French President: France will keep our AAA rating. Légion étrangère starts regular traing for operation "Le Boomerang".

Mitu Mistralit peab tootma, et Prantsusmaa AAA reiting säiliks?

Gapping down

In reaction to disappointing earnings/guidance: STV -5.7% (light volume), P -5.1%.

Select financial related names showing weakness: BBVA -2.2%, ING -2.1%, BAC -1.9%, MS -1.6%, STD -1.6%, C -1.5%, HBC -1%.

Metals/mining stocks trading lower: MT -3.6%, SLV -3.5%, VALE -3.3%, SVM -2.6%, RIO -2.6%, HL -2.6%, CDE -2.3%, BHP -2.2%, BBL -2.2%, AU -1.6%, GDX -1.4%, AUY -1.3%, GLD -0.6%.

Select oil/gas related names showing early weakness: WFT -3%, STO -2.5%, SDRL -2.3%, BP -2.1%, CVX -1.7% (believes that approximately 2,400 barrels of oil have been emitted to date since seeps were first detected on November 9), TOT -1.7%, RDS.A -1.6%, E -1.5%.

Other news: DMND -12.8% (under pressure following reports that director Joseph Silveira died from alleged suicide with ongoing accounting investigation), ALU -6.3% (still checking), NLST -5.5% (discloses Sales Agreement with Ascendiant Capital Markets), FNV -2.8% (announced C$340 mln bought deal financing), CCL -2.7% (still checking), LEN -2.3% (ticking lower, prices $350 mln of its 3.25% Convertible Senior Notes due 2021), CELG -0.5% (will discontinue Phase III MAINSAIL trial in castrate-resistant prostate cancer).

Analyst comments: JNY -3.9% (downgraded to Neutral from Buy at Lazard ), ABH -3.3% (ticking lower, downgraded to Sector Perform from Outperform at RBC Capital), FRO -2.6% (continued weakness, downgraded to Underperform at FBR Capital).

In reaction to disappointing earnings/guidance: STV -5.7% (light volume), P -5.1%.

Select financial related names showing weakness: BBVA -2.2%, ING -2.1%, BAC -1.9%, MS -1.6%, STD -1.6%, C -1.5%, HBC -1%.

Metals/mining stocks trading lower: MT -3.6%, SLV -3.5%, VALE -3.3%, SVM -2.6%, RIO -2.6%, HL -2.6%, CDE -2.3%, BHP -2.2%, BBL -2.2%, AU -1.6%, GDX -1.4%, AUY -1.3%, GLD -0.6%.

Select oil/gas related names showing early weakness: WFT -3%, STO -2.5%, SDRL -2.3%, BP -2.1%, CVX -1.7% (believes that approximately 2,400 barrels of oil have been emitted to date since seeps were first detected on November 9), TOT -1.7%, RDS.A -1.6%, E -1.5%.

Other news: DMND -12.8% (under pressure following reports that director Joseph Silveira died from alleged suicide with ongoing accounting investigation), ALU -6.3% (still checking), NLST -5.5% (discloses Sales Agreement with Ascendiant Capital Markets), FNV -2.8% (announced C$340 mln bought deal financing), CCL -2.7% (still checking), LEN -2.3% (ticking lower, prices $350 mln of its 3.25% Convertible Senior Notes due 2021), CELG -0.5% (will discontinue Phase III MAINSAIL trial in castrate-resistant prostate cancer).

Analyst comments: JNY -3.9% (downgraded to Neutral from Buy at Lazard ), ABH -3.3% (ticking lower, downgraded to Sector Perform from Outperform at RBC Capital), FRO -2.6% (continued weakness, downgraded to Underperform at FBR Capital).

October PCE Prices- Core M/M +0.1% vs +0.1% Briefing.com consensus

PCE Headline Y/Y +2.7%; Core Y/Y +1.7%

Oct. Personal Income +0.4% vs. +0.3% Briefing.com consensus; prior +0.1%

October Durable Orders ex-trans +0.7% vs 0.0% Briefing.com consensus; Prior revised to +0.6% from +1.8%

October Personal Spending +0.1% vs +0.3% Briefing.com consensus

Initial Jobless Claims 393K vs. 391K Briefing.com consensus; prior revised to 391K from 388K

Continuing Claims rises to 3.691 mln from 3.623 mln

PCE Headline Y/Y +2.7%; Core Y/Y +1.7%

Oct. Personal Income +0.4% vs. +0.3% Briefing.com consensus; prior +0.1%

October Durable Orders ex-trans +0.7% vs 0.0% Briefing.com consensus; Prior revised to +0.6% from +1.8%

October Personal Spending +0.1% vs +0.3% Briefing.com consensus

Initial Jobless Claims 393K vs. 391K Briefing.com consensus; prior revised to 391K from 388K

Continuing Claims rises to 3.691 mln from 3.623 mln

JPMi arvates on Euroopa ja USA majanduslik ning poliitiline seis järgnevate kuude jooksul rõhumas tooraineid, mistõttu langetatakse kogu sektor "underweight" peale. Zerohedge vahendab raportit.

Veebilehel techcrunch.com antakse teada, et tänavu tulevad interntentipoodidele pigem rõõmurohked pühad, sest inimesed on aktiivselt internetist ostlema asunud ning müüginumbrid on juba 14% võrra suuremad ($ 9,7 miljardit) kui möödunud aastal samal ajal.

