues downside guidance for Q4 (Dec), sees Q4 (Dec) revs of ~$82 mln vs. $86.77 mln Capital IQ Consensus Estimate.

The Centers for Medicare and Medicaid Services updated their coverage policy to now cover the infusion costs associated with the administration of PROVENGE. With this decision, the coverage of PROVENGE is now consistent with all other infused biologics. A recent analysis suggests that approximately 75% of patients had minimal or no out-of-pocket costs for PROVENGE.

Firma alandab prognoose, aga tähtsam uudis ilmselt Provenge osas:

Dendreon sees Q4 revs below consensus; provides PROVENGE updates (7.60)

Co issues downside guidance for Q4 (Dec), sees Q4 (Dec) revs of ~$82 mln vs. $86.77 mln Capital IQ Consensus Estimate.

The Centers for Medicare and Medicaid Services updated their coverage policy to now cover the infusion costs associated with the administration of PROVENGE. With this decision, the coverage of PROVENGE is now consistent with all other infused biologics. A recent analysis suggests that approximately 75% of patients had minimal or no out-of-pocket costs for PROVENGE.

Sears Hldg slips slightly under its near eight year close low from Nov 2008 at 28.50

DNDN on teinud hommikuse uudise peale täna suure hüppe, aktsia kauples vahepeal isegi 50% plusspoolel, aga nüüd on osa tõusust tagasi andnud ja kaupleb 42% plusspoolel, mille taga osaliselt Brean Murray kommentaar, kellel on aktsiale juba varem antud Müü reiting koos $ 6 hinnasihiga. Analüütikud usuvad, et konkurents ei jäta DNDN-le ravimile väga palju mänguruumi.

Dendreon: Beats 4Q11 revenue for sure, but competitive landscape should change with upcoming Zytiga phase 3 results as well as MDV3100 approval - Brean Murray (10.97 +3.37)

Brean Murray notes DNDN released the 4Q11 gross Provenge revenue of $82 million, which beat the consensus estimates of $72 million, and their estimate of $76 million. Consensus likely still included some hepatitis C royalties from analysts that did not yet remove them due to Dendreon's sale of these royalties in early December, so the beat was more like $13 million rather than $10 million. Firm says with gross to net expected to be about 6%, they expect net revenue for 4Q11 to be about $77 million and believe that the stock has overreacted to this announcement, especially given management's continued expectation of modest sequential growth in 2012. Firm says this result was clearly viewed as a positive for Dendreon, given the stock reaction that they view as way overdone, but they emphasize the competition to come from Zytiga once clinically successful and approved in the pre-chemotherapy setting, as well as from MDV3100 off-label starting late in 2012.

Dendreon: Beats 4Q11 revenue for sure, but competitive landscape should change with upcoming Zytiga phase 3 results as well as MDV3100 approval - Brean Murray (10.97 +3.37)

Brean Murray notes DNDN released the 4Q11 gross Provenge revenue of $82 million, which beat the consensus estimates of $72 million, and their estimate of $76 million. Consensus likely still included some hepatitis C royalties from analysts that did not yet remove them due to Dendreon's sale of these royalties in early December, so the beat was more like $13 million rather than $10 million. Firm says with gross to net expected to be about 6%, they expect net revenue for 4Q11 to be about $77 million and believe that the stock has overreacted to this announcement, especially given management's continued expectation of modest sequential growth in 2012. Firm says this result was clearly viewed as a positive for Dendreon, given the stock reaction that they view as way overdone, but they emphasize the competition to come from Zytiga once clinically successful and approved in the pre-chemotherapy setting, as well as from MDV3100 off-label starting late in 2012.

Kui USA töötleva tööstuse ISM oli oodatust parem, siis mõni aeg tagasi raporteeritud teenindusektori ISM jälle pisut nõrgem

December ISM Services 52.6 vs 53.0 Briefing.com consensus; November 52.0

December ISM Services 52.6 vs 53.0 Briefing.com consensus; November 52.0