Gapping up

In reaction to strong earnings/guidance: DE +6.8%, TIVO +3.2%.

Other news: SINO +37.7% (thinly traded, has signed a memorandum of understanding with Wilson, Sons Shipping Agency), AEZS +4.9% (Aeterna Zentaris and Hikma Pharmaceuticals sign a commercialization and licensing agreement for Perifosine for Middle East and North Africa Region), BSX +3.6% (receives FDA approval for PROMUS Element plus platinum chromium stent system), NOK +2.7% (Nokia Siemens announced restructuring), FDML +0.8% (Carl Icahn discloses additional purchases; Icahn discloses purchase of 165K shares at $13.70-13.74, on 11/18-11/22), VIVO +0.7% (ticking higher; early strength attributed to positive mention in Barron's).

Analyst comments: JASO +1.9% (upgraded to Market Perform from Underperform at Wells Fargo).

In reaction to strong earnings/guidance: DE +6.8%, TIVO +3.2%.

Other news: SINO +37.7% (thinly traded, has signed a memorandum of understanding with Wilson, Sons Shipping Agency), AEZS +4.9% (Aeterna Zentaris and Hikma Pharmaceuticals sign a commercialization and licensing agreement for Perifosine for Middle East and North Africa Region), BSX +3.6% (receives FDA approval for PROMUS Element plus platinum chromium stent system), NOK +2.7% (Nokia Siemens announced restructuring), FDML +0.8% (Carl Icahn discloses additional purchases; Icahn discloses purchase of 165K shares at $13.70-13.74, on 11/18-11/22), VIVO +0.7% (ticking higher; early strength attributed to positive mention in Barron's).

Analyst comments: JASO +1.9% (upgraded to Market Perform from Underperform at Wells Fargo).

$LNG - Citigroup raises PT to $19 follwing GNF deal, says Phase 2 valuation would be huge $45/sh based on $2.0B EBITDA. New Street high PT.

Eile arutati Bloomberg TV-s analüüsimajade ajaloolist täpsust ja üllatavalt jäi keskmine 45% peale, kusjuures parimaks loeti Raymond Jamesi 67%-ga ja halvimaks RBC Capital Markets ~37%-ga.

November Michigan Sentiment- Final 64.1 vs 64.2 Briefing.com consensus; Prelim 64.2

ECB Jens Weidmann ütles täna uuesti selgelt ja kõvahäälselt, et ECB kaotab täielikult usaldusväärsuse, kui ta muutuks lender of last resort funktsiooni täitma.

A leading member of the European Central Bank's governing council Tuesday warned against the central bank becoming a lender of last resort for the euro zone, underlining the growing rift in the currency bloc about what role the ECB should play in fighting the debt crisis.

The ECB "would overstep its mandate and call its independence into question with a commitment as lender of last resort for highly-indebted member states," ECB Governing Council Member Jens Weidmann said in a speech delivered Tuesday.

EUR/USD täna üsna tugeva müügisurve all olnud. Esmalt mõjus negatiivselt Saksamaa võlakirjaoksjoni tehniline ebaõnnestumine ja võimaliku põhjuse müümiseks on andnud ka JPMi kommentaar eurotsooni majandusliku väljavaate osas.Pikemalt Zerohedge'i vahendusel

As we expect the Euro area economy to be in recession until late 2012, we think that a 25bp cut in December will not be the last. Hence, we have now pencilled in additional easing of 25bp at the policy meetings in March and June 2012. As the deposit facility will reach 0.25% already in December, the additional cuts may not lower the effective overnight rate much. In our view, those moves would nevertheless send important policy signals.

As we expect the Euro area economy to be in recession until late 2012, we think that a 25bp cut in December will not be the last. Hence, we have now pencilled in additional easing of 25bp at the policy meetings in March and June 2012. As the deposit facility will reach 0.25% already in December, the additional cuts may not lower the effective overnight rate much. In our view, those moves would nevertheless send important policy signals.

Markets are seeing some strength following a Reuters report citing the German daily Bild that German backing for the issuance of joint euro zone bonds is no longer being categorically ruled out

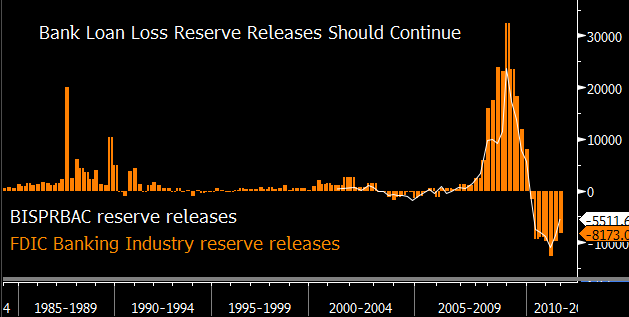

Bloomberg on eilses börsipäeva foorumis postitatud teemat täna samuti kajastamas. Alloleval graafikul on kujutatud USA pankade laenukahjumite reservid (negatiivne number tähendab, et reserve vähendatakse). Pangad on käimasoleva aasta Q2 käigus reserve kärpinud $9 miljardi võrra ja Q1 käigus vähenesid reservid $11 miljardi võrra.

UK Q3 GDP growth confirmed at +0.5%